The ferrous complex is hardly inspiring confidence. Steel output cuts should eventually force more price weakness upstream to iron ore.

Meanwhile, Goldman has finally cottoned on to the structural nature of the Chinese property crash. It is forever.

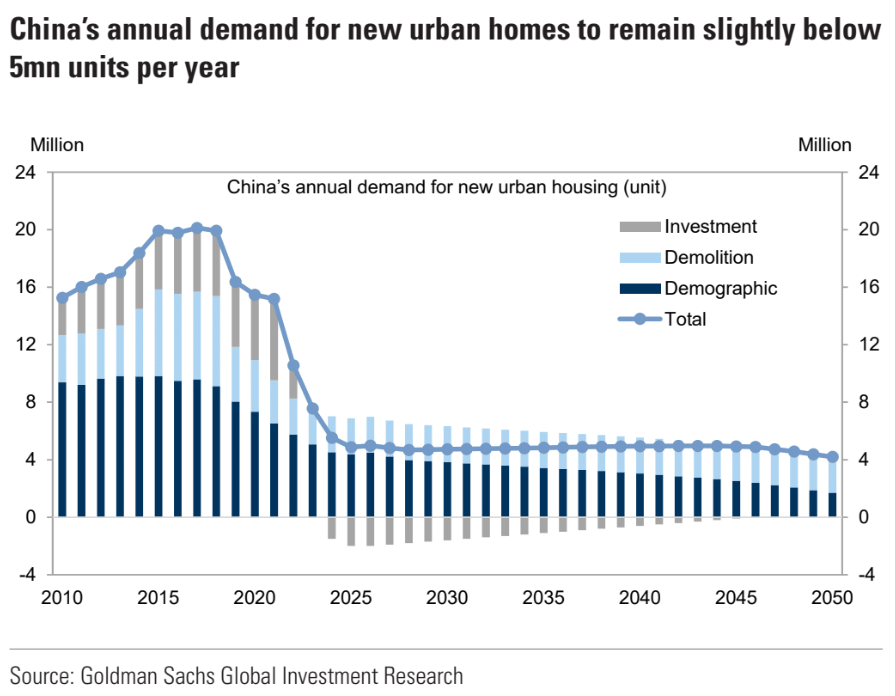

Gauging China’s new urban housing demand: In a recent comprehensive update, we re-examine China’s underlying demand for new housing units in coming years.

In particular, we incorporate the fact that investment demand in China could turn negative as owners sell vacant apartments, and that the 2015-18 government-led shanty-town redevelopment should result in fewer demolitions in subsequent decades.

We estimate that China’s urban demand for new properties is likely to remain slightly below 5mn units per year in the foreseeable future, 75% below its peak of 20mn in 2017.

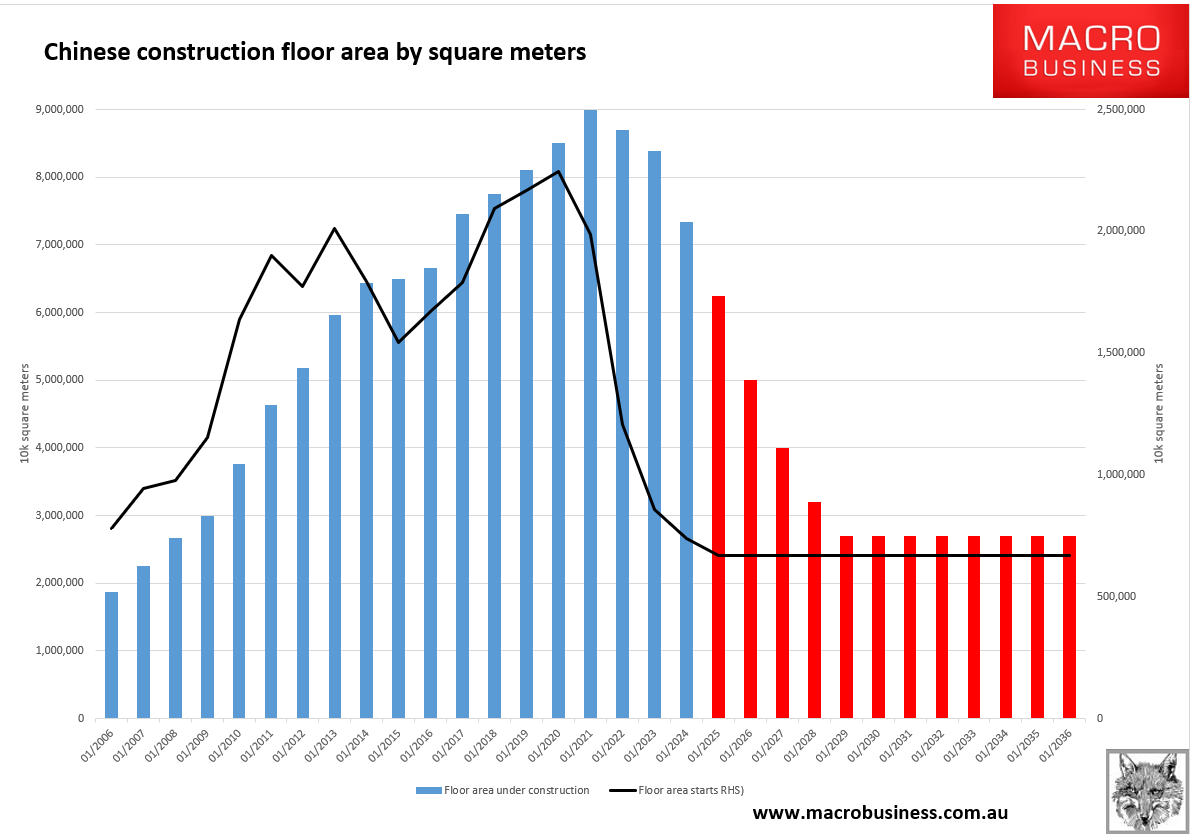

Starts are down 75% already. But given sales are only down by half, this suggests that the bust has a long way to go before China fully capitulates.

Given empty, half-build, unsold, idled and grown-over inventory is still immense, there is every prospect of ongoing construction volume falls as Goldman’s investors sell into a glutted secondary market where prices no no bottom.

It was a once-in-a-millennium boom, and likewise the bust.