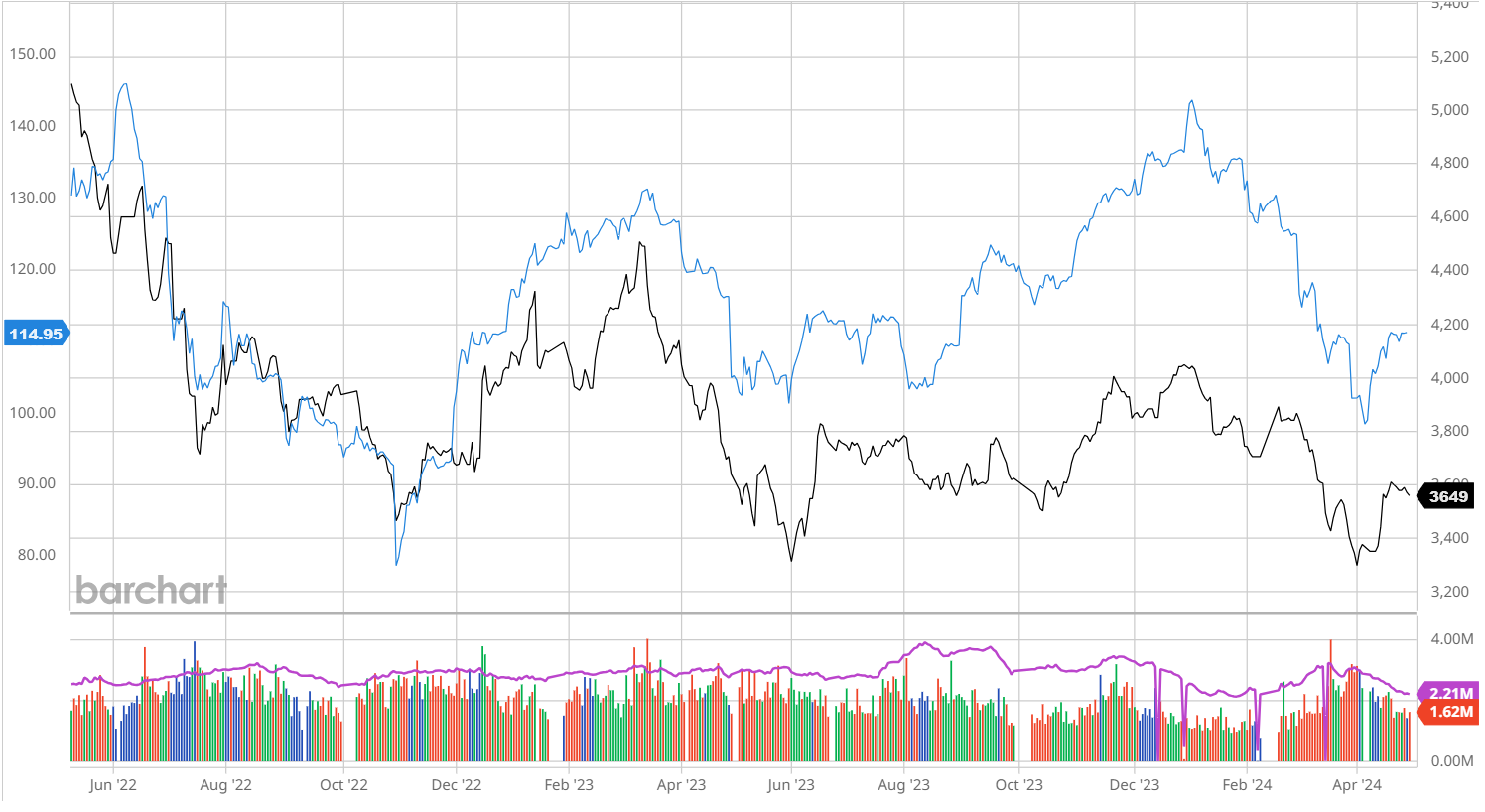

The FE complex rebound has stalled:

The signals out of China are mixed at best:

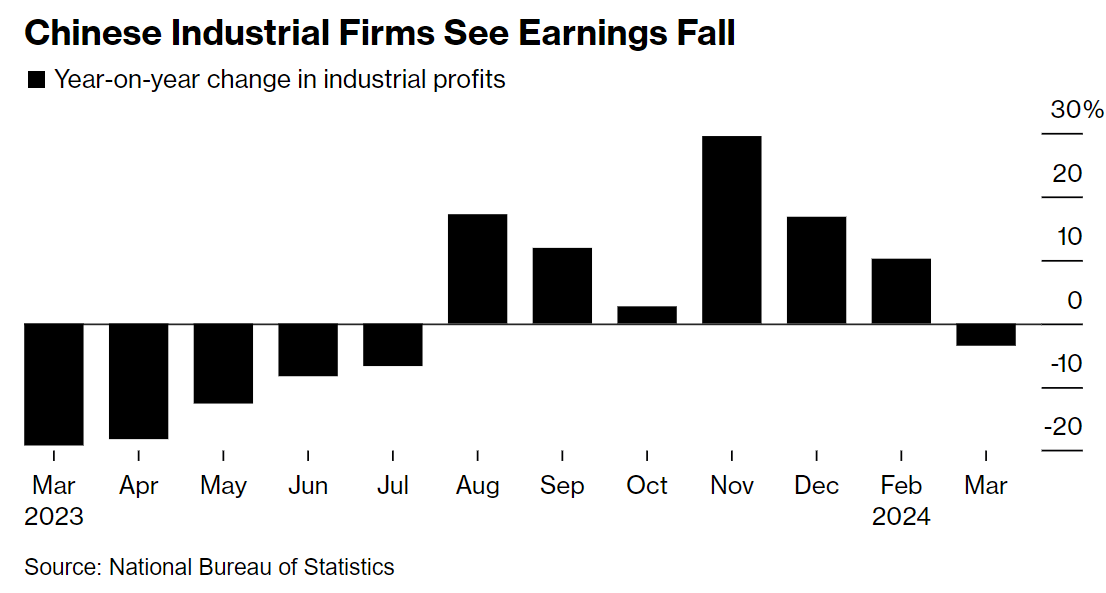

China’s industrial companies’ profits fell in March as exports flagged and deflationary pressures persisted, suggesting the economy’s stronger-than-expected growth early this year might be tough to maintain.

Industrial profits at large-scale Chinese companies declined 3.5% from a year earlier in March, according to data published by the National Bureau of Statistics on Saturday. For the first three months of the year, profits rose 4.3% to 1.51 trillion yuan ($208 billion), slowing from a post-Covid rebound.

Industrial profits derive from nominal growth, so this tells us that the deflationary environment in China is intensifying, which makes it easier to meet GDP targets but harder to lift living standards as debt burdens grow not shrink.

Is there an imminent answer? Goldman:

Macro trip takeaways: We hosted a China macro trip in Beijing on April 23 and the tone was in general downbeat.

Although the Q1 real GDP growth was stronger than expected, speakers questioned the reliability and sustainability of the print.

On property, speakers believe policy designs of current easing measures have flaws and risks are rising for falling property prices to spill into the financial system.

On deflation and overcapacity, speakers do not see any signs that the government changes its focus from stimulating goods and production to stimulating services and demand.

Although Q2 real GDP growth is likely above 5% yoy due to last year’s low base, speakers are cautious on the medium term outlook, especially when measured in nominal terms.

More tools and more complexity in China’s monetary policy: Both the Ministry of Finance and the PBOC suggested last week that the central bank should increase trading of central government bonds (CGB) to enhance monetary and fiscal policy coordination.

In our view, PBOC regular purchases and sales of CGB is a new tool for the central bank to manage liquidity and control the yield curve.

At present, we expect one RRR cut in Q2, one 10bp policy rate cut in Q3, and another RRR cut in Q4.

But the probability of RRR cuts will decline if the PBOC releases liquidity via large CGB purchases, and the probability of a policy rate cut will diminish if the USD strengthens further.

April Politburo meeting and PMIs to watch: TheApril Politburo meeting, which focuses on economic affairs, is expected to be held in the next day or two.

Policymakers should be content with the 5.3% yoy real GDP growth in Q1 (given the “around 5%” growth target this year) and are in no hurry to introduce additional easing measures.

We expect policy tone to be neutral and the focus to be on implementing existing easing measures instead of making new ones.

For April PMIs, residual seasonality points to a notable decline: we expect the official NBS manufacturing PMI to drop from 50.8 in March to 50.1 in April.

There is nothing much here to keep steel and iron ore prices high. But then, there is always India, says HSBC:

“We expect steel demand growth to be muted in the next five years, growing at about 2% as mainland China cuts back,” Lau said. “However, we see India stepping up and recording the world’s fastest steel consumption growth rate.”

“We don’t expect a meaningful increase in iron ore output by major producers,” Lau said. At the same time, “we expect iron ore demand to remain robust, reflecting our global-steel output estimates,” he said.

I expect Chinese steel output to fall about 3% per annum for the next ten years, or about 30mt per annum.

India can reduce this through its aggressive capacity expansion, but to do so, it will have to contend with China’s Himalayan-sized overcapacity, which dumps more steel everywhere every year. India is already importing around 9mt, with China as the largest contributor.

Can anybody seriously contend that a massive steel production overcapacity war between China and India will do anything other than crater global steel prices?

On top of that, India has better-quality iron ore reserves than China and excellent potential to expand them further.

India only imported 5mt of iron ore in the last year while exporting roughly 40mt.

As for the majors, 40-50mt of new ore are coming this year (Onslow, Iron Bridge, Vale) and every year until 2030 (Simandou and Vale).

I have not seen the full HSBC report, so I can’t comment with complete authority, but the quotes are categorically wrong.