Advertisement

China is closed for CNY for a week. SGX is closed for two days.

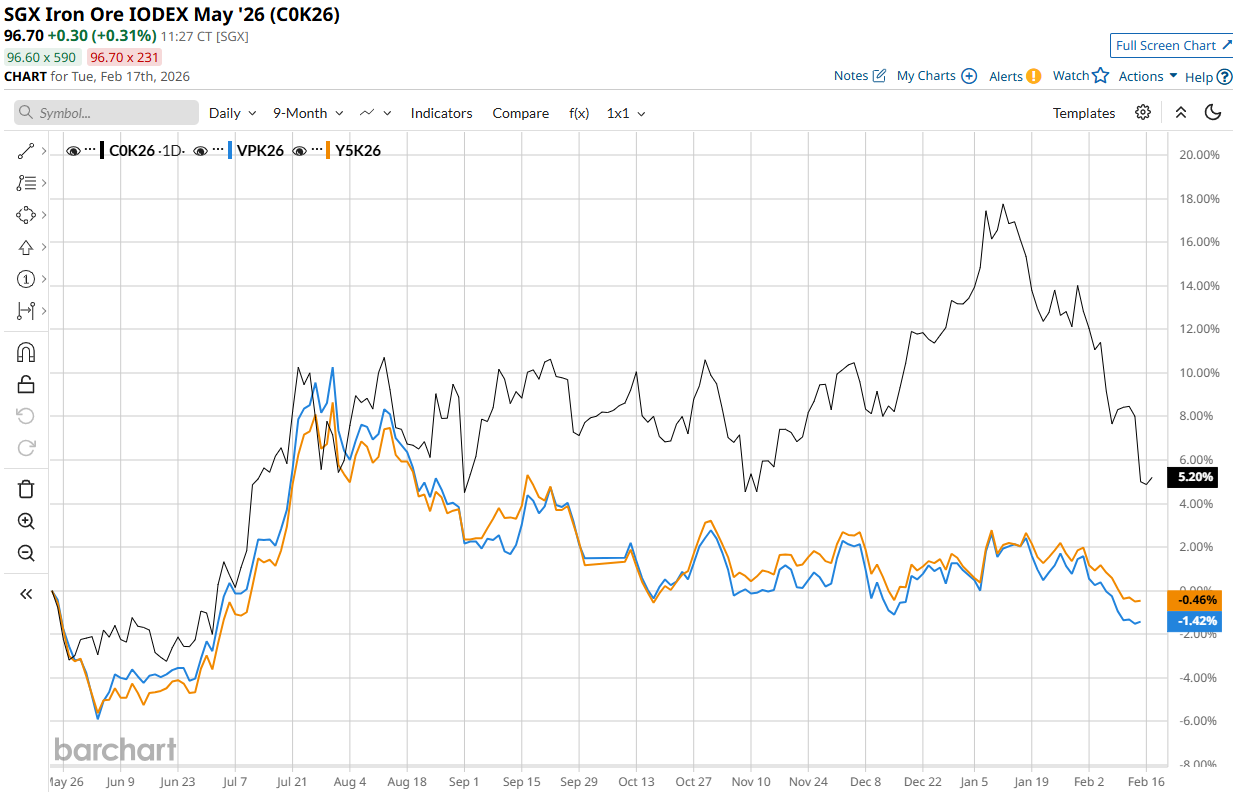

Steel profits have improved, and we will probably see a decent rebound in output post-holiday. However, I expect this will only serve to drive steel prices lower amid stalling (and contracting) steel export growth plus weak domestic demand.

On the supply side, we already know of incremental volume growth from the Pilbara, Capanema, and Simandou. You can add this.

Advertisement

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.