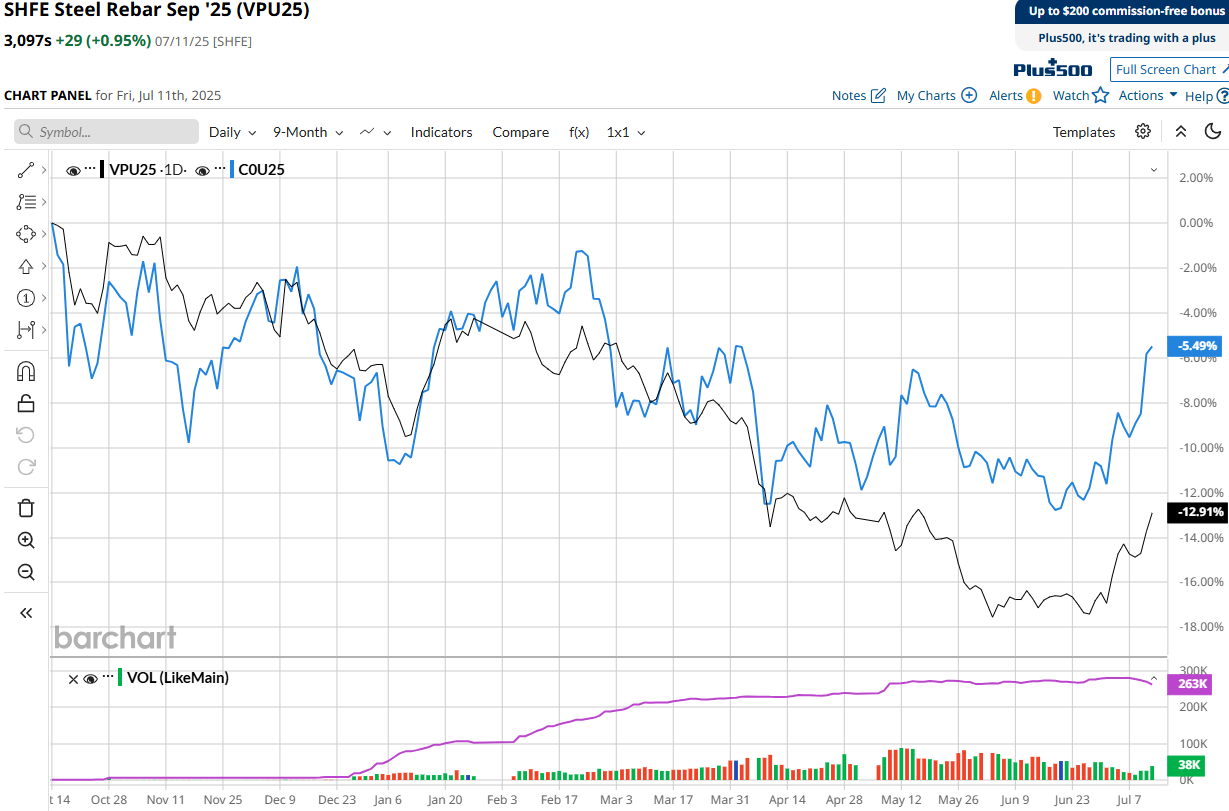

Markets are so fun sometimes. Iron ore is in all sorts of trouble, but traders love to push a counter-trend rally.

The latest MySteel data is still down as expected.

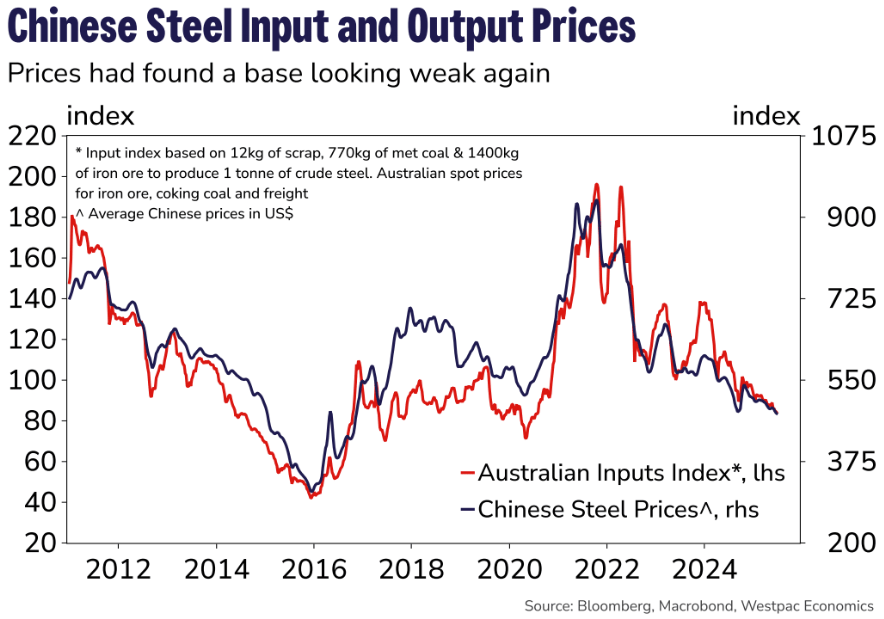

Westpac sums it beautifully.

Iron ore has been incredibly stable

A good example of why to stay calm has been the relative lack of volatility in iron ore prices.

This comes despite the ongoing uncertainty over tariff policies and their impact on global trade and economic growth.

There is also uncertainty over the strength of China, which purchases about 75% of global seaborne iron ore volumes.

Overall, we are in a slightly surreal situation for iron ore where the demand fundamentals are clearly deteriorating but it appears that traders are waiting for additional policy stimulus at the next Politburo meeting, likely to be in the 3rd week of July.

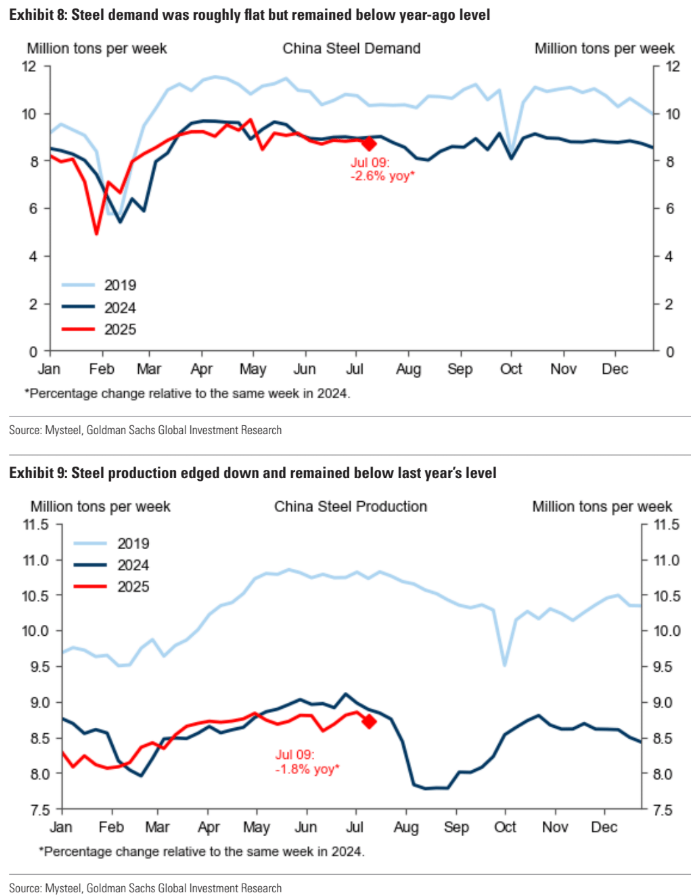

Chinese steel production has been supported by a record amount of steel being exported to the rest of the world through the first five months of this year.

Nevertheless, CISA data suggests the weakness seen in steel production in April and May has continued into June.

When you also consider that steel production in the Hebei, Shanxi, Yunnan and Guizhou provinces is being actively curtailed, along with robust supply from the seaborne trade, we continue to expect the price of 62%fe to drop below US$90/t and be down to around US$86/t by year end.

Steel supply-side reform can be price-positive for iron ore if the market is in deficit.

But if it is in oversupply, the opposite applies. It is even more price-negative.

This is a marvelous chance to take bearish positions as we push into the age of the Pilbara killer.