Joseph Capurso and Carol Kong at CBA have written an excellent report explaining the economic implications of the US-China trade war de-escalation.

Key Points:

- The 90 day reduction in tariffs on US-China trade confirms ‘peak tariff’ is past.

- We estimate the US effective tariff rate on imports from China is now 41%, down from 155%.

- We estimate the impact on the Chinese economy is small at around +0.3ppt, and only +0.1ppt on the US economy.

- We estimate a negligible impact on the Australian economy because Australia has only a small exposure to the US.

What was agreed?

In a joint statement, the US and Chinese governments agreed to a 90 day pause in the post-Liberation Day (on 2 April) tariff escalation. During the 90 day pause, the US will reduce tariffs on imports from China by a total of 115ppts. The US will retain the 10% baseline tariff, the 20% fentanyl-related tariffs, sectoral tariffs and all tariffs from the first Trump and Biden administrations.

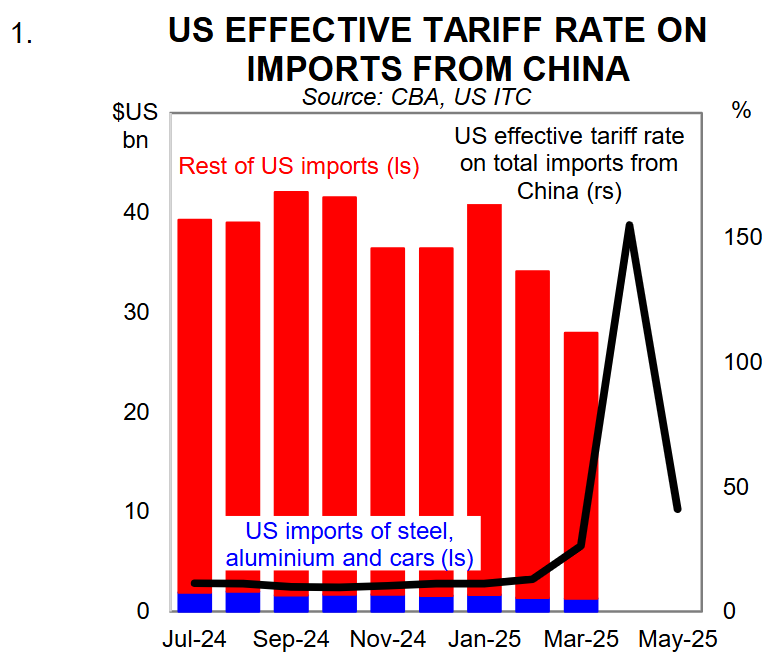

We estimate the US effective tariff rate on imports from China is now 41%, down from 155% (black line in chart 1). The current rate of 41% is materially higher than the 2024 rate of 11%. Imports of steel, aluminium and cars from China still face a 25% tariff. These products comprise a small share of total US imports from China (blue bars in chart 1).

China will also lower its tariffs on imports from the US by 115ppts. The cumulative tariff increases so far in 2025 is 10%, down from 125% previously. In addition, the Chinese government committed to ‘adopt all necessary administrative measures to suspend or remove the non-tariff countermeasures’ taken against the US since Liberation Day. These non-tariff measures include export controls on rare earths, anti-trust and anti-dumping probes.

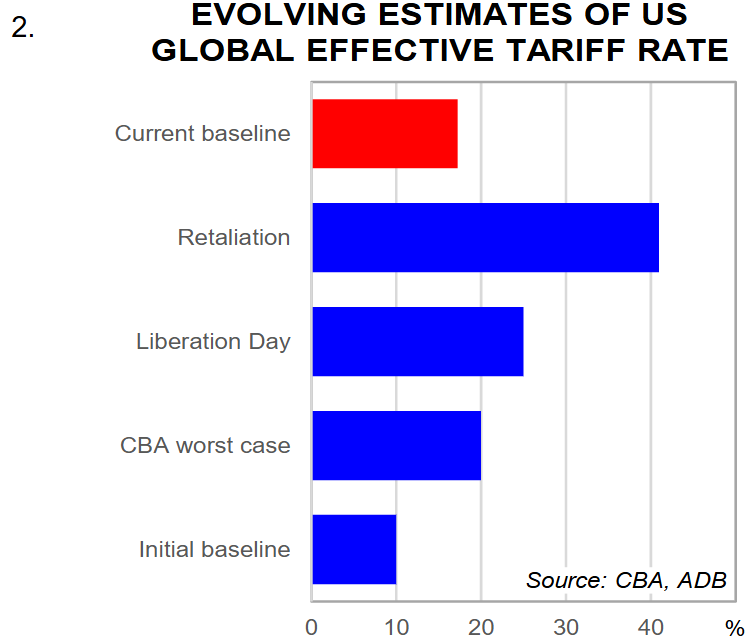

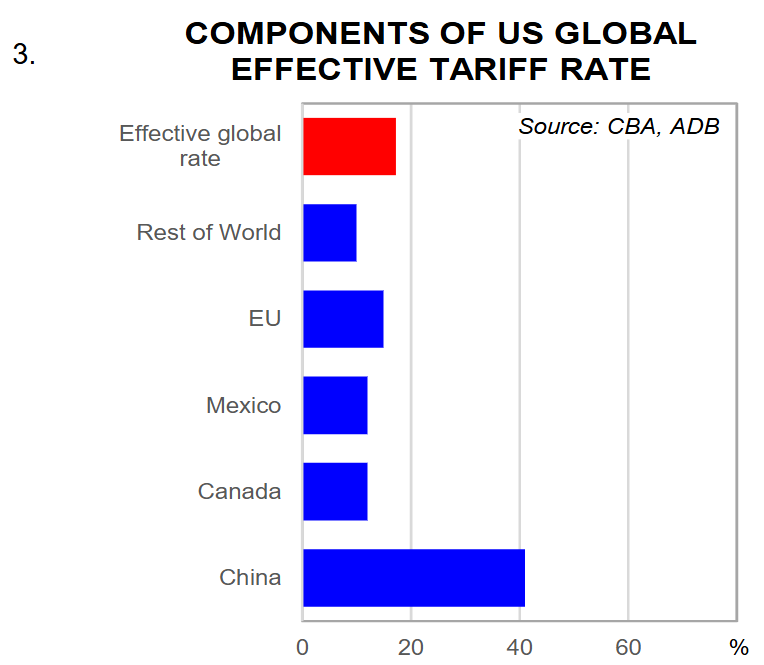

Our estimate of the US global effective tariff rate is now 17% compared to 21% assumed in our recent global economic growth update (charts 2-3).

What will happen over the next 90 days?

The 90 day deal gives the US and Chinese governments time to rethink their positions. Their earlier positions were going to have a material negative impact on their economies.

We consider there is little chance the US and Chinese governments will agree to a comprehensive trade agreement in the next 90 days. The short-lived first trade agreement in President Trump’s first term took around one year to negotiate. At the end of the 90 days, we expect tariffs on imports from China and the US will still be material, probably not much lower than currently. There may be exemptions or lower tariffs for certain products deemed critical. But for non-critical products, we expect material tariffs.

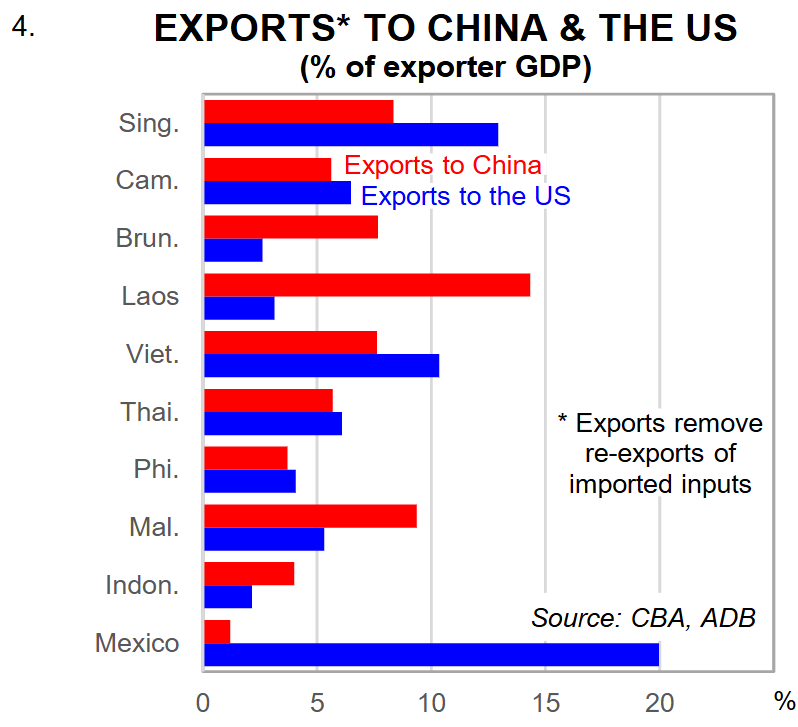

We consider the US government still wants to reduce its trade deficit in goods with China. To do that, the US government will need to convince other governments to reduce the transshipment of Chinese goods through their ports. The US could use the ‘stick’ of high tariffs or the ‘carrot’ of low tariffs. The US has much leverage with Mexico but less with southeast Asia (chart 4).

The long term strategic rivalry between the US and Chinese governments remains. They both want to be the dominant military power in East Asia. They both want to be the leader in a range of high tech industries. And they both want to reduce their dependencies on each other for critical inputs. Future trade between the US and China will be less than in 2024. High tariffs will drive that reduction in dependency.

Implications for economies

The temporary deal reduces some of the downside risks to the US and Chinese economies. But the deal will still inject a stagflationary impulse into the US and Chinese economies.

We have updated our model estimates of the impact of US tariffs on imports from China. The reduction in tariffs—if extended for one year—will add back around 0.3ppt to Chinese economic growth (chart 5). But we are not changing our forecast for Chinese economic growth in 2025 of 4.6% for two reasons. First, the agreement is for only 90 days rather than one year. It is uncertain what the tariff regime will be after the deal expires. Second, we consider the lower economic costs simply mean the Chinese government will not have to provide as much support to the economy as it would have.

China is an important source of imports for the US. Lower tariffs on imports from China will boost profit margins of US importers and purchasing power of US consumers. We estimate the impact of yesterday’s deal is around 0.1ppt (chart 5). Given the uncertainties of the economic outlook, including US monetary and budget policy, we retain our forecast for US economic growth in 2025 of 1.1%.

We estimate the direct and indirect impact on Australia from the US-China agreement is minimal (chart 5).