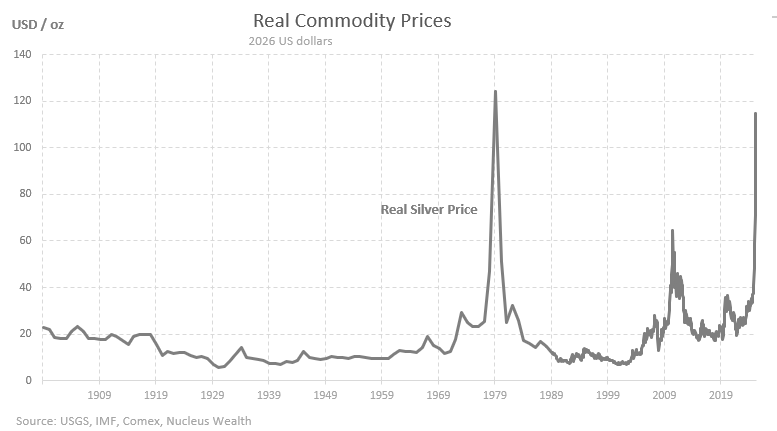

Silver surfed a massive wave, then wiped out. But it remains a long way above long-term prices. Is there a new paradigm for silver, or are we heading back to its long term real price of sub-$20?

Background on metals pricing

For most industrial metals, like iron or copper, the long-term commodity price is the cost to extract it from the ground + a premium. When the premium is too high: more mines are built, the market floods with supply, the commodity price returns to normal.

Sometimes people will hoard these metals for short periods; mines do take years to build; other materials can be substituted. But, eventually, economic rationality wins out.

Gold is different

Partly because it is really rare and expensive to extract. But mainly because we don’t actually do anything with around half of the gold produced, except bury it in a vault somewhere else.

The demand signal is not the same. i.e. if the price of an industrial metal doubles, users will use less of it. Gold doubles, and sometimes that just means that investors & central banks want more of it.

Is silver different?

Silver is mostly an industrial metal. But, investors play some role, and so in times like today, they can have an outsized effect on prices. Only about 20% of silver is for investment, gold is closer to 50%.

Long term, adjusted for inflation, silver typically trades sub $25:

Silver is often viewed alongside gold, and for good reason. Both act as anti-US-dollar assets and tend to benefit when the USD weakens. This relationship has been particularly visible in recent months, as shifting expectations around the Federal Reserve — and the selection of a more policy-stable Fed Chair — reduced the probability of aggressive monetary easing. That shift removed some tail-risk inflation scenarios from investor psychology, pressuring both gold and silver.

There are differences .

| Gold | Silver | |

| Inflation Hedge | Sometimes effective; failed in the high-inflation 1980s | Same story — silver lost value during the 1980s |

| Safety / Geopolitics | A strong “insurance” asset during crises | Shadow effect: benefits, but weaker |

| Supply Dynamics | Scarcer, expensive to mine. Gold is about 50-100x more expensive to produce | Way more abundant, much cheaper to produce |

| Investor Influence | Investors (excluding central banks) are about a third of demand. | Investors account for ~20% of demand |

| Central Bank Role | Huge — buying/selling moves the market | Minimal — banks hold little silver |

Because investors (including central banks) make up a much smaller share of silver’s demand than gold’s, sentiment shifts can cause outsized price swings. A sudden inflow or outflow of capital represents a much larger percentage of total silver demand, amplifying volatility and creating what many analysts call the “greater-fool dynamic” — buying not just for fundamental value, but in the hope that another investor will pay more.

Both metals rely partly on the idea of limited supply meeting perceived limitless demand, but silver’s relative abundance keeps its scarcity stories in check.

Silver Supply: Flat Mining Output, Flexible Recycling, and Realistic Limits

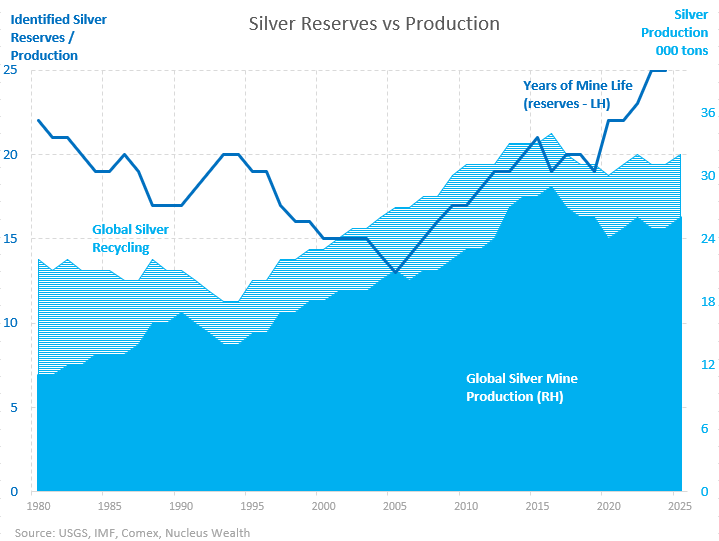

A major driver of silver’s recent bull case has been the belief that the world is running into a structural shortage, especially given demands from solar and electronics manufacturing. At first glance, it seems plausible: global mine production has stagnated for nearly a decade.

However, zoom out to a longer timeline and a different picture emerges. Since 1980, silver mining output has more than doubled. And the number of years of reserves is higher today than then. i.e discoveries (and higher prices) have increased reserves faster than the growth in production.

Recycling is also an overlooked supply lever. Today, around 190–200 million ounces of silver are recycled annually, but during price spikes this can jump to 300 million ounces or more. The recycling pool is vast, covering everything from old tableware and jewellery to industrial scrap. Much of this becomes economical only when prices rise, dramatically increasing the recyclable supply.

So, undeveloped supply is available if miners commit to projects.

Silver: Rarely the primary metal

Because silver is often a byproduct of copper, gold, zinc, or tin mining, higher prices for these metals can indirectly increase silver output. i.e. when copper mines expand, sometimes that will increase the supply of silver as well.

At production costs in the low $20s, today’s prices are extremely profitable, signalling miners to expand capacity. Put simply: while supply can be tight in the short term, the silver ecosystem has enough elasticity — especially through recycling — to accommodate large surges in demand over time.

Silver Demand: Solar Hype vs. Reality, and Why Investment Dominates Volatility

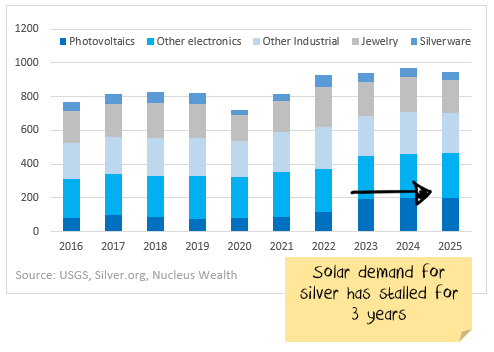

Demand for silver is often framed around its industrial uses, particularly solar photovoltaics. While solar has been the standout growth sector over the last decade, it represents roughly the same volume as investment demand — and crucially, solar growth has stalled for the past three years.

Key sector trends show a clearer picture:

| Growth | Issues | |

| Solar (PV) | Strong historical growth; now plateauing | Grid constraints slow expansion despite tech improvements |

| Jewellery | Flat or declining | Higher silver prices reduce substitution profitability |

| Electronics | ~1% growth | Electrification helps, but not a game-changer |

| Other industrial | <1% growth | No new major demand uses emerging |

| Investment | ?? unstable | Swings drive price volatility |

Solar could still double over the next decade, but this would increase global silver demand by only ~17%, requiring just 1–2% growth in annual output — historically very achievable.

The bottleneck in the energy transition lies in transmission and storage infrastructure, not silver shortages.

Investment flows remain the most important variable. Sentiment, speculation, macro fears, and online narratives can push silver dramatically higher in short windows, far beyond what fundamental demand would justify.

Outlook: Short-Term Explosiveness vs. Long-Term Gravity

In the short run, silver can behave like a leveraged macro trade. Fear of currency debasement, momentum trading, geopolitical shocks, or shifts in Fed expectations can easily push prices back above $100. These are the same forces that drove past spikes.But long-term, gravity reasserts itself. As new supply comes online and recycling surges at high prices, silver tends to settle into sustainable ranges that support profitable mining without creating shortages.

Historically, that has meant below $25 — and the same logic suggests prices will eventually drift back toward those levels over the next 10–15 years.The dynamic contrasts sharply with gold, which is anchored by central bank demand and geopolitical hedging. Silver, tied to industrial cycles and byproduct mining expansions, follows a more elastic, boom-and-bust pattern.

Key takeaway: Silver can deliver explosive short-term gains driven by sentiment — but long-term prices are likely to normalise as supply responds. We aren’t running out of silver. Solar panels are not going to swamp demand. What we have right now is an investor-driven boom. An investment in silver today is either:

- short-term demand continuing to swamp supply while mines are being built and/or

- a new paradigm where investors want way more silver than in the past, and more than mines will be able to produce

Both of those are bets better suited to speculators rather than investors.

Damien Klassen is Chief Investment Officer at the Macrobusiness Fund, which is powered by Nucleus Wealth.

Follow @DamienKlassen on X(Twitter) or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an Authorised Representative of Nucleus Advice Pty Limited, Australian Financial Services Licensee 515796. And Nucleus Wealth is a Corporate Authorised Representative of Nucleus Advice Pty Ltd.