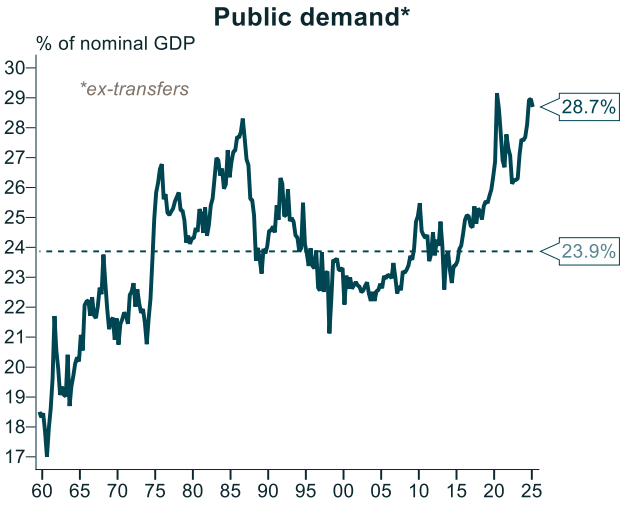

Last week’s Q1 national accounts release from the Australian Bureau of Statistics (ABS) showed that Australia’s economy remains on life support, driven by historically high population growth and public spending.

Source: Alex Joiner (IFM Investors)

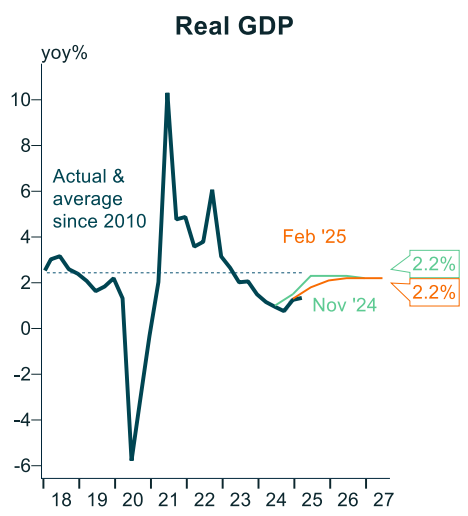

Australia’s aggregate GDP grew by only 0.2% in Q1 2025, less than half the 0.45% growth tipped by the Reserve Bank of Australia (RBA) in its latest Statement of Monetary Policy.

Source: Alex Joiner (IFM Investors)

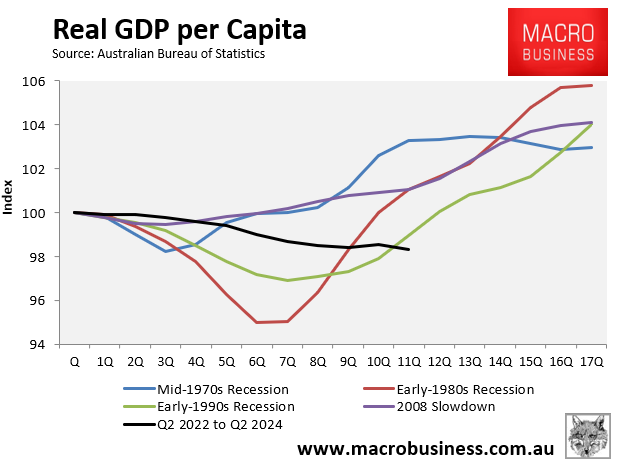

Australia’s per capita GDP also declined by 0.2% in Q1 2025, representing the ninth decline in eleven quarters and the longest (but not deepest) recession in modern history:

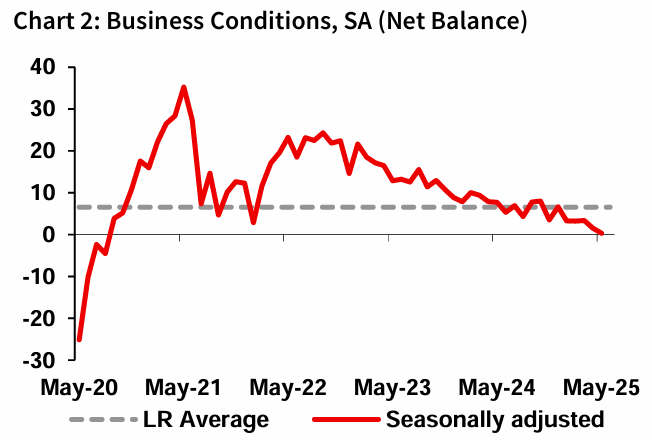

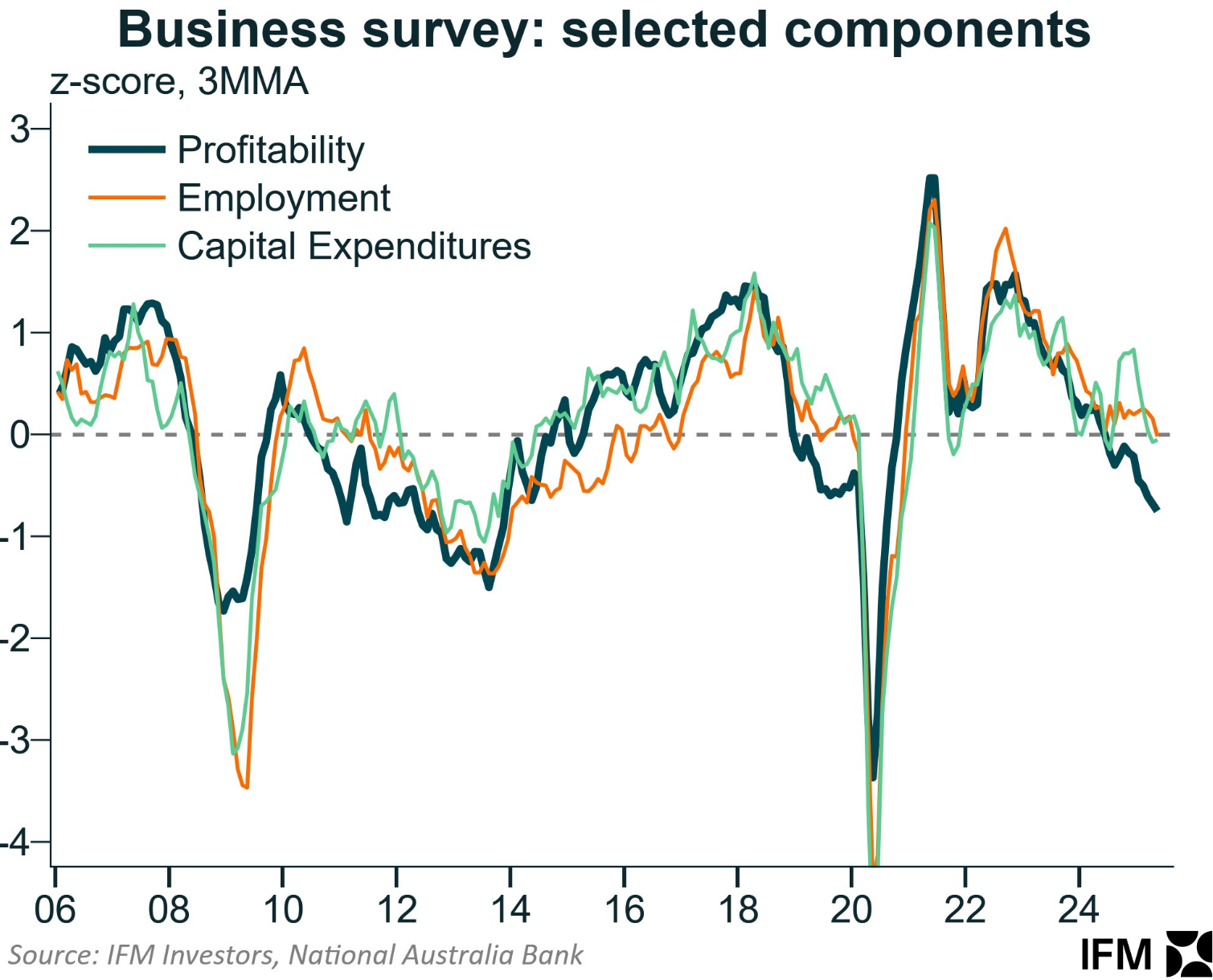

The NAB business survey was released on Tuesday, which showed that business conditions have collapsed:

Australian businesses reported the weakest business conditions—a composite measure of firms’ reported trading conditions, employment, and profitability—since 2014 in May, excluding the pandemic period.

As illustrated below by Alex Joiner from IFM Investors, profitability has collapsed, which has pulled employment and capital expenditures lower:

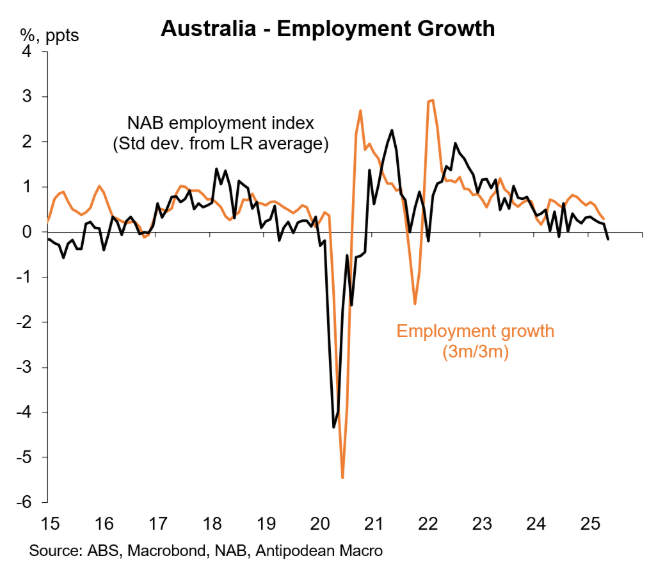

Indeed, the following chart from Justin Fabo from Antipodean Macro shows that reported hiring declined in May to be below average levels:

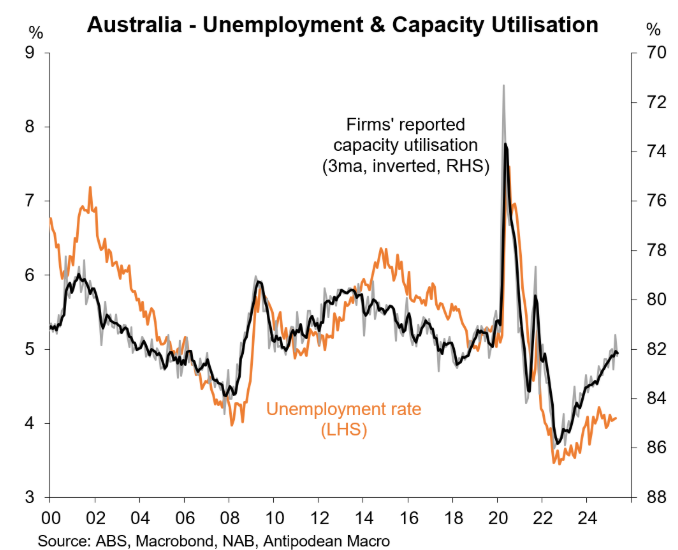

Capacity utilisation has also fallen heavily, which typically corresponds to rising unemployment:

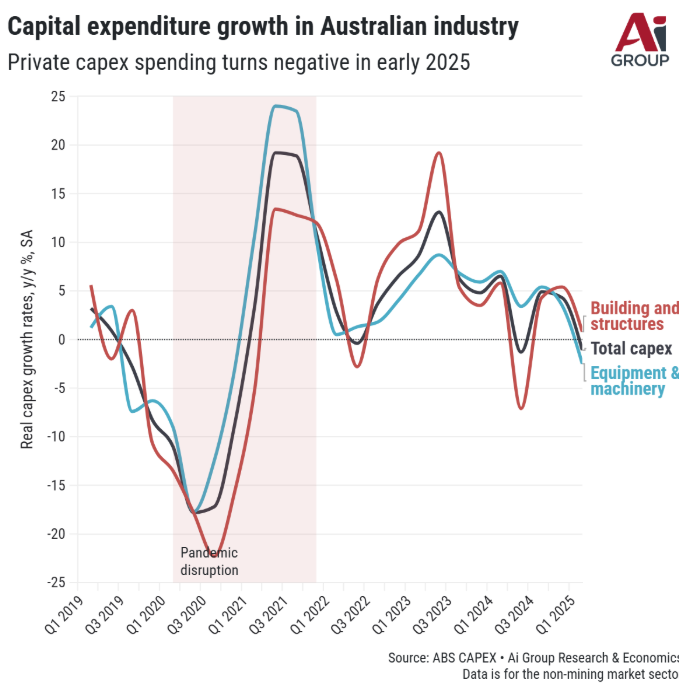

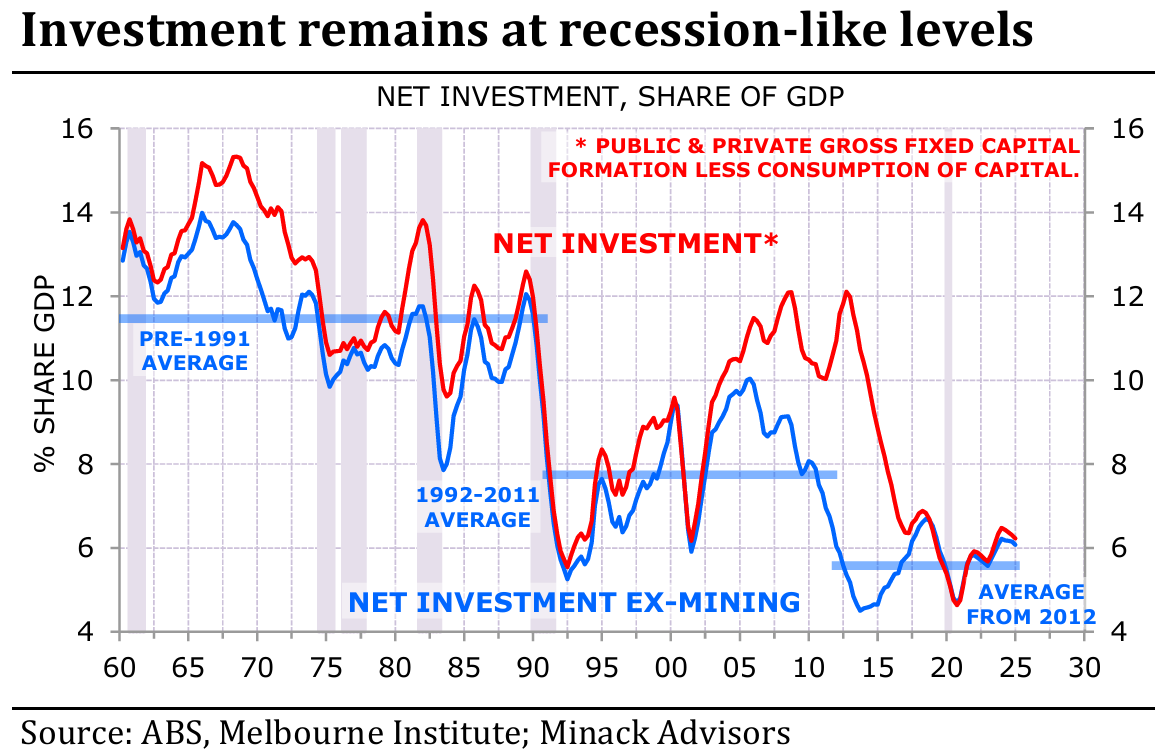

Arguably, the most concerning theme is the slump in capital expenditures, which were also captured in the Q1 capex release from the ABS:

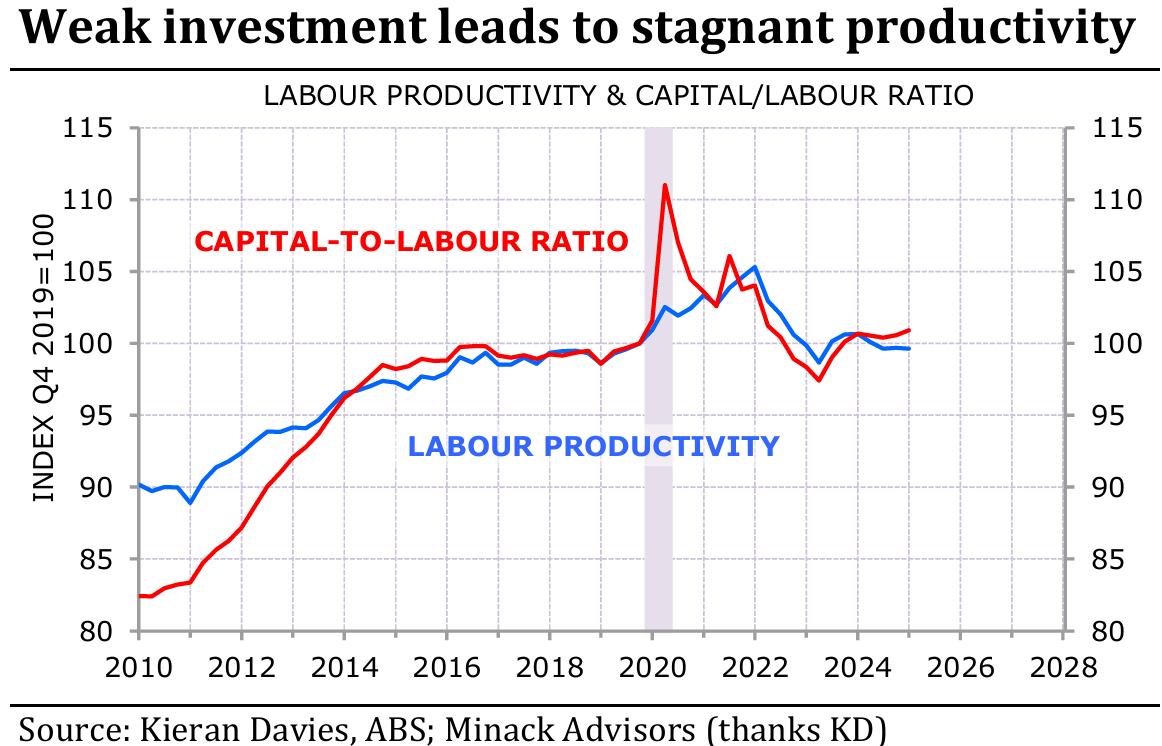

As noted by this week’s seminal report by leading independent economist Gerard Minack, “low investment and fast population growth prevent capital deepening and productivity growth. The result is stagnant real incomes and falling per capita GDP”.

Australia’s net investment is tracking at recessionary levels at the same time as the population continues to expand aggressively, resulting in “capital shallowing” and declining productivity growth.

The upshot is that Australia has a low-productivity “zombie” economy that is only expanding courtesy of historically high population growth and government spending.

In contrast, the private sector and per capita economies continue to stagnate, and the NAB survey and ABS capex data indicate that this situation is unlikely to change in the near future.