From the Market Ear:

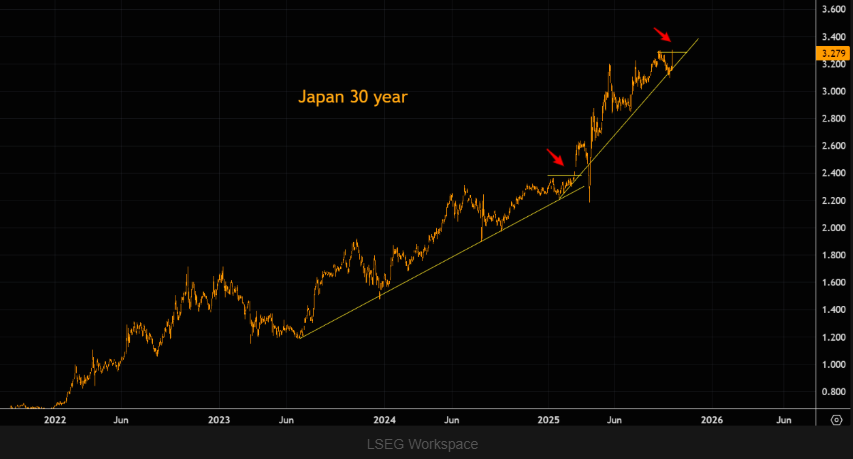

Kamikaze

The Japanese 30 year has risen sharply over the past few years. Is this a similar break out move like we saw earlier this year?

Gold loves it

Gold loves rising Japanese 30 year yields…

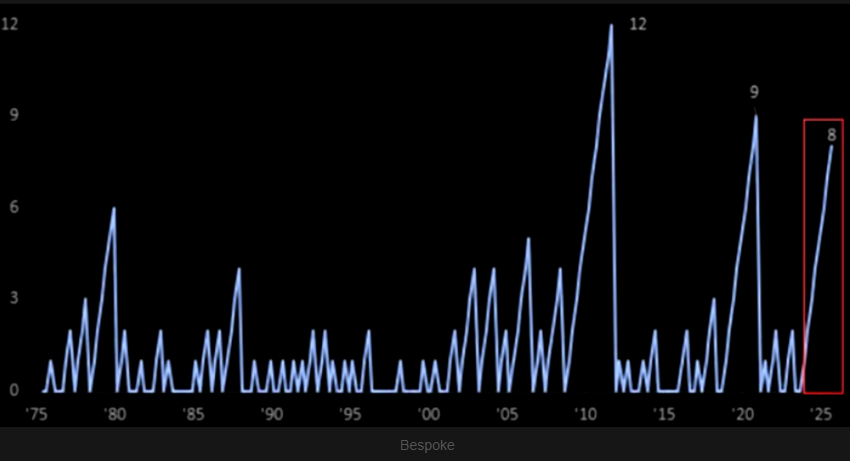

The streak

Gold prices have now posted their 8th consecutive quarterly gain, the third-longest streak on record. This trails only the 9-quarter run in 2019-2020 and the record 12-quarter streak from 2009-2011. Over this stretch, gold prices have surged +108%, the biggest rally since March 1981.

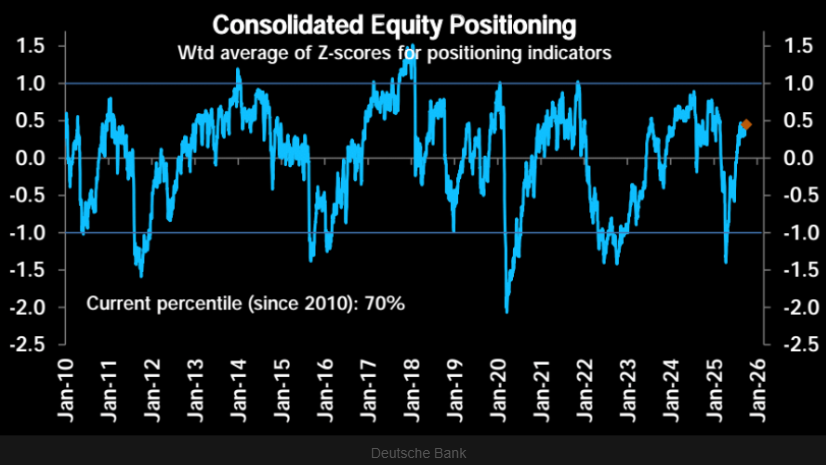

Overweight – not morbidly obese

Deutsche Bank: “Equity positioning is overweight but not yet stretched in our reading.”

Will they buy even more?

S&P realized vol has fallen below 10% — its lowest since Jul-24 and in the 3rd percentile since 2020. This matters because the impact of each 1% drop gets nonlinear at low levels:

A drop from 20% → 19% raises leverage in a 10% vol-control strategy by ~2.6%.

A drop from 10% → 9% raises leverage by ~11%.

If realized vol falls further, it could trigger significant incremental buying from vol-control funds, acting as a positive tailwind for the S&P in the near term. (BofA derivs)

Why so low SPX?

SPX loves falling bond volatility. Note the MOVE is “suggesting” the SPX should take out new ATHs imminently.

Sexy SOX

SOX at the most overbought levels since late 2017.

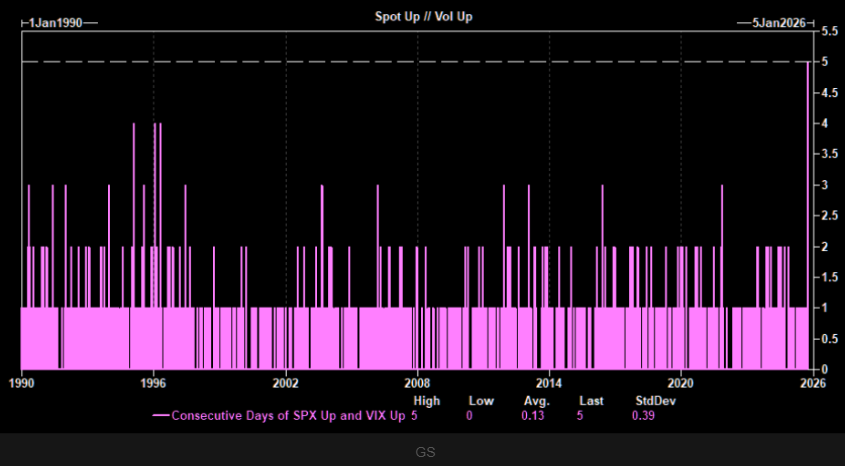

Never happened before

Spot up, volatility up in a pic. Goldman’s derivatives guru, Cullen Morgan: “…past week saw SPX green five days in a row for a return +1.09%… At the same time, VIX Index was up 1.36 points, ALSO notching five consecutive days higher… since the creation of VIX in 1990, this has never happened before.”

European assets are experiencing a revival

“European assets are experiencing a revival, buoyed by a falling risk premium. Policy changes in Germany, a Fed pivot, and global portfolio diversification are making European assets a rewarding source of diversification. The southern periphery (Italy, Spain, Portugal, Greece) is leading the way on the back of falling credit risk (further credit rating upgrades), explaining the outperformance of financials and banks.” (Soc Gen)

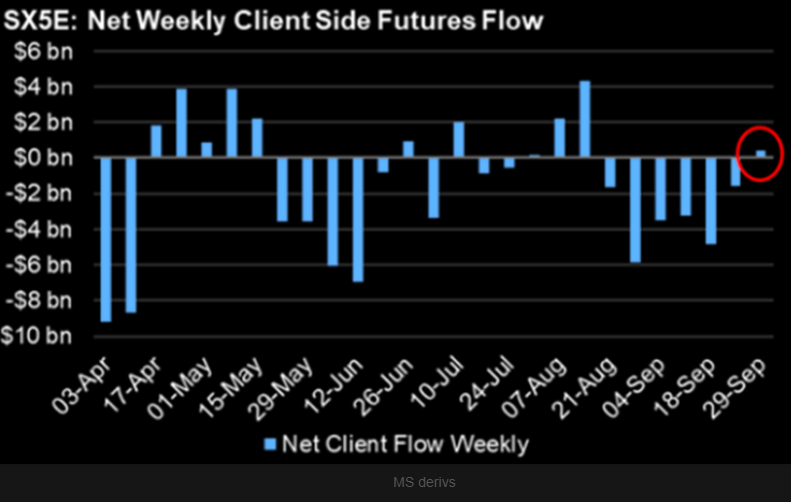

Room to get pulled back in

Chart shows weekly futures buying of Europe by Morgan Stanley clients.