We’ve suddenly lurched from AI is unstoppable to a growth scare as jobs data weakens. The Market Ear.

Wishing & hoping & thinking & praying

AI mentions on earnings calls have exploded tenfold. Retail traders are back chasing the Mag7. Tech giants are borrowing record sums to fund data centers. For now, optimism is profit — but history calls this stage “late cycle.” Here is the latest collection of AI & Mag7 related charts.

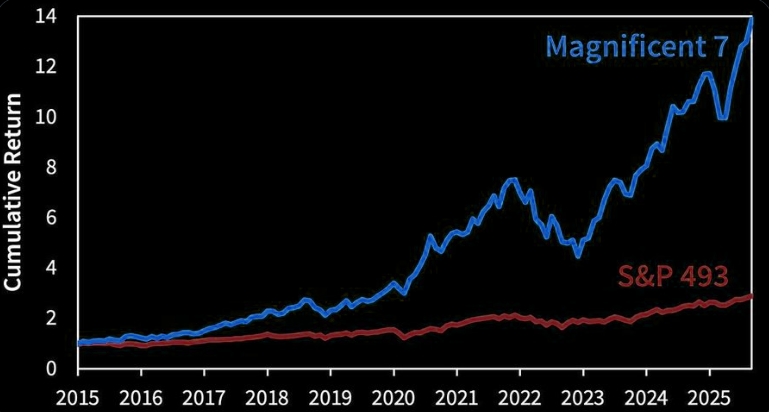

Standard (7) & poor’s (493)

Why is it even still called S&P 500?

Source: M Arouet

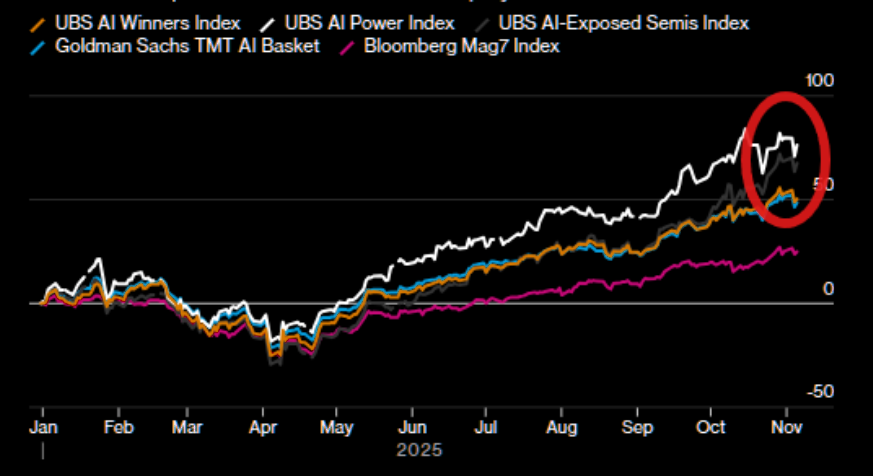

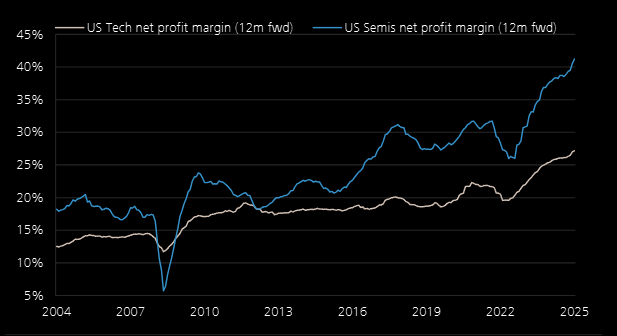

Catch me if you can

While the Mag-7 is up 25% YTD, the real eye-watering gains have been in the bank AI baskets which are up 50-75%.

Source: Bloomberg

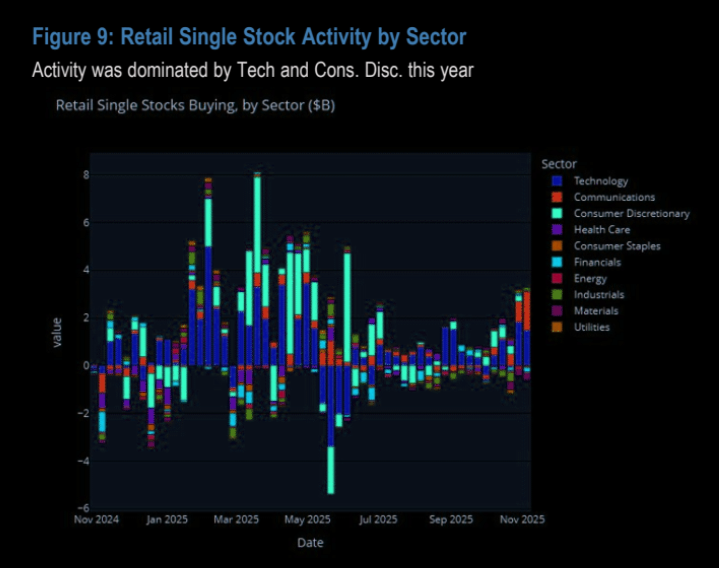

Retail Roaring: Back and Buying the Mag 7 (Again)

Retail trading activity continued to gain momentum this week, with cash equity purchases surging to $8.1B — the highest level in four months and well above the YTD average of $6.2B.

In addition to $5.3B in ETF buying, retail investors purchased $2.7B in single stocks, with activity concentrated in Technology and Communication Services. The Magnificent 7 accounted for nearly all of the single-stock buying.

Source: JPM Quant

Everything

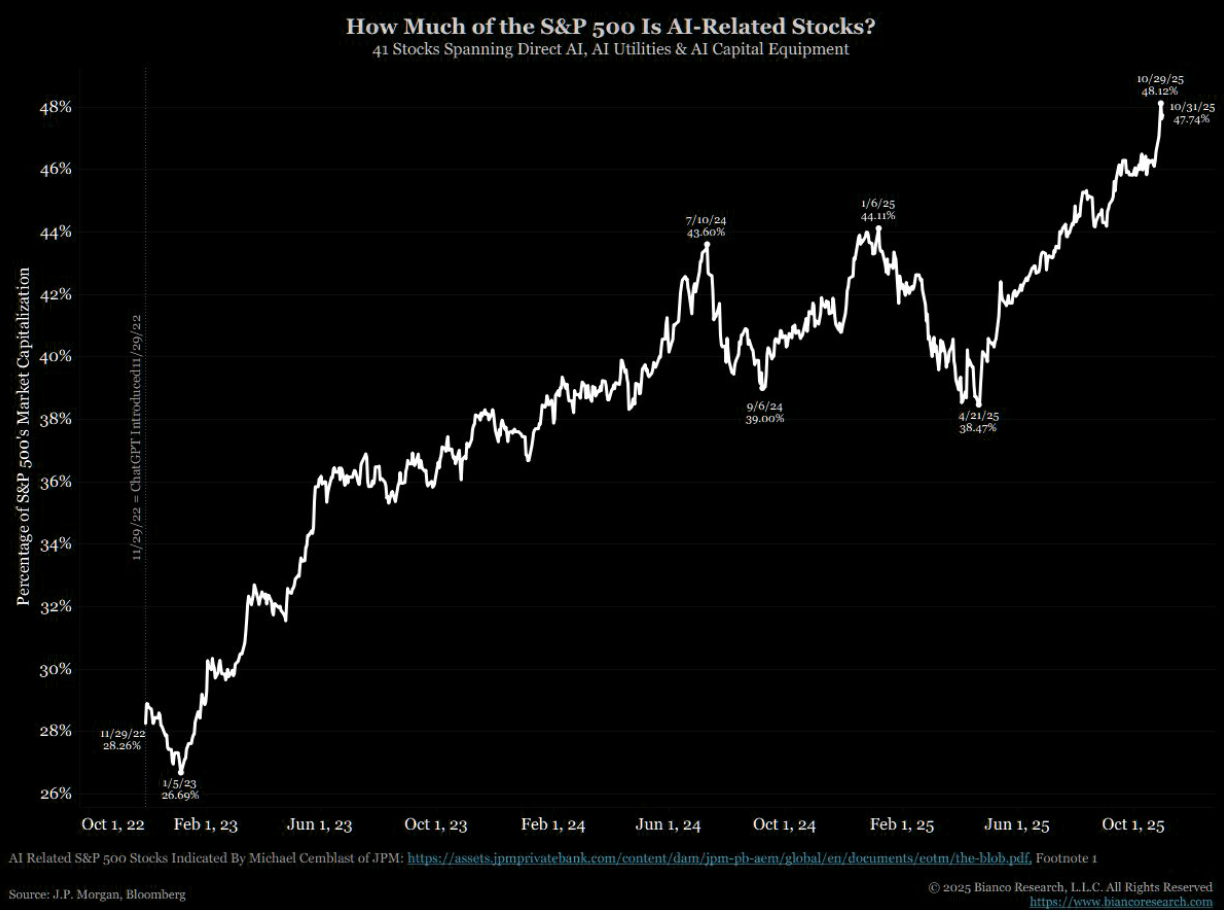

AI stocks are already at a record concentration for one theme, 48% of the S&P 500.

Source: JPM / Bianco

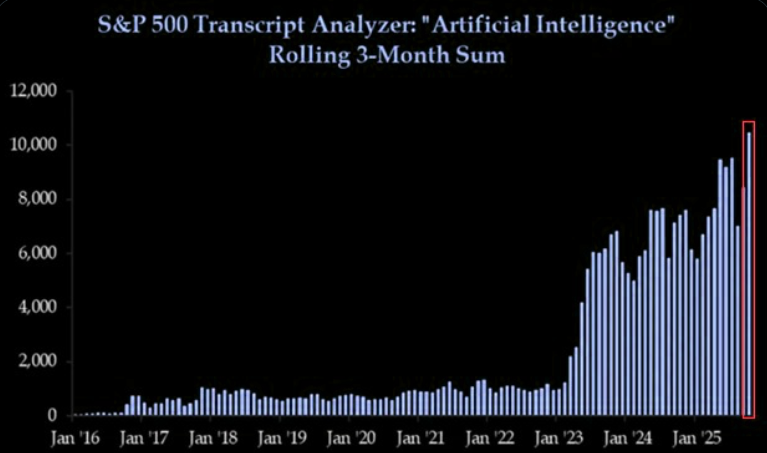

This AI thing looks like it is catching on…

“AI” mentions during S&P 500 earnings calls this quarter have surpassed 10,000 for the first time in history. This figure has DOUBLED over the last 18 months. To put this into perspective, “AI” was cited just ~1,000 times during the 3-month period ending March 2023.

Source: TKL

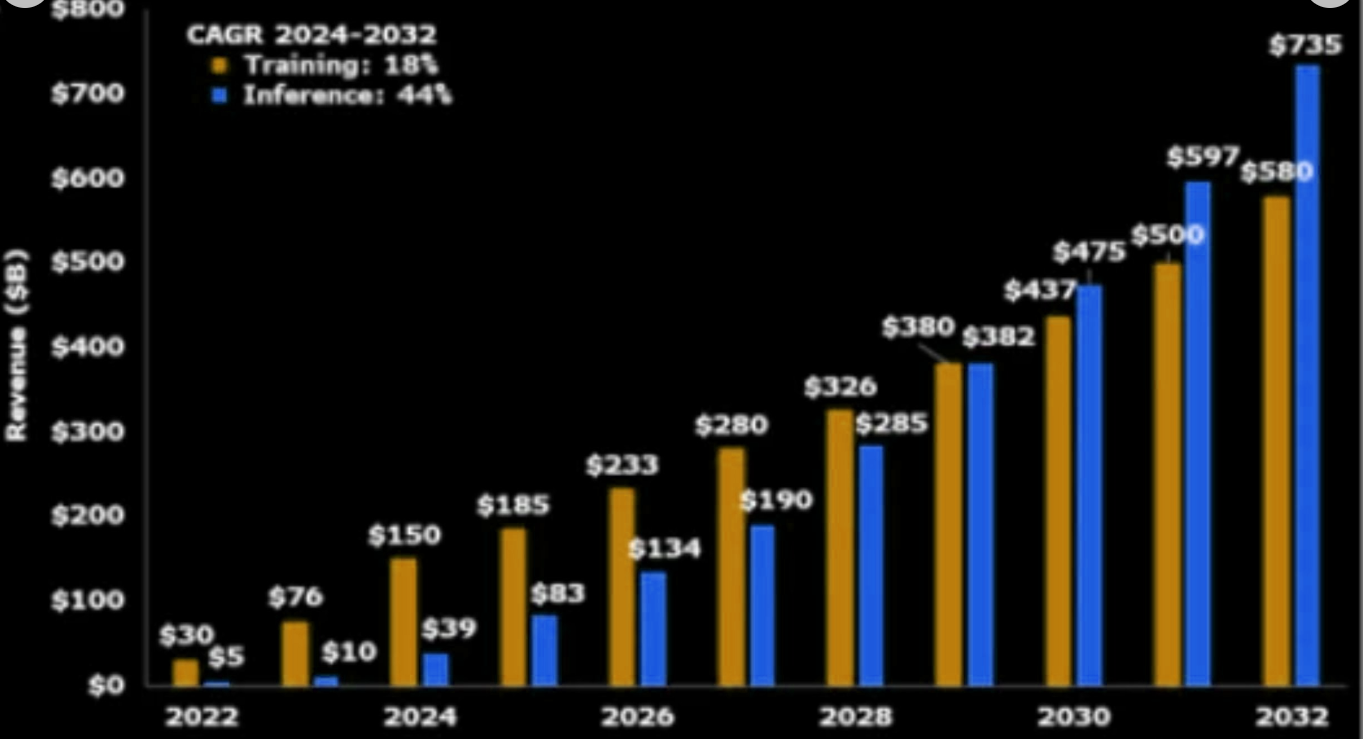

A nice normal 44% CAGR for the next 7 years…

AI inference rev. estimated to grow 44% CAGR until ’32.

Source: Bloomberg

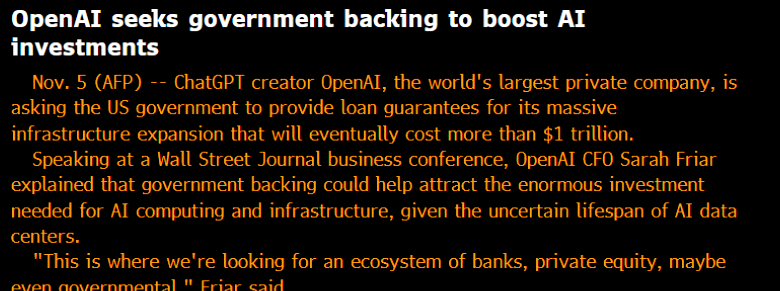

I smell a rat

“Why does Sam Altman need the taxpayer to guarantee their debt if they are going to make hundreds and hundreds of billions of dollars? Has he just done a cash analysis and realised he’s cash flow short?” (Julian Brigden)

Source: Bloomberg

Reminiscence of…

Deutsche Bank explores hedges for data centre exposure as AI lending booms. Executives discussing options including shorting basket of artificial intelligence stocks or using derivatives to transfer risk.

The potential bubble

UBS sees a potential bubble here: The bubble risk sits in the margins of tech, particularly semis. Margins typically compress as capital intensity rises and competition expands – think OpenAI partnering to produce more ASICs through JVs or moving into browsers and online advertising, encroaching on existing players’ turf.

Source: UBS

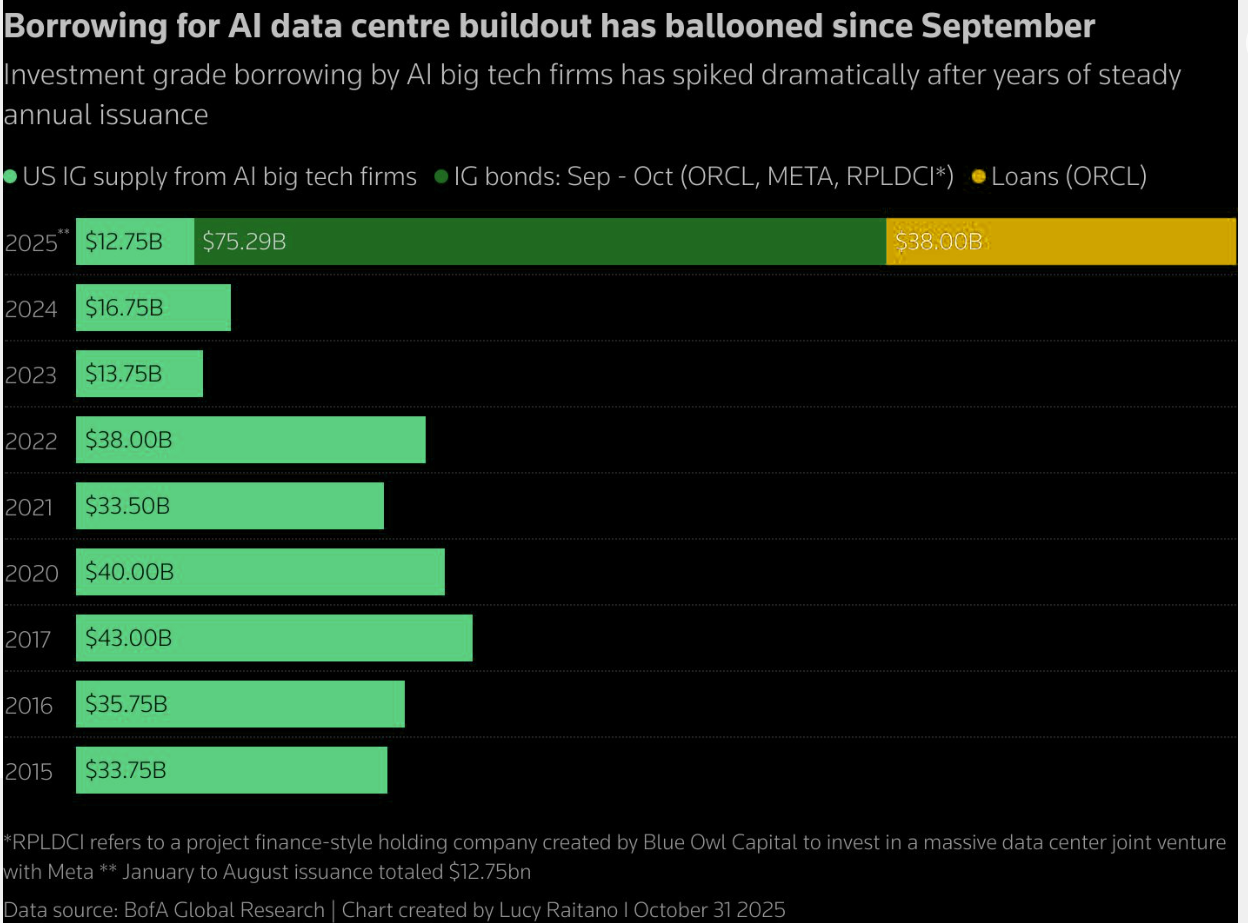

Big Tech borrowing for AI data centers

2015-2024 average: $32B/year

Sept-Oct 2025 alone: $75B

> Meta borrowed $30B

> Oracle borrowed$18B

> META also did $27B off-balance sheet with Blue Owl

AI companies now 14% of IG index.

The “money-printing” tech companies are… borrowing heavily.

Source: @junkbondinvestor

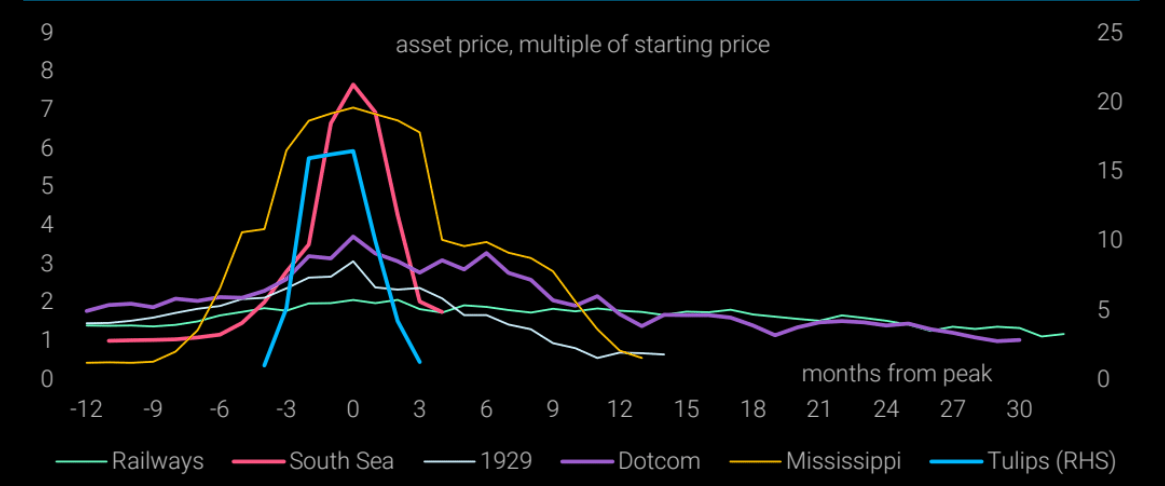

Bubble history

The world’s most infamous bubbles.

Source: TS Lombard

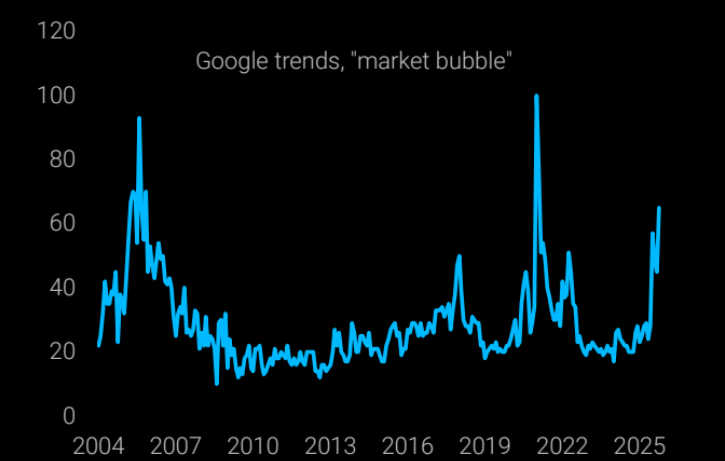

Bubble talk

Everyone is talking about the bubble.

Source: TS Lombard

I don’t think growth is any substantial trouble so long as the US government reopens shortly.

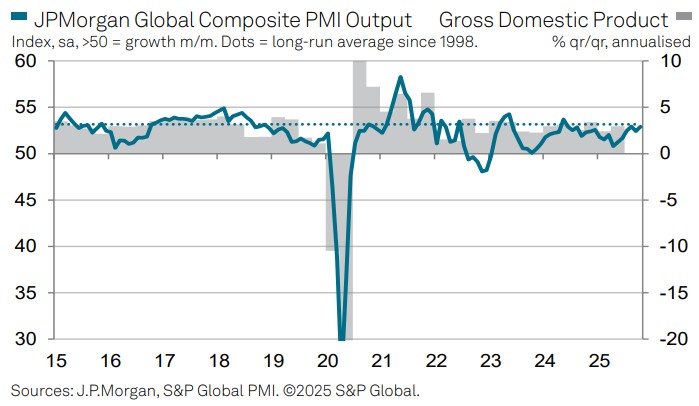

Global PMIs suggest we are still early, not late cycle.

The start of the final quarter of 2025 saw the rate of expansion in global economic activity accelerate, as growth of new work intakes picked up to a 17-month high. Trends in business sentiment and international trade were less positive in comparison, as optimism eased from September’s recent high and new export business contracted at the quickest pace since July.

Growth of incoming new business hit a 17-month high in October, with all six of the sub-sectors covered by the survey seeing expansions. Similar to the trend in output, servicesfocused industries fared better than manufacturers

Markets need to balance AI profits versus AI shocks. We’ve overshot on the former for now.

My best guess is we run again as the Fed cuts on AI job shock.