New Zealand experienced one of the world’s biggest house price booms over the pandemic, with prices soaring by around 30%.

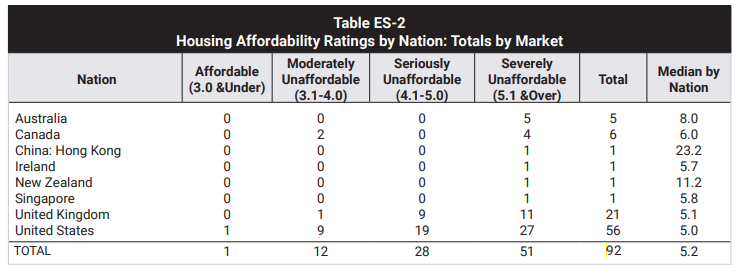

As a result, the 2022 Demographia Housing Affordability Survey ranked New Zealand as having one of the world’s most expensive housing markets, with a median multiple of 11.2 in 2021.

Source: 2022 Demographia Housing Affordability Survey

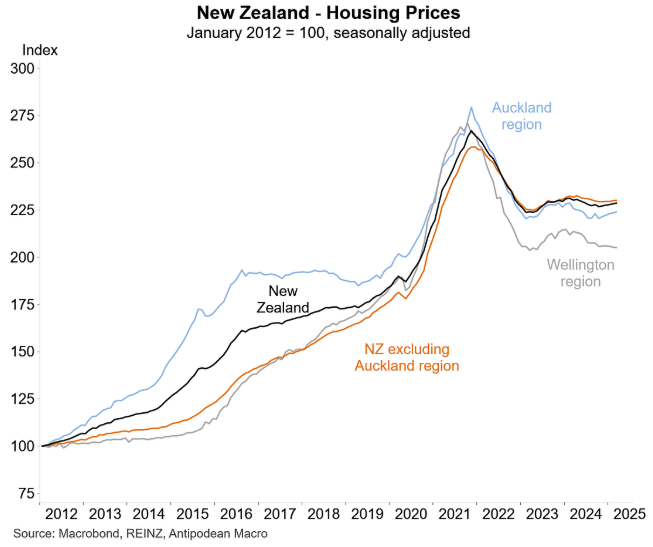

New Zealand’s market has since experienced a house price ‘crash’.

As Justin Fabo from Antipodean Macro illustrated below, home prices across New Zealand have fallen significantly from their peak.

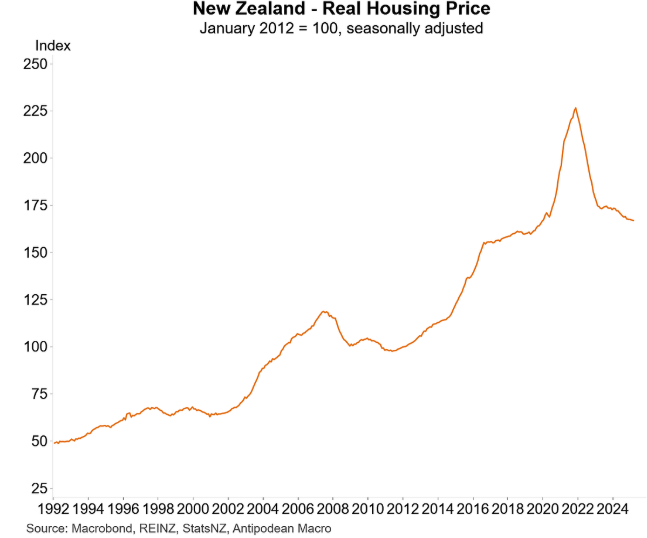

In real inflation-adjusted terms, New Zealand’s median house price has returned to pre-pandemic levels.

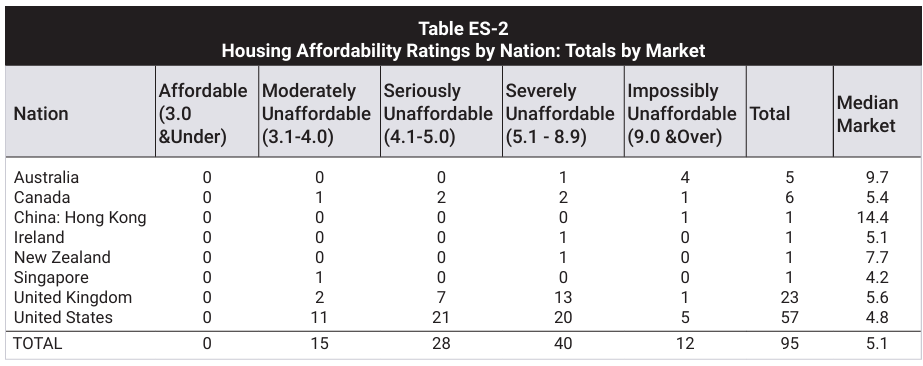

As a result, Demographia’s 2025 housing affordability survey shows that New Zealand’s median multiple had fallen to 7.7 in 2024, down from 11.2 in 2021.

Source: 2025 Demographia Housing Affordability Survey

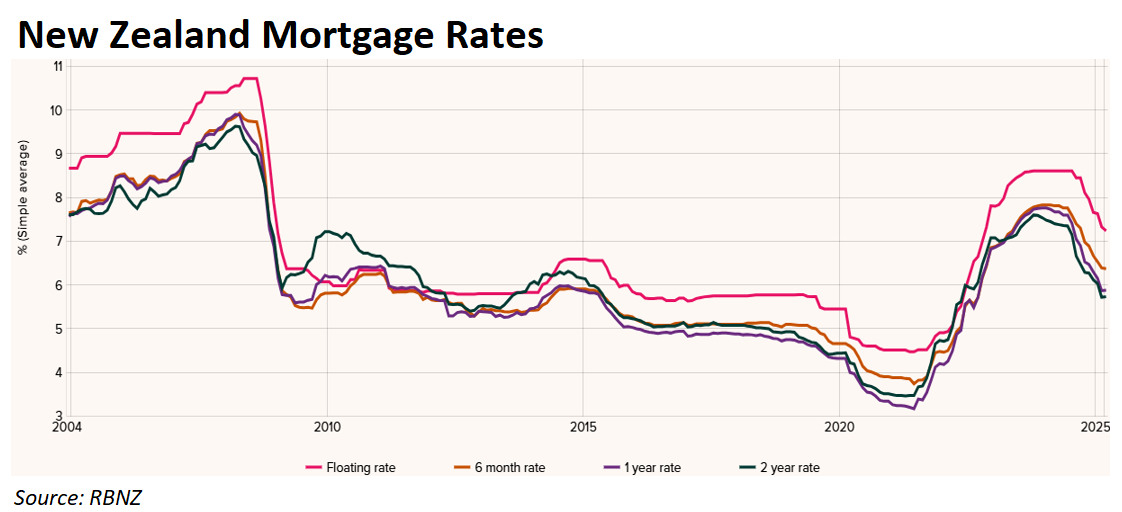

New Zealand mortgage rates have declined dramatically following the Reserve Bank’s 2.0% monetary easing.

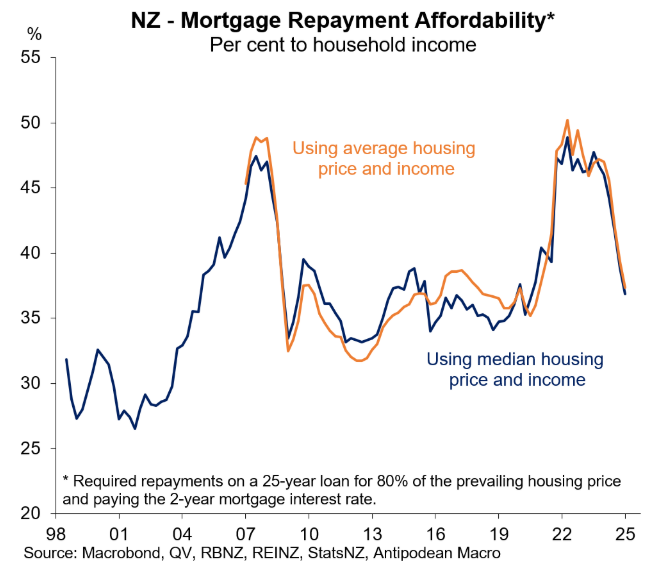

Lower home prices and interest rates have significantly increased mortgage affordability.

Mortgage repayments as a percentage of household income have declined from around 50% to just over 35%.

As a result, New Zealand home buyers are in the box seat, with vendors cutting prices and mortgage interest rates falling.

Contrast New Zealand with Australia, whose median multiple has increased from 8.0 in 2021 to 9.7 in 2024, according to Demographia.

Australia’s mortgage affordability is also tracking near its worst level in history.

If housing affordability is to improve, lower prices are necessary. New Zealand’s politicians seem to understand this concept.

Unfortunately, Australia’s politicians do not share this view and continually implement stimulatory policies to boost mortgage demand and prices.