By Ashwin Clarke and Lucinda Jerogin, economists at CBA:

Key Points:

- The price of gold has surged to new record highs this month, driven by safe-haven demand.

- Australia is the third largest producer of gold and will be a beneficiary of price improvements.

- Sustained higher gold prices will stimulate mining investment, as well as boost national income and government revenue. This will be a small tailwind to the economic recovery underway in Australia, but is unlikely to move the dial on monetary policy.

- The Commonwealth and WA government will be material beneficiaries of higher prices, with revenue likely at least $1 billion higher annually over the next two years if the current gold price is sustained.

Gold prices surge:

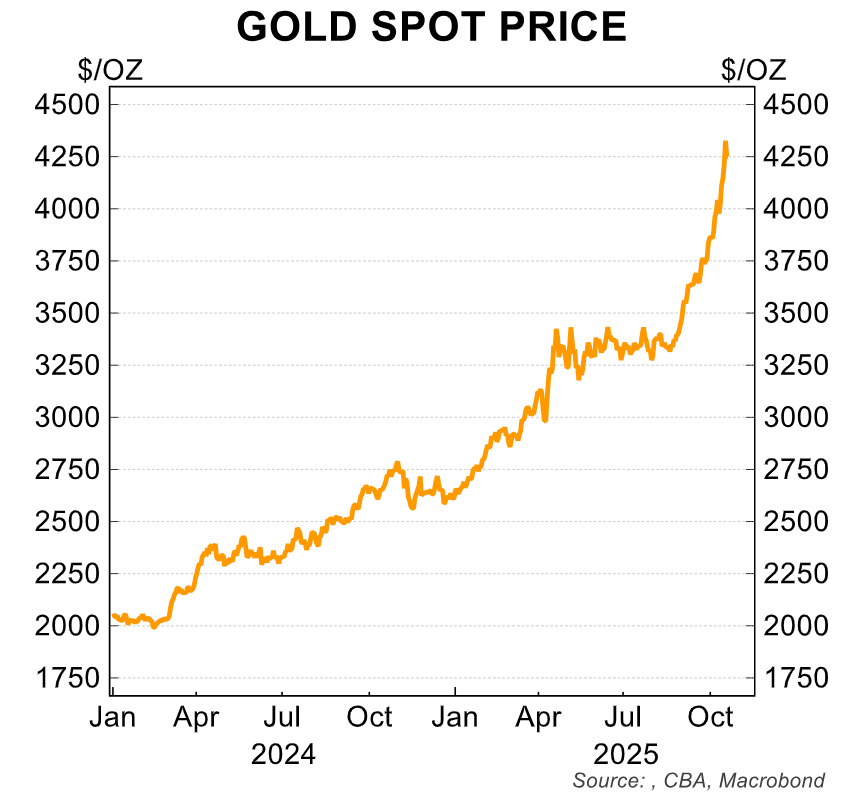

The price of gold has been the obsession of global markets as of late, hitting new record highs daily. The recent boost comes on top of a steady increase over the past two years.

Most recently, the spot price sat at just over US$4,300, more than double the US$1978/oz recorded in Q2 2023 (chart 1).

Safe-haven demand has been a key structural driver of gold this year. The ‘Liberation Day’ tariffs helped gold’s emergence as the preferred safe-haven asset over the US dollar and US Treasuries. Central bank purchasing, geopolitical tensions and lower interest rate expectations have also been key drivers, as our Head of Commodities and Sustainable Economics Vivek Dhar discussed.

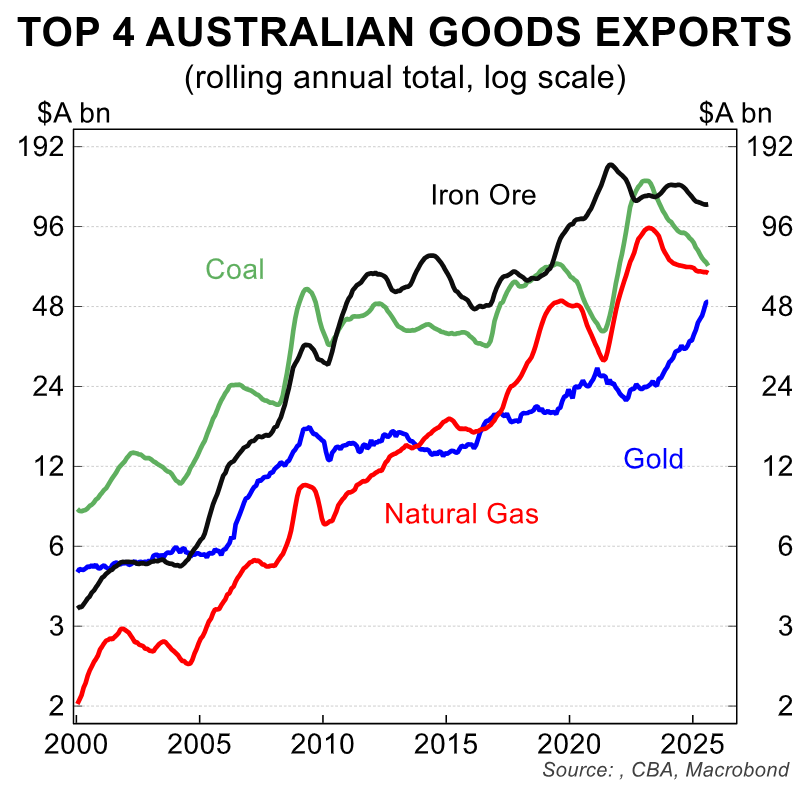

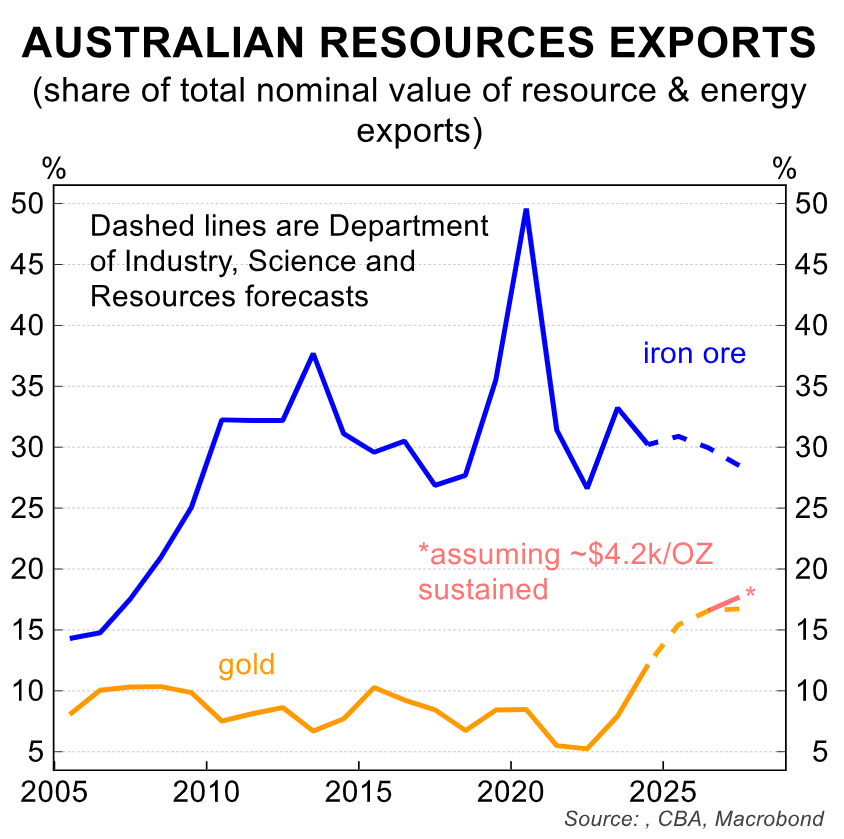

Higher prices have rapidly increased the importance of gold in Australia’s export basket (chart 2).

In October, we expect gold to have surpassed coal as Australia’s second-largest export by value. We expect it to remain Australia’s second-largest export over the next two years if higher prices are sustained.

Australia plays an important role in the gold market:

As the third-largest miner of gold and with one of the largest gold reserves in the world, the Australian economy stands to benefit from recent price gains.

In 2024/25, Australia mined almost 300 tonnes of gold, the majority in WA and most of which is exported. Around ¾ of Australia’s gold exports have ended up in China, the UK, India, Singapore or the US in recent years.

While Australia also imports a large amount of gold, it is a net exporter, with export values over three times larger than imports values in 2024/25.

We expect higher gold prices will transmit through the Australian economy in two ways: higher national income and higher investment.

Higher gold prices will support national income on the margin, especially for the public sector:

Higher gold prices mean higher income for gold miners. The increase in export values from gold prices staying at their current level is expected to be around 0.5% of nominal GDP compared to if they followed the Department of Industry, Science and Resources’ September price forecasts.

Higher gold prices will also boost the trade balance, though the boost in the current account will be lower as some of the income from gold exports will flow abroad to overseas investors.

The higher export values will support miners’ profits and national income, especially the Federal government’s, whose financial position had already surprised to the upside in the most recent final budget outcome.

Using the Federal treasury’s most recent sensitivity analysis as an input, the Commonwealth and WA government revenue will together be at least $1 billion higher annually over the next two years if the current gold price is sustained.

The Federal treasury’s sensitivity analysis assumes some of this response will be offset by a higher exchange rate and hence this is a conservative estimate.

If the exchange rate does not respond, the revenue boost would be larger (more on this below).

For households, higher gold prices will support household wealth and income on the margin through a boost in share prices and dividends.

However, the majority Australia’s mining industry is foreign owned resulting in a large proportion of the higher profits flowing overseas (estimates of foreign share of ownership of the mining sector are as a high as around 80%).

Mining investment will also be boosted, and higher production should follow:

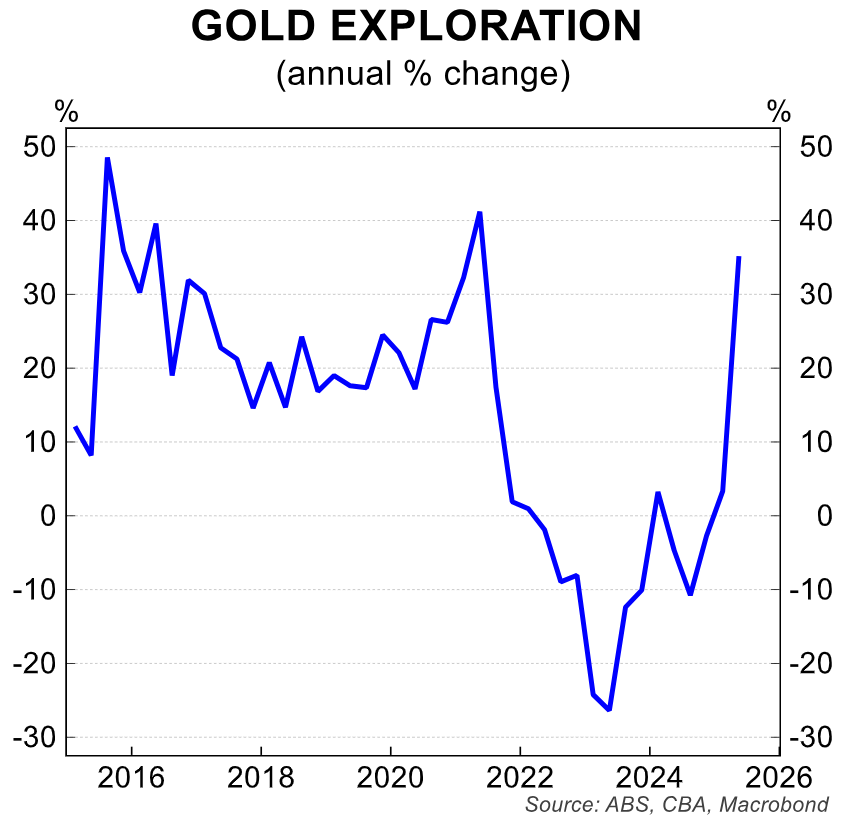

On the investment front, we have already seen gold exploration investment increase substantially over H1 2025 in response to earlier price increases (chart 4).

Gold exploration spending has almost reached the 2021 record high and now accounts for around a third of total spending on mining exploration in Australia. This follows existing plans by miners to significantly expand gold production in coming years.

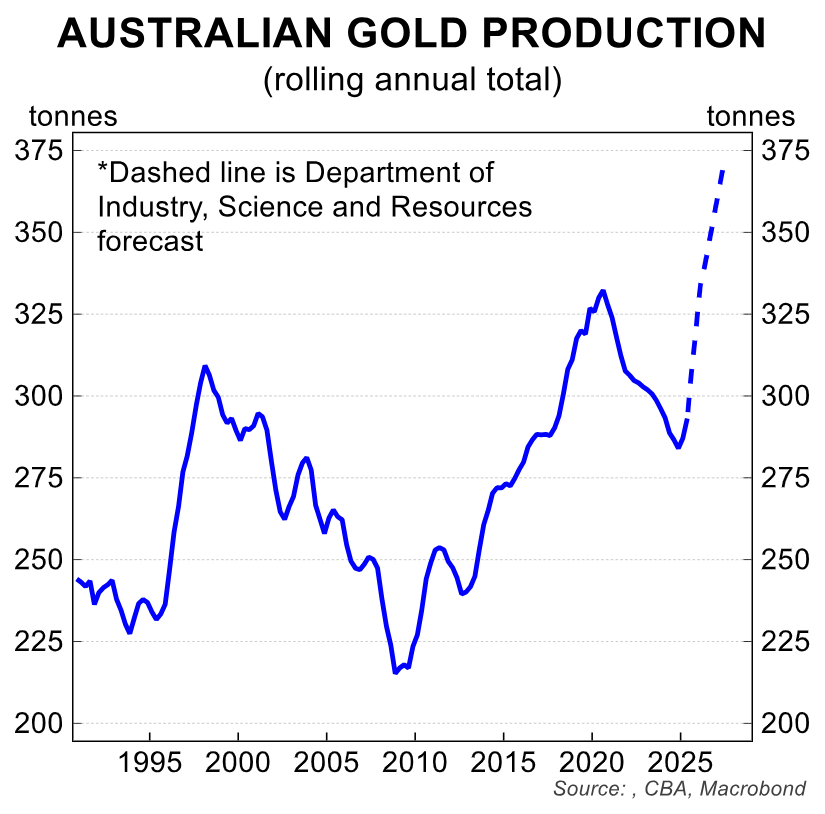

The Department of Industry forecasts gold production volumes to increase by 25% by 2026/27, spurred by new mines and higher utilisation of existing resources, including low grade projects that were previously uneconomical (chart 5).

These investment plans were formed off the back of earlier price increases and hence the recent surge is likely to push exploration and investment even higher. This effect is likely to be most pronounced in WA, where almost 70% of Australia’s gold is mined.

We judge that the increases in investment and exploration, though, are still expected to be modest relative to the very large existing pipeline of mining capital expenditure, although note that most of this is maintenance capex.

While little data is available on capex by commodity, the Department of Industry’s latest list of major projects showed gold projects accounting for only 10% of capex on the list.

Altogether the boost to the economy from higher gold prices is expected to be modest:

All in all, the recent surge in the price of gold will likely be a small tailwind to the economic recovery underway in Australia. Favourable prices will support export revenue and encourage increased investment.

However, the additional investment and small gains to national income will likely be swamped by other major economic drivers in the Australian economy.

Specifically, the pickup in household consumption, the future path for inflation and any challenges emanating from the uncertain geopolitical environment abroad.