Lifetime mortgages won’t help housing affordability

A new proposal has been pitched in the United States to address the country’s housing crisis. The Trump administration is working to introduce 50-year mortgage terms for homebuyers.

Instead of the standard 30-year fixed mortgage, payments would be spread across 50 years.

President Trump has framed it as a continuation of the American Dream, likening it to Franklin Roosevelt’s introduction of the 30-year mortgage.

Federal Housing Finance Agency Director Bill Pulte has called the plan a “game changer”.

Since the principal would be amortised over a longer period, monthly repayments would be reduced, making repayments appear more affordable to first homebuyers. As a result, younger buyers and renters would be able to enter the housing market despite high prices and interest rates.

However, analysts warn that lower monthly repayments would inflate demand, pushing home prices even higher. Economists caution that the policy would worsen affordability rather than solve it.

Buyers could also still be repaying mortgages well into their 70s or 80s, making it a lifetime mortgage.

Here in Australia, several lenders have recently begun offering 40-year mortgages, some of which are solely for first home buyers.

One-third of Australian adults polled by Finder said they’d take out a 40-year home loan if it meant lower monthly payments.

Canstar estimated that an individual on a median full-time wage is eligible to borrow up to $24,000 more on a 40-year mortgage than on a 30-year mortgage, while a couple working full-time can borrow up to $48,000 more.

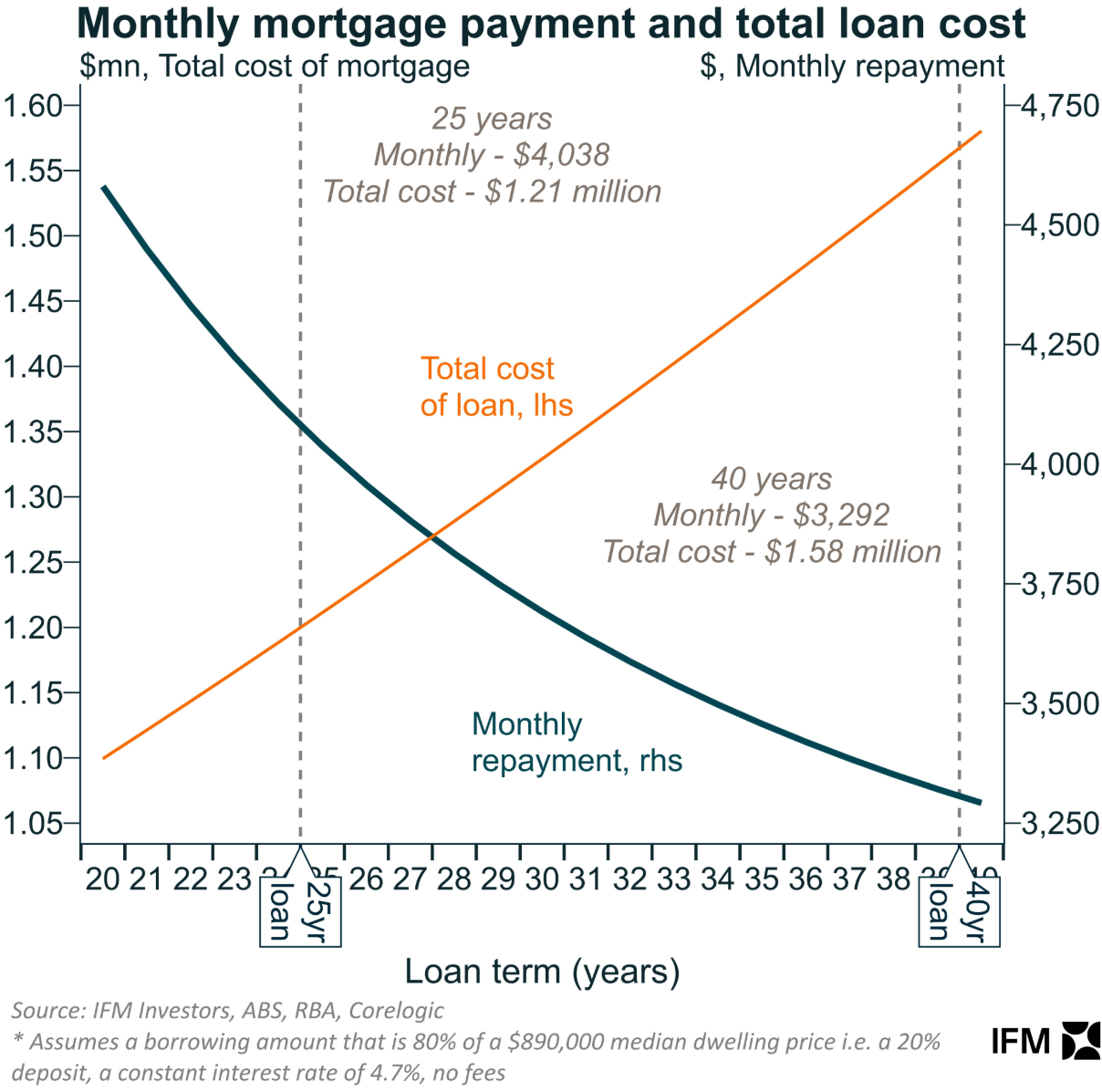

The following chart from Alex Joiner at IFM Investors illustrates how a lengthier 40-year mortgage term increases borrowing capacity.

Longer loan terms lower monthly repayments, but lifetime repayment costs grow, and more Australians will carry mortgage debt into retirement.

The reality is that these types of mortgage reforms will exacerbate the housing crisis and ultimately hinder financial stability and affordability.

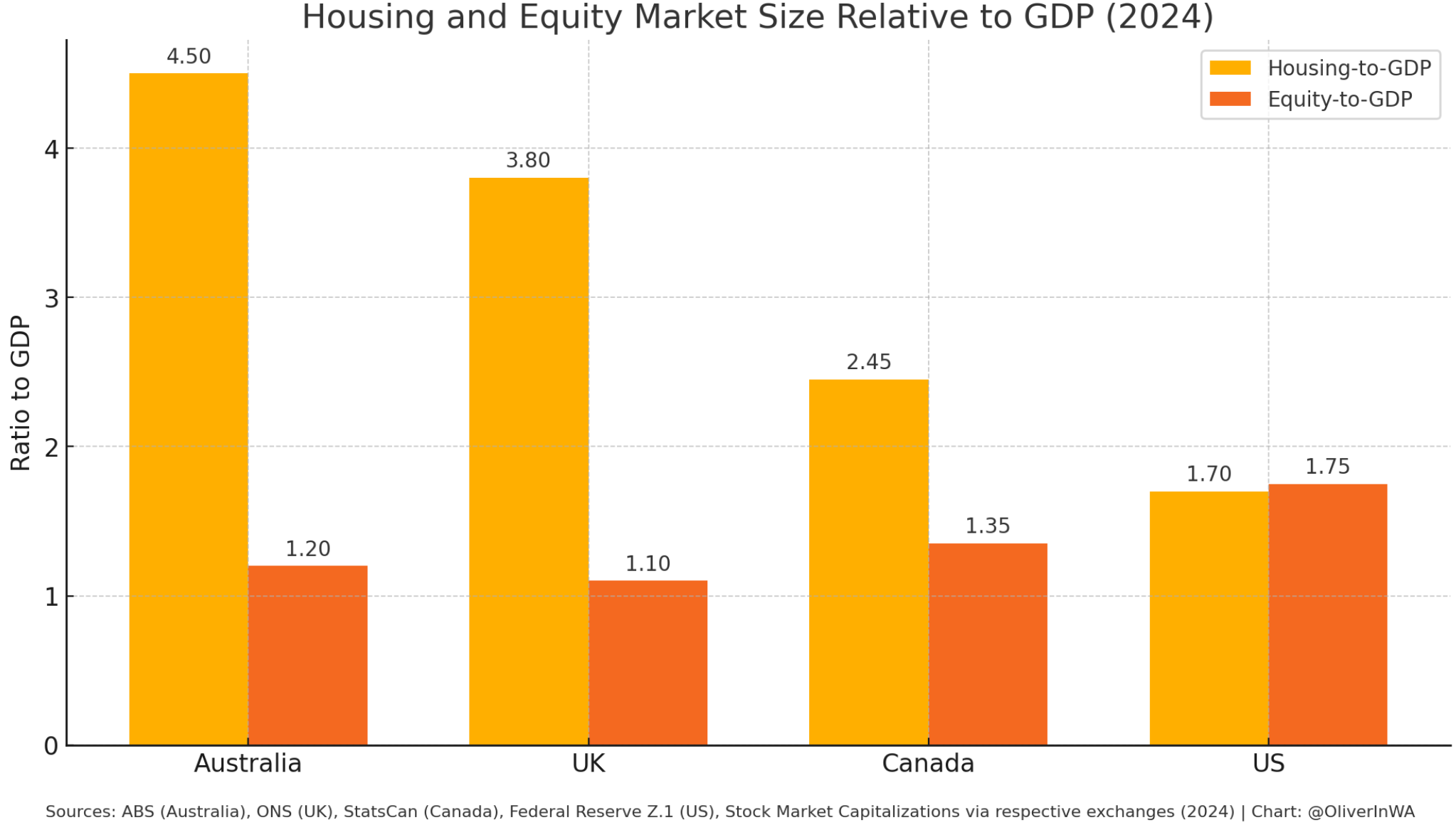

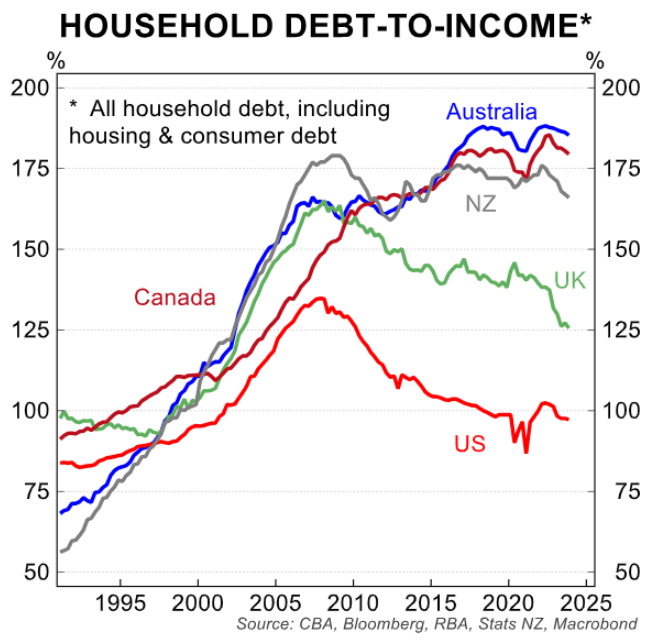

Australia already has one of the most expensive housing markets in the world relative to our economy and household incomes.

Allowing households to borrow more for their homes would achieve the same thing it usually does: increase debt levels and long-term housing costs.

This century has supplied abundant empirical evidence for how the story will conclude. Home prices and mortgage debt will be pushed to new heights.

The last thing that overvalued housing markets need is more mortgage fuel being poured on the bonfire.