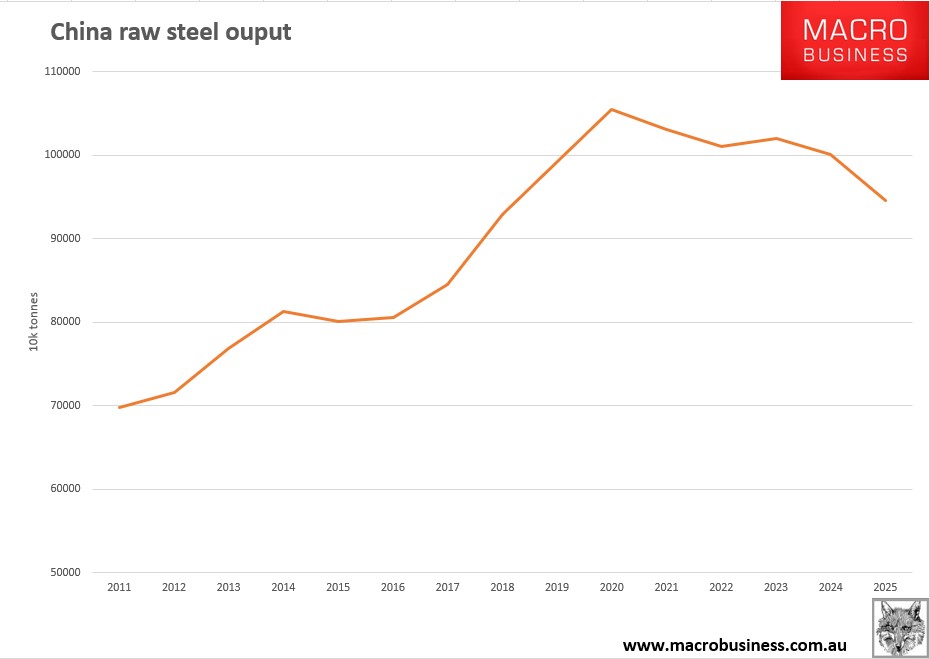

2025 turned out to be a banner year in the great steel crash.

As of the November data, Chinese output was down 4% year-to-date. With a generous extrapolation for December, Chinese steel output will have shrunk well below one billion tonnes in 2025, approaching 2018 levels.

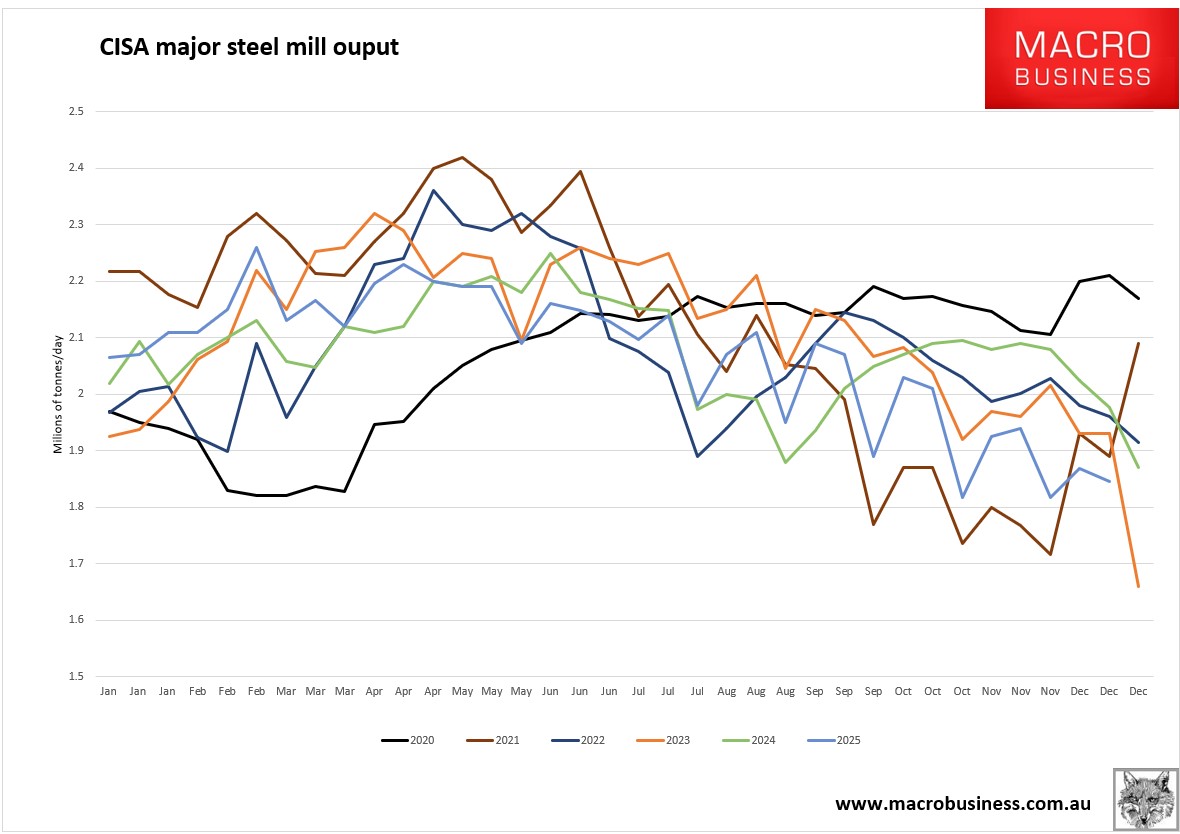

Leading CISA data confirms no late-year rebound for China.

Globally, it was even worse, with world steel output down roughly 4.6% in 2025.

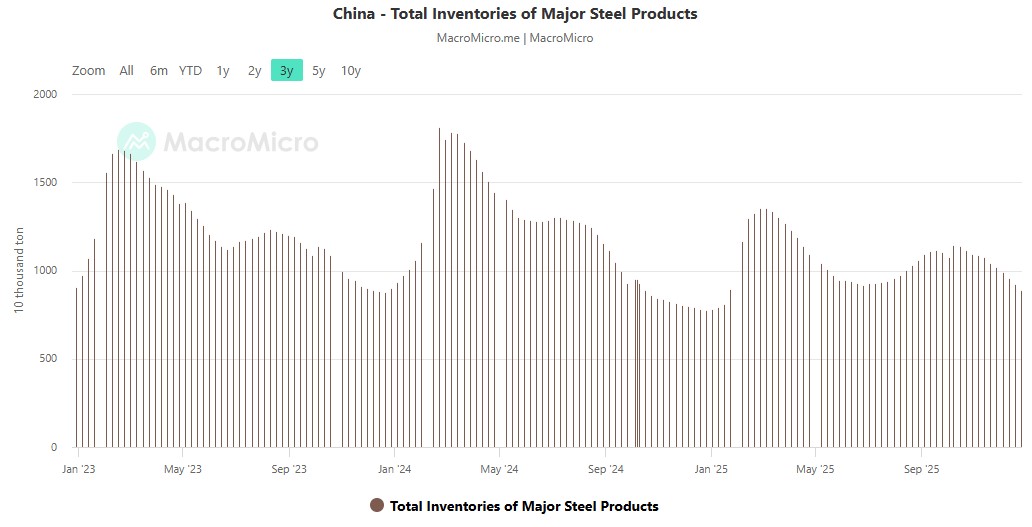

Also, according to CISA, steel inventory is seasonally high in China. Other measures are similar.

The new year restock will be muted.

This brings us to what 2026 will hold. Ongoing falls for raw steel volumes are a certainty.

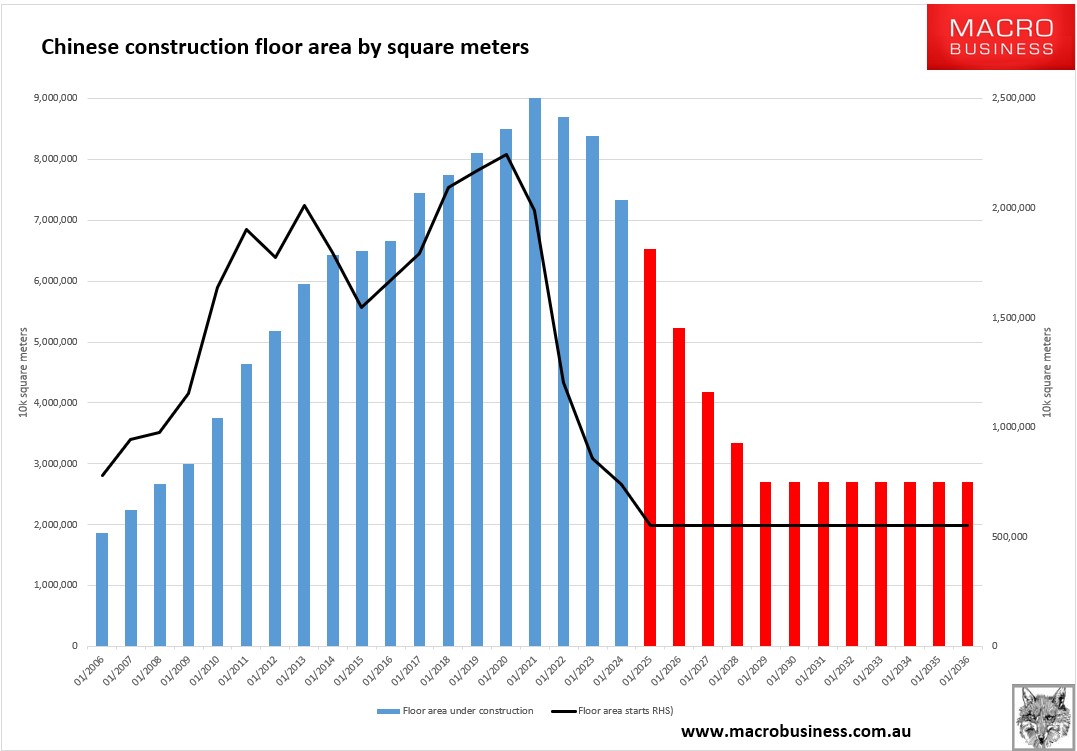

The real estate bust is getting worse, not better, and policymakers appear to have washed their hands of it.

Despite being down by three quarters from the 2020 peak, floor area starts are still falling faster than floor area under construction.

The latter will catch down eventually as idle, unsold, half-built, rotting stock is ever so slowly absorbed.

Meanwhile, prices and new floor area starts will keep falling.

We are barely one-third of the way through this adjustment in steel demand volumes from real estate.

So far, there have been two major shock absorbers for iron ore in this huge downstram demand bust.

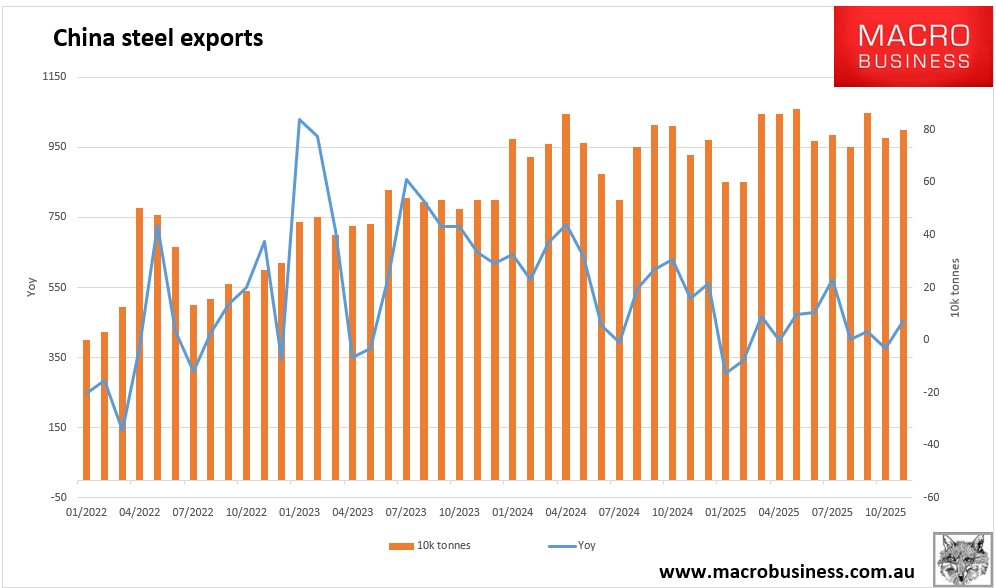

The first is the rise of Chinese steel exports. This has now played out, with tariffs rising in response, underscored by China’s new export-permitting regime. Exports will be flat or fall this year.

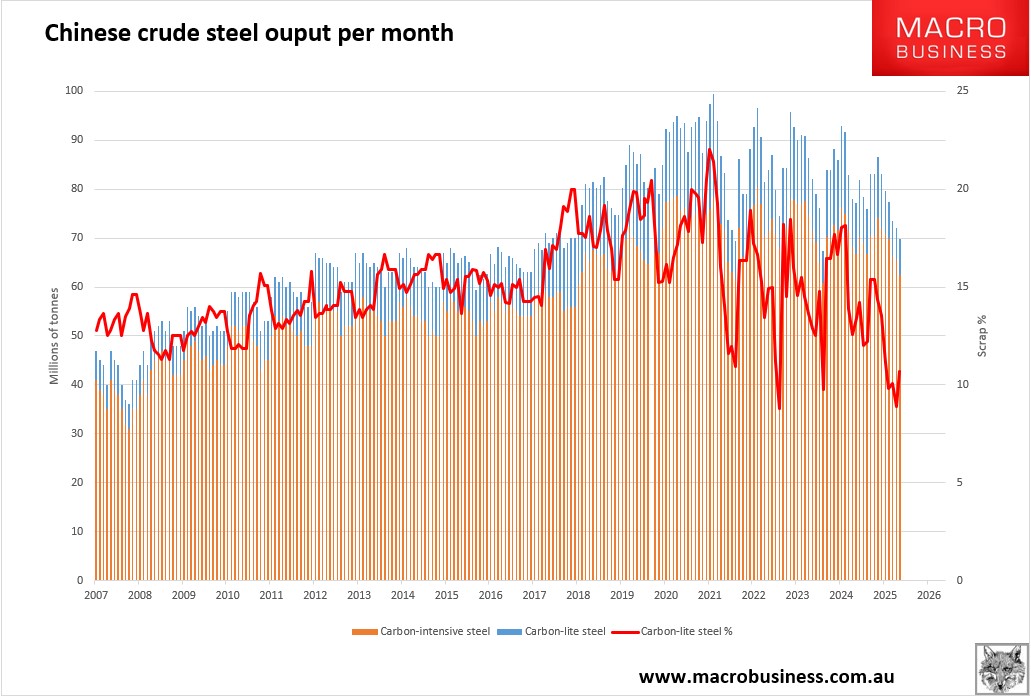

The second shock absorber has been China’s abandonment of decarbonising steel. Given its greater reliance on long product steel used in construction, steel recycling was always going to absorb a larger share of the real estate adjustment than blast furnace production. However, China has done nothing to prevent this, so steel recycling has collapsed, protecting iron ore-based blast furnace output.

China is now producing the same amount of recycled steel it did in 2009, while producing 50% higher tonnages from blast furnaces in reference ot the same year.

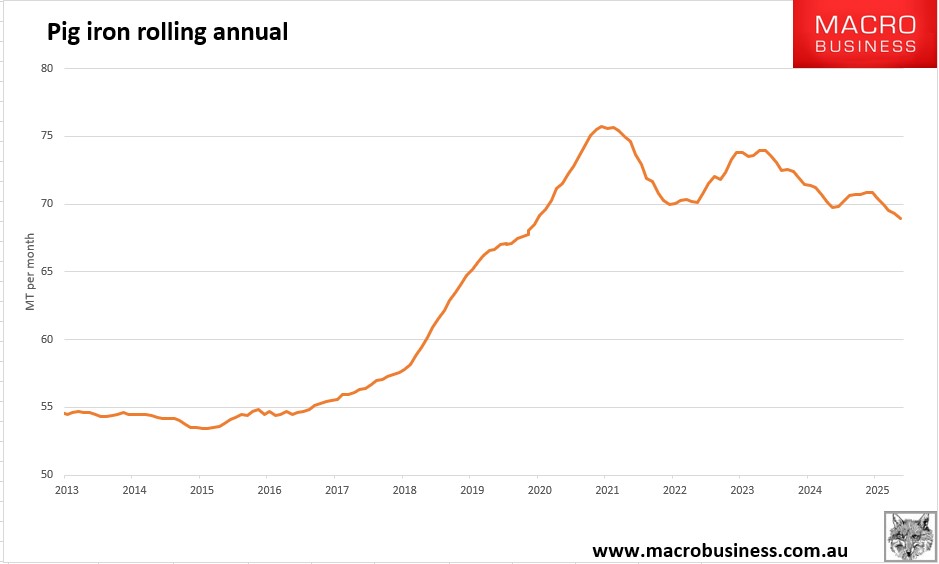

Even so, pig iron output is also falling slowly.

I expect Chinese steel output to continue falling at roughly a 3% pace for much of the next decade. At some point, China will have to adopt much stronger carbon pricing or similar measures, or steel recycling will go the way of the dodo.

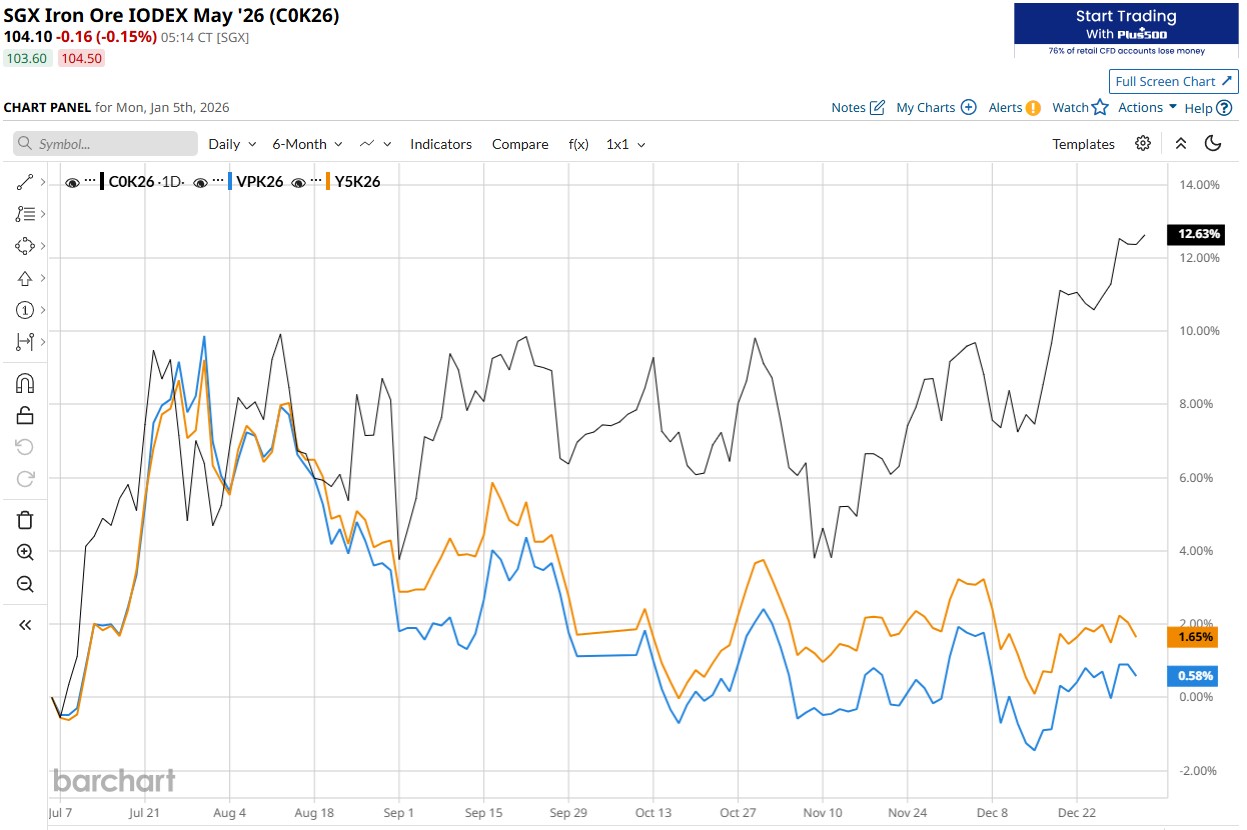

So far, the great steel crash has not significantly affected iron ore prices. However, blind Freddy can see the steadily ratcheting pressure from the demand side.

This has manifested itself in chronically weak steel mill margins, which has led them to buy as much cheaper low-grade ore as possible. This is partly why import volumes of iron ore have remained high.

But how long can this go on? The iron ore jaws must close eventually. Front-month futures are partying on short-term factors like the BHP-CMRG standoff, but even Chinese fumbling can’t hold the price up forever as Simandou, Gara Djiblet and Vale bring more volumes.

I am still playing the short sides timed with periods of seasonal weakness.