Minack: Aussie interest rates about to crater below zero

Gerard Minack destroys Australia’s sick economy.

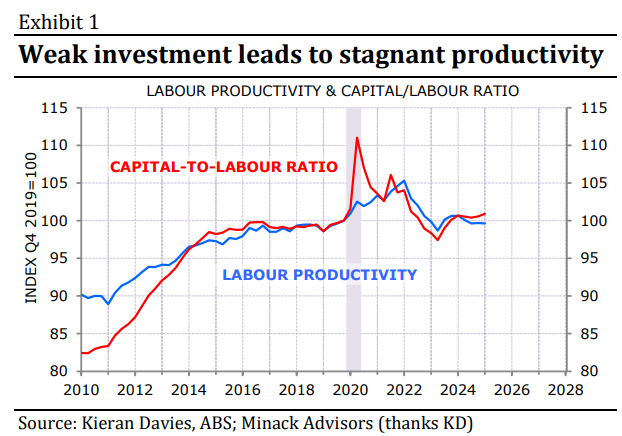

Australia remains stuck in a macro rut. Low investment and fast population growth prevent capital deepening and productivity growth. The result is stagnant real incomes and falling per capita GDP. This malaise is also reflected in anaemic corporate earnings, but not in the equity market’s premium valuation. The RBA has room to keep cutting, but that will provide only symptomatic relief to what are structural, not cyclical, problems. Australia’s GDP is stagnating. Per capita GDP has grown in only one of the past 11 quarters. The key problem is flat-lining productivity, and that reflects the lack of capital deepening (Exhibit 1).

In turn the lack of capital deepening reflects low investment spending and fast population growth. Through the past dozen years the non-mining investment share of GDP has averaged a level only previously seen at the worst point of Australia’s worst post-war recession, in the early 1990s (Exhibit 2).

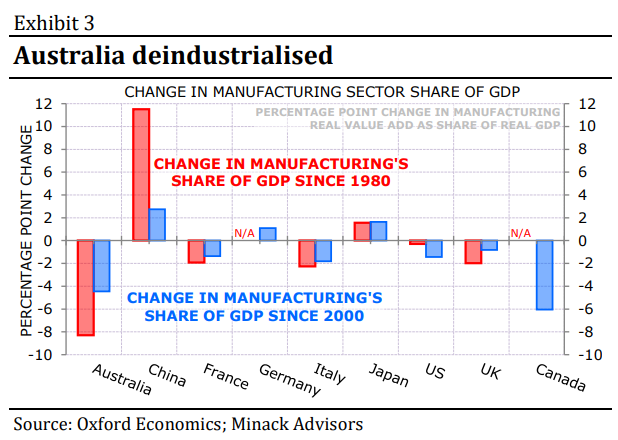

There are many reasons for low investment spending. First, the fast population growth: labour is cheap and plentiful so there is not much incentive to undertake labour-replacing investment. Labour replacing investment is the same as productivity enhancing investment. Second, Australian manufacturing – a capital-intense sector – has been decimated through the past 45 years (Exhibit 3). Mining is capital intensive, but since 2018 mining net investment share of GDP has averaged 0.1%.

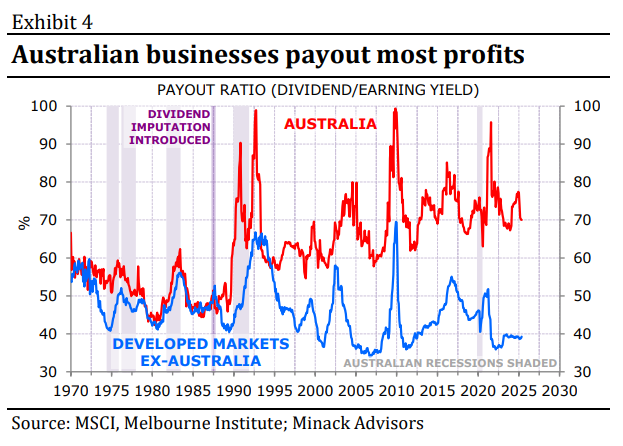

Third, many Australian sectors have oligopolistic structures which blunt the need for innovation or investment. Fourth, Australia’s franking system – which effectively provides dividends tax free to domestic shareholders has encouraged structurally high payout ratios for Australian business (Exhibit 4). Shareholders prefer firms to pay dividends, not to invest.

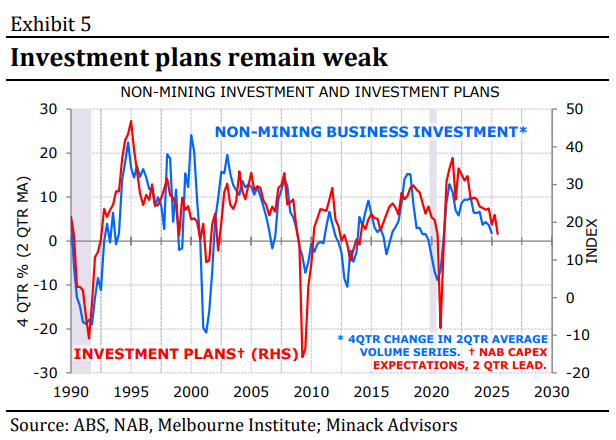

There’s no sign that the investment malaise is about to end. There are few signs of domestic capacity shortages outside of construction, the Trump Administration is creating global uncertainty, and leading investment indicators are soft (Exhibit 5).

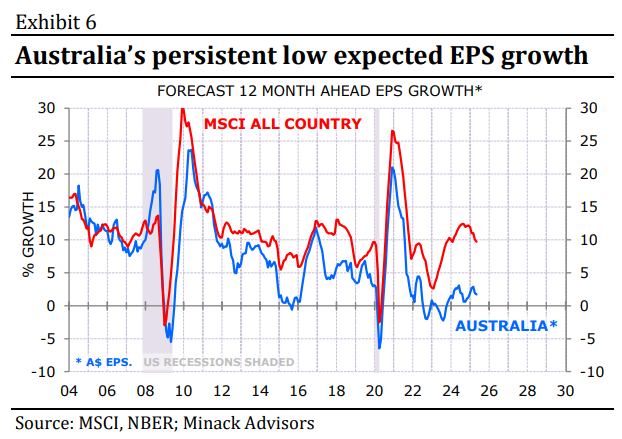

It is true that the stock market is not the economy. But the fact is that Australia’s macro stagnation has coincided with a period of low EPS growth. Aside from the pandemic reopening surge, Australia’s nominal EPS growth has remained mid-to-low single digits since 2017 (Exhibit 6).

Low earnings growth is not reflected in equity market valuations. Exhibit 7 provides a snapshot of expected EPS growth (horizontal axis) and equity valuation (prospective PE, vertical axis). Investors pay more for markets with fast EPS growth, who knew? But Australia stands out. As one client noted, Australia offers European-style growth at a US-style multiple. Which is actually rude to Europe, where EPS growth is expected to be over three times higher than Australia.

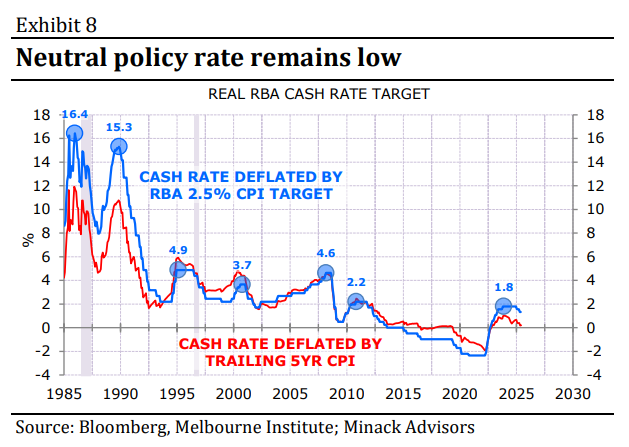

The high valuation on Australian equities may reflect domestic investors willingness to pay a premium to access high tax-advantaged dividend yields. It may also reflect the pressure-cooker effect from Australia’s enormous compulsory investment savings. From a foreign perspective, however, it is an unenticing mix of low growth and high value. The RBA is easing policy. There is plenty of room to cut. In real terms the cash rate was zero or negative for 6-7 years before the pandemic (Exhibit 8).

There was no evidence that a zero real cash rate was stimulative. Inflation and wage growth persistently fell below official forecasts. If the neutral rate remains zero or less in real terms – and I don’t see any reason it should have risen – then the RBA can cut the nominal rate to 2½% or less once it is sure inflation is heading to target. This will provide modest cyclical stimulus, but low rates will not fix Australia’s structural problems.

And there you have it.