Let’s start with the cause:

One of China’s biggest property firms delayed its earnings report while another posted a record profit decline as the nation’s real estate crisis shows no signs of easing.

Country Garden Holdings Co., once the nation’s top residential builder by sales, made a surprise announcement late Thursday that it will miss a deadline for reporting annual results, saying it needs more information. China Vanke Co., at one time the largest listed developer, said net profit tumbled 46% last year, the biggest drop since its 1991 listing.

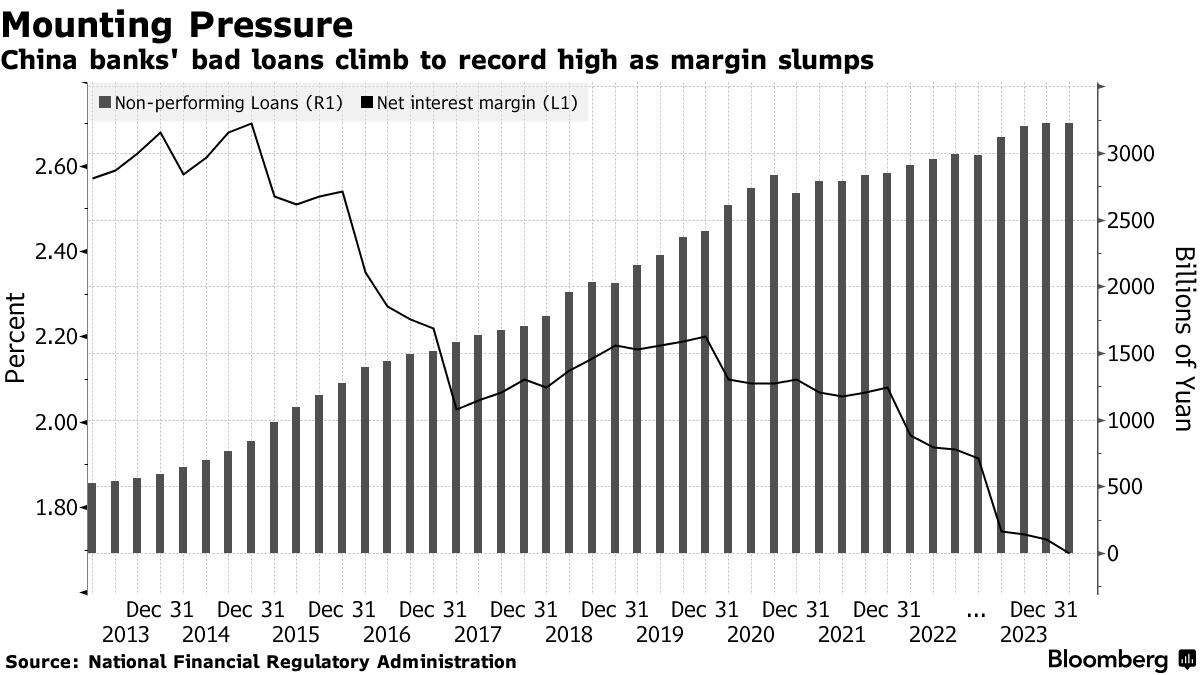

The dire statements, along with a jump in bad loans at some banks, underscore how a weak economy and sluggish consumer confidence continue to weigh on home sales in the world’s second-biggest economy. Annual price declines deepened in February for both new and used homes, highlighting the challenge for authorities as they try to salvage the beleaguered market.

…Fitch Ratings on Thursday cut forecasts for the housing market, now expecting a 5%-10% fall in new home sales this year amid weaker home-buying demand. The ratings firm previously estimated a 0%-5% decline.

The Fitch numbers are stupid.

Sales are down by half across Q1. Vanke very likely financially engineered its profit. All China’s megabuilders are like Evergrande now as the banking system follows credit markets into tightening debt covenants despite so-called “white lists” and other yawnulus from Beijing.

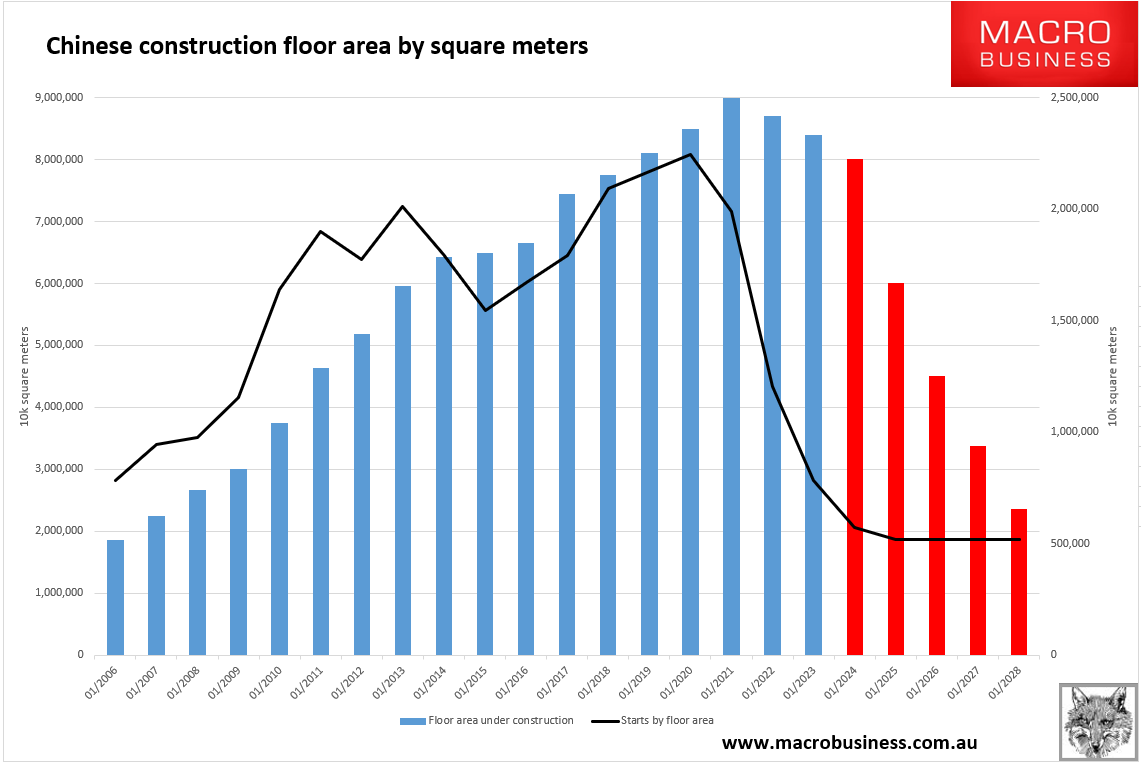

The drawdown in construction and sales has barely started versus starts:

There is a backlog of completions to get done, so activity won’t entirely disappear. But so what?

Any way you slice it, construction steel demand in China is going over the edge of the steepest and deepest cliff in the galaxy.

It doesn’t matter what number we put on it. Demand for rebar, wire rod, and other construction steel could drop -50 %, -60% or -70%. It doesn’t matter. Dead is dead.

Which brings us to the fun part.

Dalian iron ore futures have broken new lows:

Along with coking coal:

The scuttlebutt from MySteel is pretty bad:

The blast furnace (BF) capacity utilization rate among the 247 Chinese steel producers under Mysteel’s regular tracking stood largely stable on week at 82.76% during March 22-28, though it dipped 0.03 percentage point from the previous week.

During the same period, the daily hot metal output among these sampled steelmakers was also generally unchanged at 2.21 million tonnes/day, down by a tiny 800 t/d on week, while their average operational rate lost 0.3 percentage point on week to reach 76.6%, the survey showed.

The mild decline in production was mainly due to routine maintenance among the sampled steelmakers, Mysteel Global noted.

As such, the mills’ demand for steelmaking raw materials slightly waned, with the daily consumption of imported iron ore among the same 247 mills under Mysteel’s tracking averaging 2.7 million t/d over March 22-28, dipping 3,100 t/d on week.

As of March 28, the total inventories of imported iron ore held by these sampled steelmakers dropped 2.5 million tonnes on week to reach 91.5 million tonnes, the survey showed. This would be sufficient to last them for 33.9 days at their present use rate, shorter by 1 day from the prior period, as Mysteel assessed.

The marked retreat in steel consumption among end-users made domestic steelmakers more cautious about ramping up production, and they tended to keep their feed stocks at a low level to avoid financial risks, market sources observed.

Port inventories of iron ore are bulging at 144mt, and the steel inventory has barely budged from 20mt.

These weak numbers are in the middle of peak season for steel demand and iron ore supply disruptions.

To describe this situation as weak doesn’t quite say it. Price discovery is screaming that every facet of the Chinese FE complex is already in surplus, and it is getting worse each day.

CISA can see it happening and is running around like a headless chook:

It is unlikely to succeed. The Chinese steel production sector is too fragmented. If it does, steel prices might stabilise while iron ore and coking coal fall through the floor.

However, a more likely outcome is a repeat of 2015, when excess Chinese steel production washed up at giveaway prices on every unprotected beach worldwide.

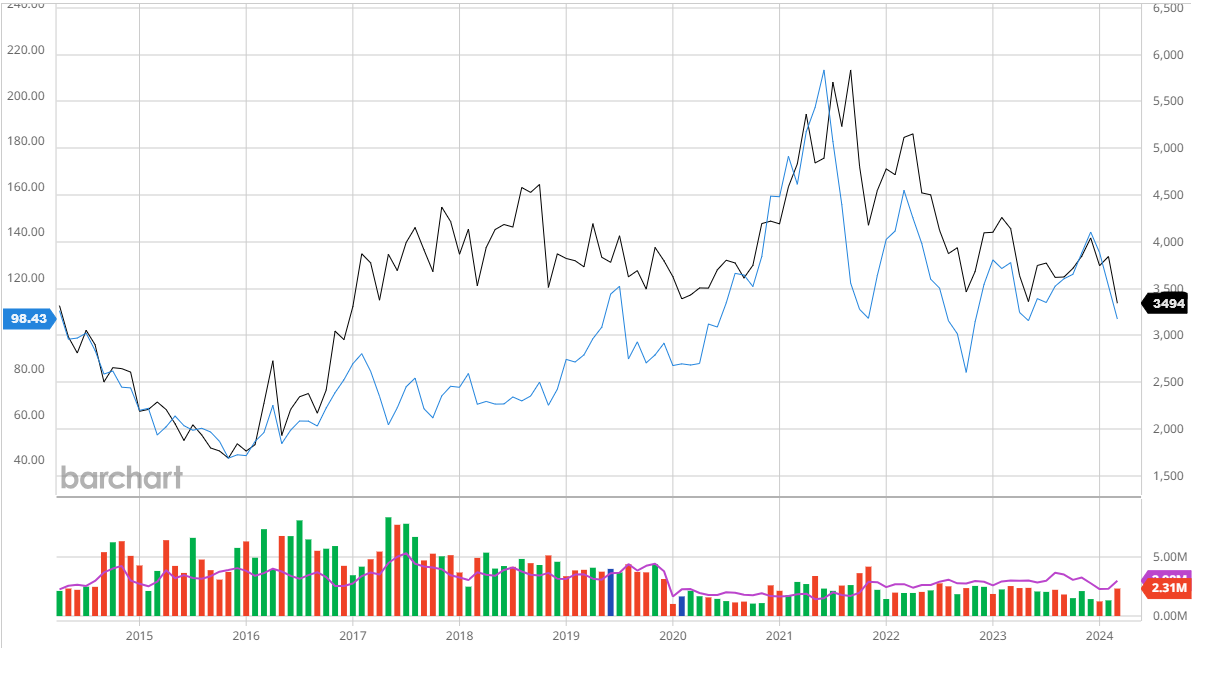

But that still won’t help iron ore coking coal. They will follow the cheap steel prices lower. Here is the long-term chart of SGX futures versus rebar futures:

In 2015, we conducted a practice run of today’s market dynamics. Rebar fell below 2000CNY, and iron ore hit $37.

Two factors triggered the recovery:

- A Chinese QE program for ghost city property construction was so out of control that it blew the roof off the world’s largest asset class and ponzi scheme for five years.

- And, a gigantic mining accident in Brazil curtailed ion roe supply for years.

Today, we face the reverse conditions. The Chinese property build-out is over as demographics turn sharply lower, and the ghost cities idle.

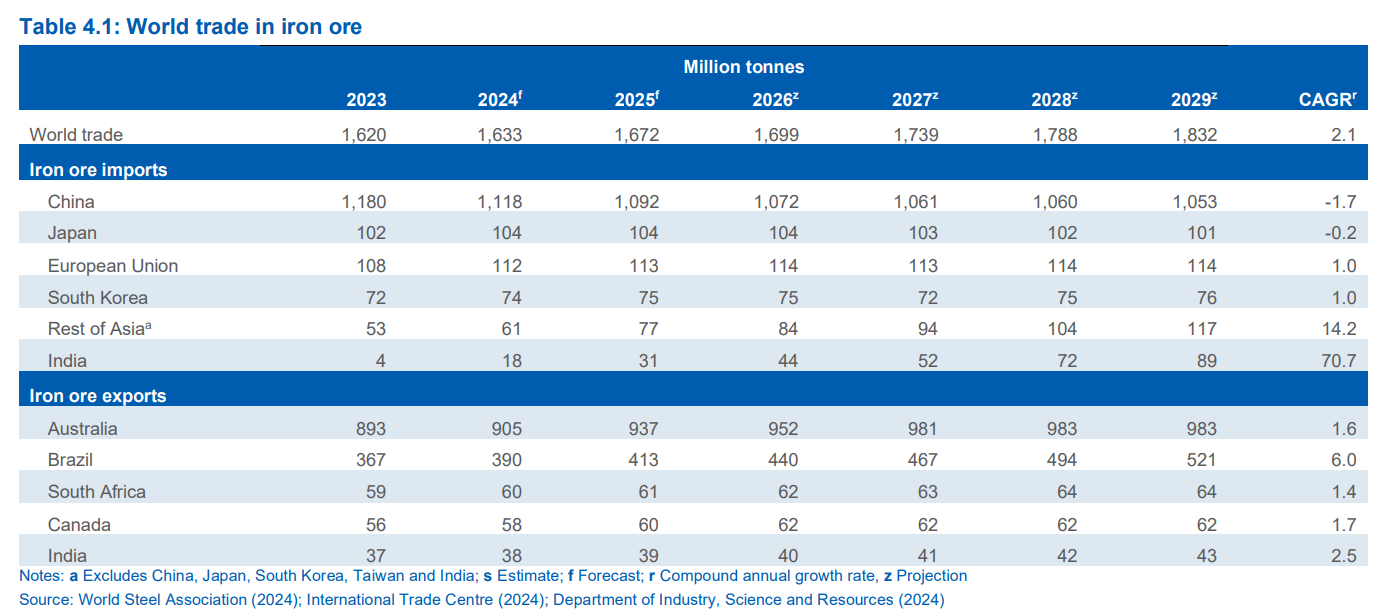

What is coming instead is more iron ore and met coal. From the Office of the Chief Economist:

The Office appears to be so horrified by the 260mt of iron ore expansion over the next five years that it didn’t even include Simandou, which adds another 60-100mt.

The table suggests that the iron ore surplus will be absorbed by a bit of demand expansion in India and the gentle subsiding of Chinese construction.

This is nonsense.

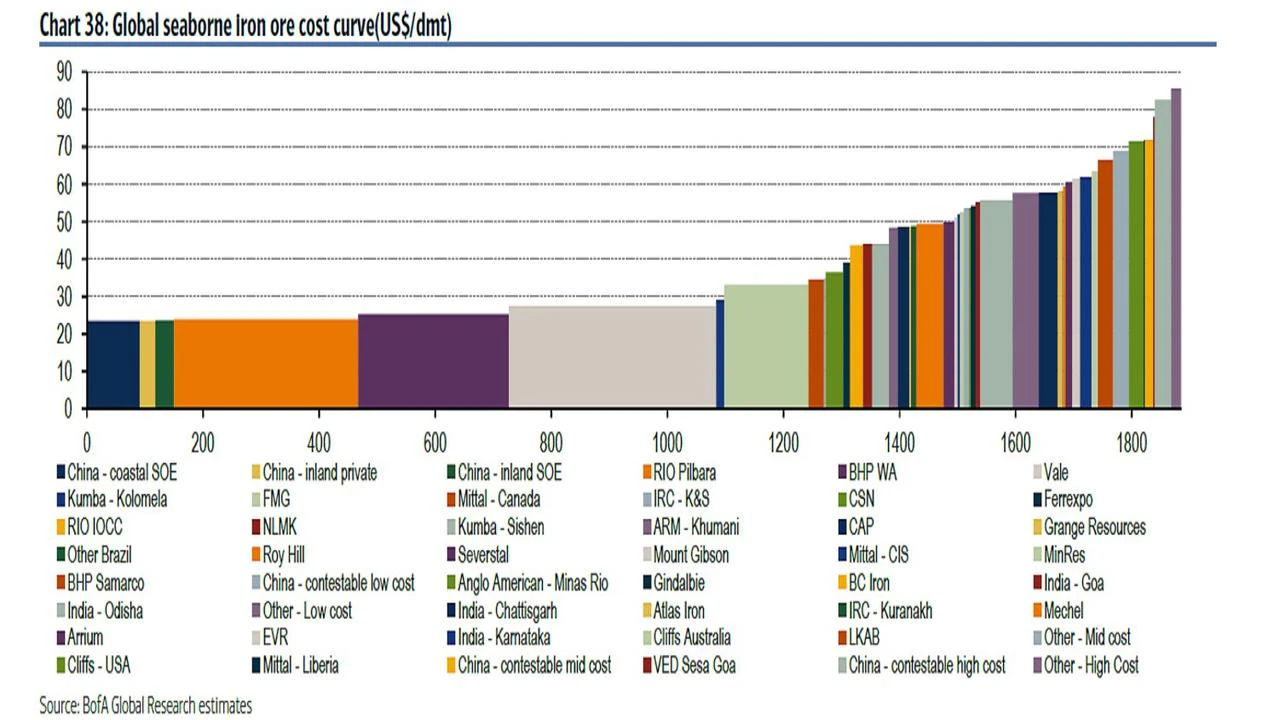

Instead, we are at the threshold of the most epic iron ore shock and consolidation the world has ever seen. At the end of it, iron ore will be $20 per tonne, and the only producers left will be those scratching out a living eating dirt in the most inhospitable climes on Earth.

Every miner above $50 per tonne on the cost curve is already the living dead:

But don’t forget, as the shakeout begins in earnest, royalties, taxes, labour costs and every other input you can think of will be cut, sliced, rationalised and shed. The entire cost curve will shrink yearly as the dying miners gasp for one last breath.

See nickel right now. So, I am very likely being optimistic.

For twenty years, demand for iron ore and coking coal has risen relentlessly, supporting all manner of Australian stupidity.

Now, it is going to reverse, and the stupidity will explode.