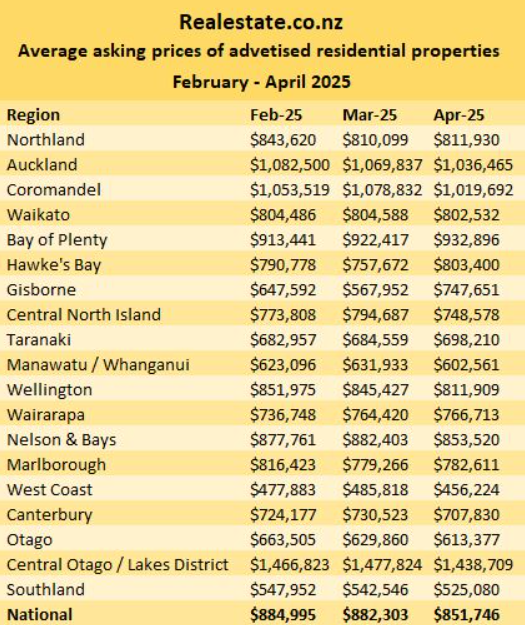

I reported last week on the latest results from Realestate.co.nz, showing that the national average asking price of homes listed on the site declined for the second consecutive month in April to $851,746, down 3.8% from $884,995 in February.

The decline in prices was attributed to a growing glut of homes listed for sale, which have have more than doubled in the past four years.

“There’s plenty of stock on the market, but we’re not seeing a boom in sales activity to move it through yet”, Realestate.co.nz Chief Executive Sarah Wood said.

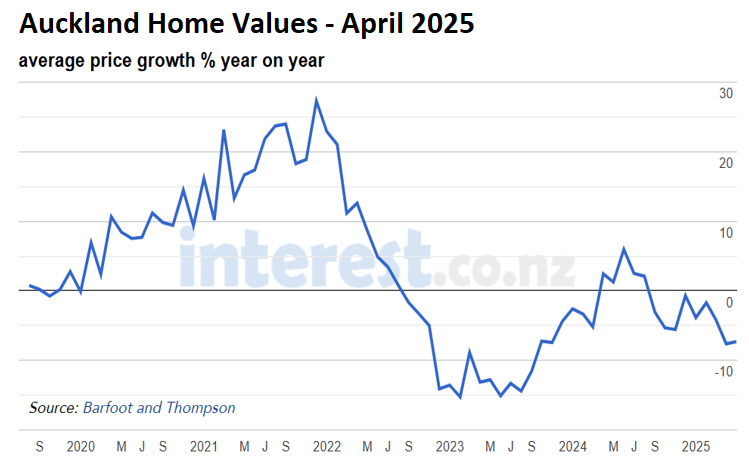

On Monday, Auckland’s largest real estate agency, Barefoot & Thompson, reported a median selling price of $934,000 in April, a decline of $36,000 (-3.7%) from March and $73,500 (-7.3%) lower than in April last year.

That was the lowest median selling price in the month of April since 2020.

The average selling price was $1,110,689 in April, down by $34,356 (-3.0%) compared to March and $102,139 (-8.4%) lower than in April last year.

The decline in prices followed a surge in for sale listings, which were the highest for April since 2008, putting stock levels at a 17-year high.

“From a price perspective, the market showed no signs of lifting”, Barfoot & Thompson Managing Director Peter Thompson said.

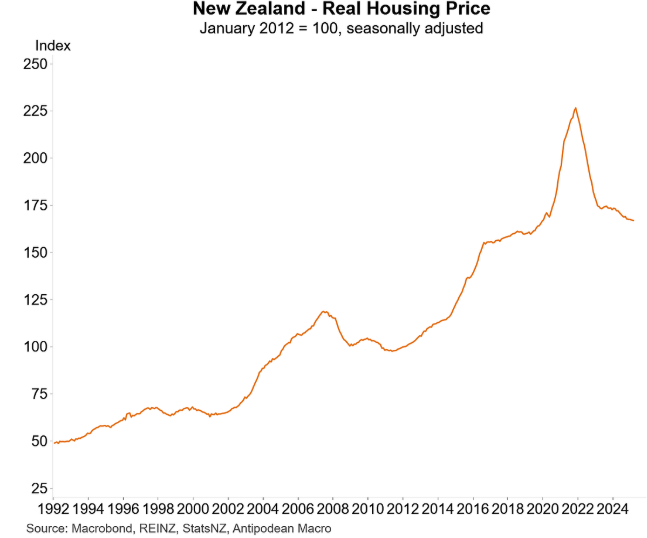

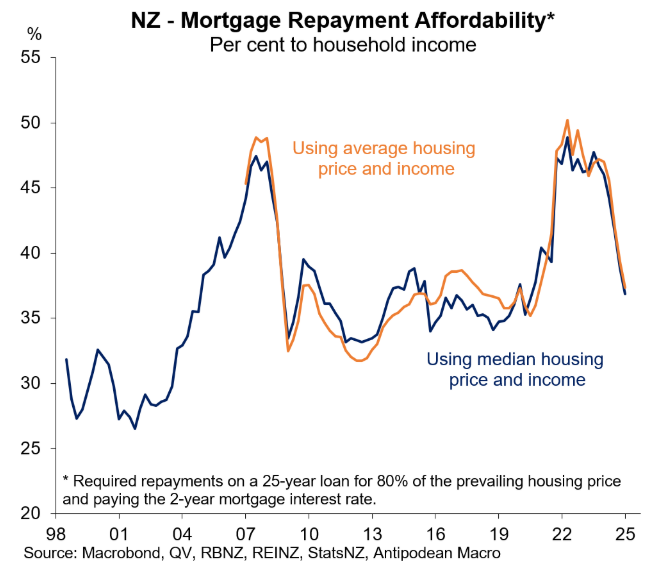

As noted previously, New Zealand’s real inflation-adjusted house price has crashed to levels last seen in late 2019, shortly before the pandemic.

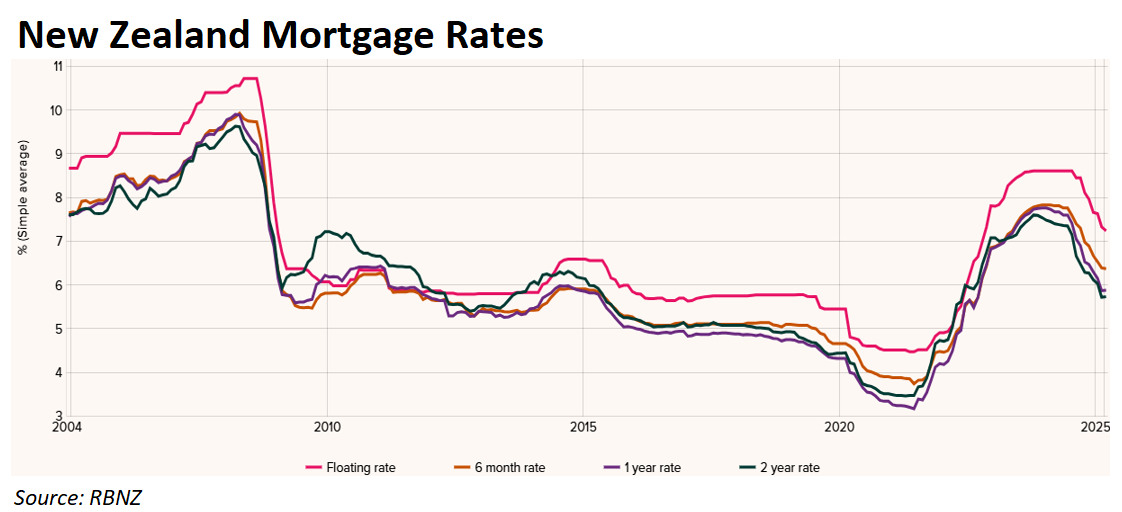

At the same time, the official cash rate in New Zealand has fallen to 3.50%, down from a peak of 5.50%.

Lower home prices and interest rates have combined to significantly improve mortgage affordability across New Zealand.

Mortgage repayments as a percentage of household income have fallen from around 50% to just over 35%.

While New Zealand’s policymakers have taken the sensible approach of allowing house prices to deflate, the Albanese government in Australia is actively working to blow an even larger house price bubble.

Labor has promised to implement a state-sponsored subprime mortgage scheme that will allow all first-time home buyers to purchase a home with only a 5% deposit, with the government (taxpayers) guaranteeing 15% of the borrowers’ loans.

Labor has also directed mortgage lenders to exclude student debt in their mortgage serviceability evaluations.

The inevitable outcome of these policies will be more borrowing, higher household debt, and higher home prices.

If housing affordability is to improve, lower prices are necessary. New Zealand’s politicians understand this concept. Australia’s politicians do not.