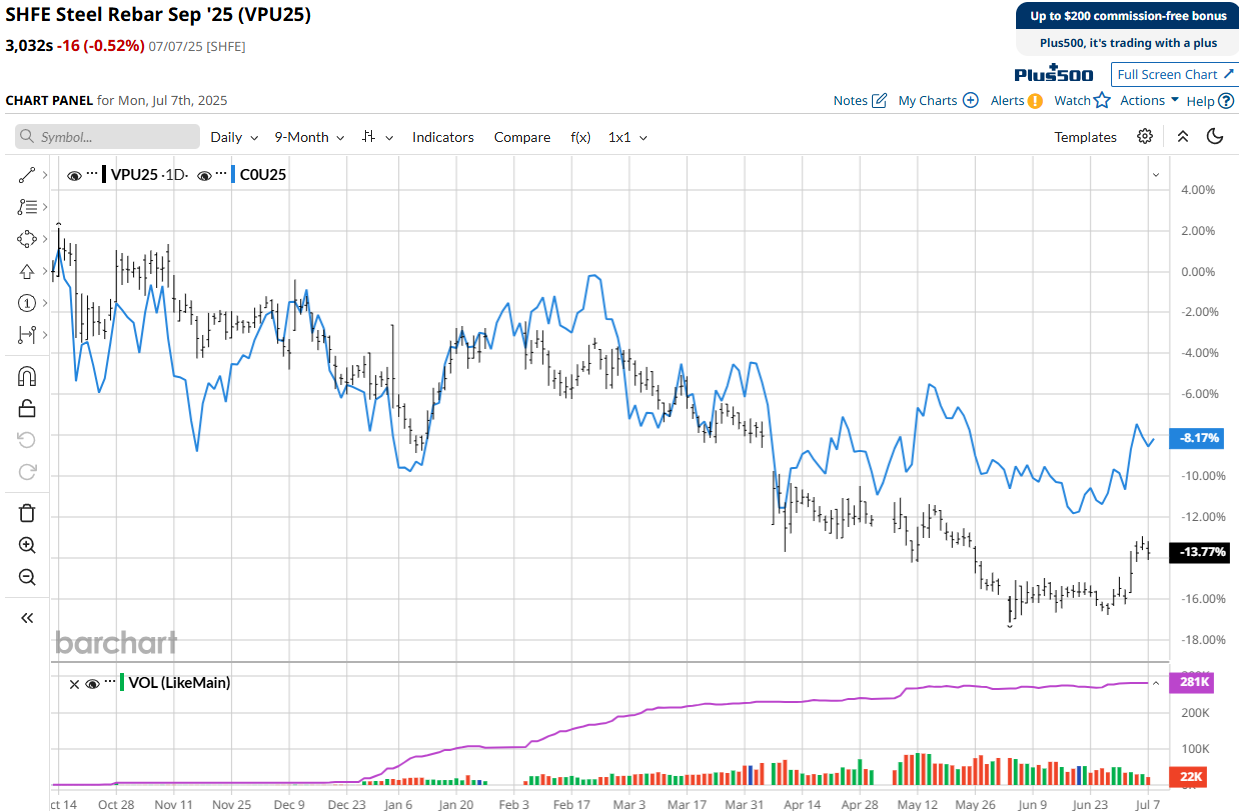

The ferrous market is not a strong believer in Chinese steel production cuts so far.

Scuttlebutt is building, though.

Steelmakers in northern China’s Tangshan city have received notice for environmental protection-related production control, information provider Tangshan Baochun Data said in a note on its WeChat account on Saturday.

Some local mills have undertaken maintenance on parts of their sintering equipment, Tangshan Baochun said, while analysts noted that the move is expected to dampen demand for iron ore.

…Over the weekend, Malaysia said it has imposed provisional anti-dumping duties ranging from 3.86% to 57.90% on certain iron and steel imports from China, among others.

…Average daily hot metal output, a gauge of iron ore demand, still hovered at 2.41 million tons, as of July 3, and were higher than the same period a year before, despite signs of softening, data from consultancy Mysteel showed.

We are getting almost daily reports of new duties and tariffs placed upon Chinese steel around the world, so a production cut makes sense.

It will lift the price of steel at home and cut off some of those exports. Goldman,

There have been signs of renewed policy focus in addressing supply discipline, as indicated by the readout of the sixth meeting of the Central Financial and Economic Affairs Commission on July 1st.

The meeting reiterated the need for China to develop a “unified national market”, explicitly calling for a crackdown on overly intensive competition between firms that has caused lower prices.

An orderly exit of obsolete industrial capacity was also stated.

We think it is still too early to sense the policy direction as supply side reform or reprieve.

However, the direction of travel towards capacity cuts instead of just curtailment is positive, and a more supportive policy environment on supply discipline could benefit industries with pre-formulated supply plans, including China’s steel and cement sectors, in our view.

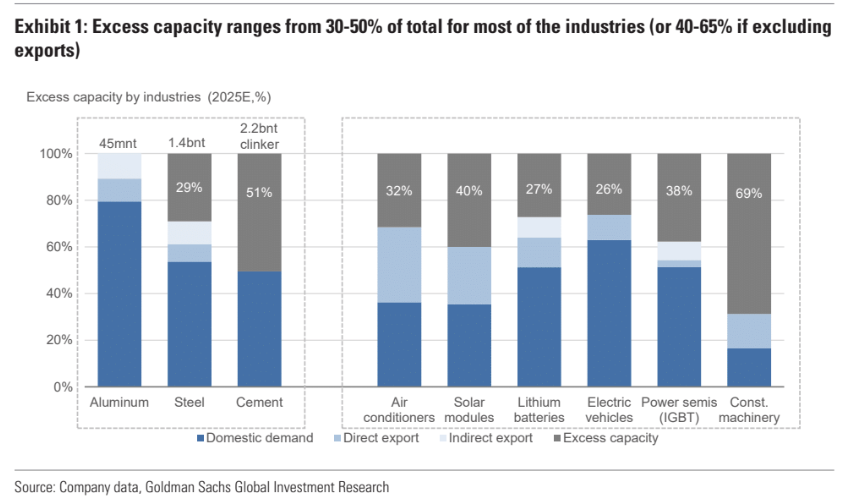

The amusing thing is that even a 5% cut would hardly scratch the surface of the steel oversupply.

One also wonders if many of the cuts wouldn’t transpire in EAF, where output has been falling since COVID, though this would certainly work against any long-term climate goal.

After the May shocker, steel output is down 2.7%YTD. Any cut to production for H2 demanding 5% down over the full year would necessitate cuts to output in the range of 50mt in H2.

This is nearly 100m less iron ore across June and H2 if it is all BOF.

Headed into Simandou, any brief rise in iron ore chasing higher steel prices is a glaring short.