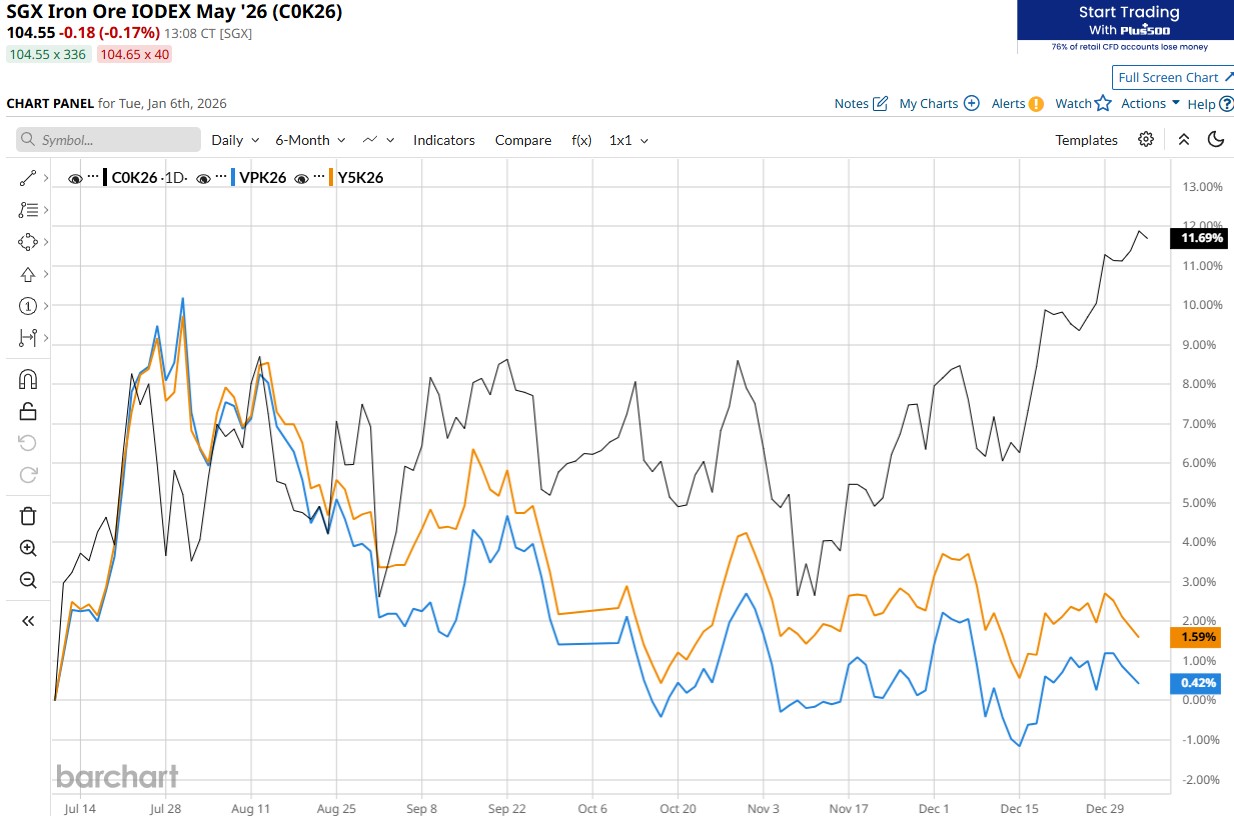

It seems nothing can bring sense to the iron ore market as the jaws widen further.

Scuttlebutt explains the seasonality.

Chinese iron ore prices are being underpinned by steelmakers restocking ahead of the Lunar New Year holiday in February, while tight domestic supplies are also lending further support.

The outlook beyond this point is hardly glowing.

With steel exports likely topping out and a rising yuan, I can’t see a great year for export growth.

Anti-involution policies are also crushing investment, so that domestic demand will lack an investment pulse.

Chinese steel output is likely to decline again by the regulation 3% or so.

The best hope for iron ore is a slow ramp-up for Simandou. S&P has more.

Simandou has been described by some as a “Pilbara killer” due to fears of the impact of its size and high grade on prices and demand for the lower-grade ore mined in Western Australia.

…”The insufficient railway capacity is the key reason for the slow iron ore shipments from Simandou. Due to a shortage of locomotives, the first shipment of 200,000 mt iron ore from Simandou took 22 days to complete loading,” said a Chinese mill source. He added that a 200,000 mt bulk carrier typically requires only two to three days to load.

…RBC said that achieving a stable nameplate capacity in 48-60 months for Simandou is “more realistic,” which means “meaningful tons” would only arrive in 2029, and will support “Pilbara margins relative to consensus.”

The upshot of all this is that the Pilbara will be “killed later, if at all. A slower Simandou ramp delays displacement of existing high-grade supply and supports medium-term grade and lump premiums,” RBC said.

…”We think Simandou is likely to export around 15 million mt of iron ore in 2026. At these volumes, we don’t expect any meaningful impact on iron ore prices next year as we think Chinese pig iron production may only decrease by around 1.5%-2% year over year. We see the IODEX averaging around $100/dmt in 2026,” Paul Bartholomew, lead ferrous metals analyst of S&P Global Energy, said.

That’s still a swing of 50mt towards surplus. It is material for prices.

The main delay at this juncture is the Wabtec locomotives, which were supposed to be built outside of China. Approximately 40 are expected to arrive from India during the first quarter. Eventually, it should have roughly 140 locomotives.

So, ramp-up is slow but will accelerate quickly from Q2.

As the creator of the phrase “Pilbara killer”, I stand by it. It was not meant to be taken literally.

What I meant was that Simndou would end the cozy iron ore oligopoly that has sustained prices at exorbitant levels for years.