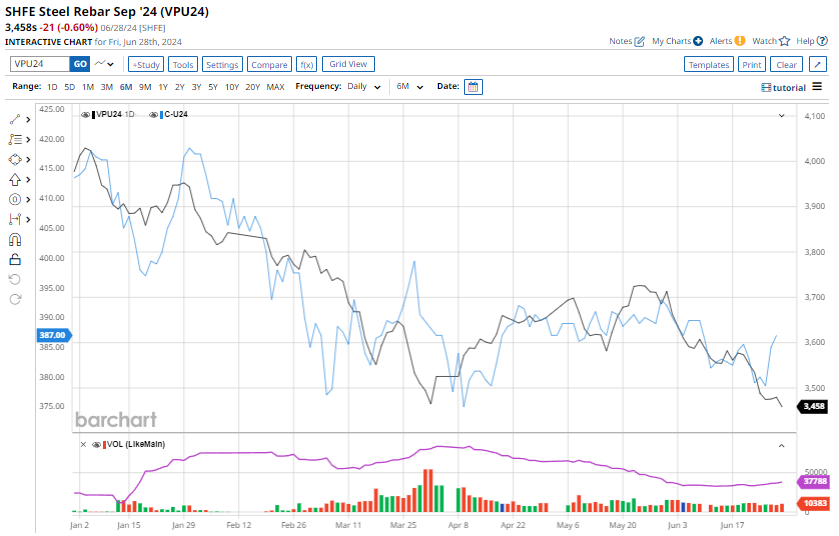

Shanghai rebar continues to fall. Global scrap has momentarily decouled:

SGX iron ore futures have bounced rather unconvincingly:

Same at Dalian:

And coking coal:

Needles to day, steel mill profits are sinking even further.

Data is mixed:

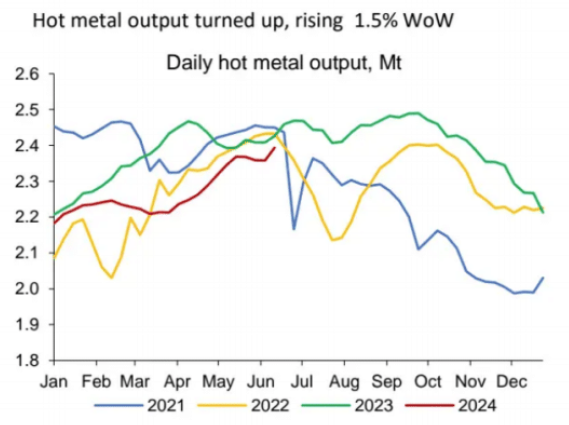

Average daily hot metal output among steelmakers surveyed hovered at a relatively high level of around 2.39 million tons as of June 27, despite a weekly fall of 0.2%, data from consultancy Mysteel showed.

But persistently high portside inventories, which climbed by 0.3% to 149.26 million tons, capped upside room.

There is a clear surplus of iron ore with hot metal output decent but port inventories still rising.

Hot metal output typically falls from here:

Given weakening Chinese chousing completions, the base case is for it to slide though H2.

Which will leave excess iron ore exposed to price falls heading into the end of Q3.

Q4 and Q1 typically rebound but H1 2025 brings more falling Chinese completions and H2 brings the Simandou Pilbara killer!