The AFR’s Jonathan Kearns argues that Australia’s interest rates are not as restrictive as those of other nations and are not high enough to tame inflation.

Accordingly, Australia is unlikely to experience the ” immaculate disinflation” that will be experienced elsewhere and will have to keep rates higher for longer.

“The basic metric for monetary policy’s stance is the central bank rate less the inflation rate”, Kearns writes in The AFR.

“This comparison highlights that monetary policy in Australia is less restrictive than in most other advanced economies, in absolute terms and relative to the historical average and range”.

“A less restrictive policy stance in Australia is not justified by economic conditions”.

“Australia does not rank well in terms of how far inflation is above target and the tightness of the labour market. The US, euro area and Canada have all tightened much more given their macroeconomic conditions and so have better prospects of containing inflation”.

“There are many different paths that inflation can take in returning to target and maybe we are witnessing an immaculate disinflation”, Kearns says.

“But given the evidence that the cash rate has not been high enough, there is an increased risk that inflation will be persistent and so it will take longer before the RBA can cut the cash rate”.

Kearns arguments don’t make sense.

First, inflation in Australia is falling at a similar rate to elsewhere.

Second, the notion that Australia’s monetary policy is less restrictive is asinine.

Australians carry some of the largest debt loads in the world. We also have a much higher share of variable rate mortgages than most other nations.

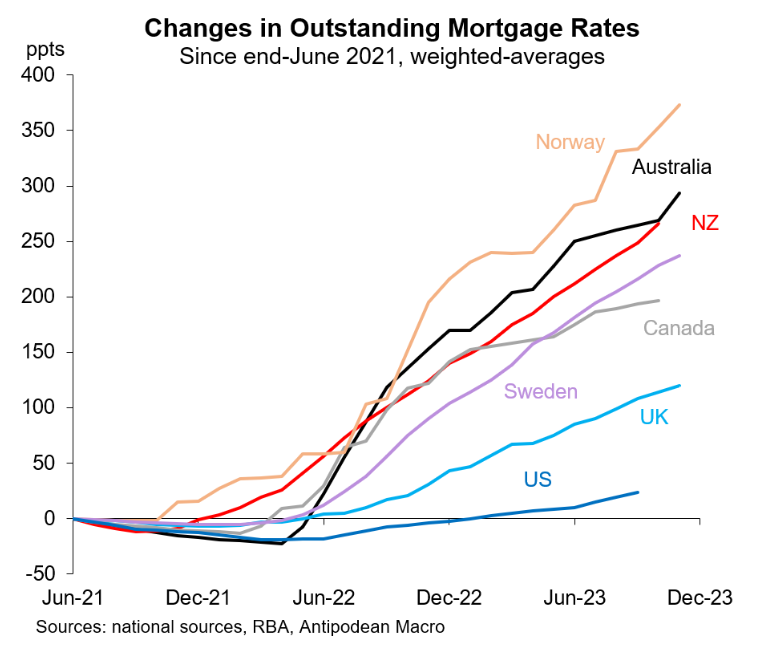

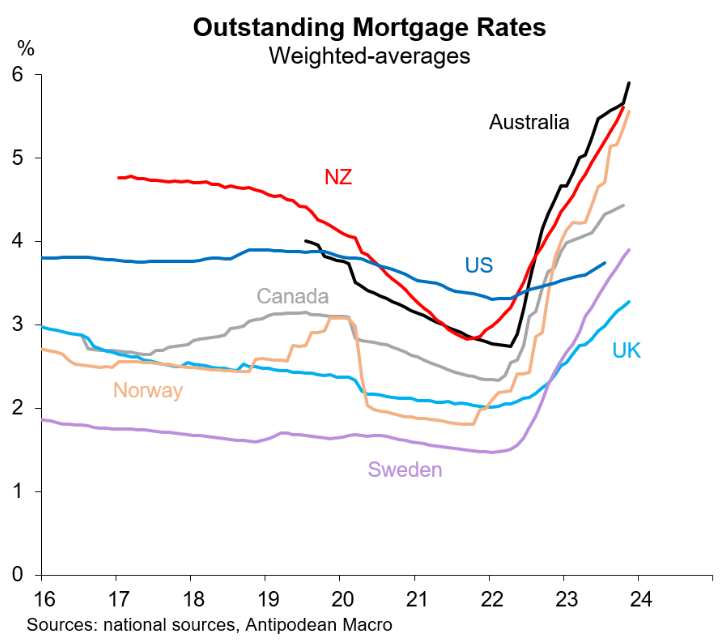

So, although the Reserve Bank of Australia (RBA) has not lifted the official cash rate (OCR) as aggressively as some other nations, the average interest rate paid in Australia is much higher:

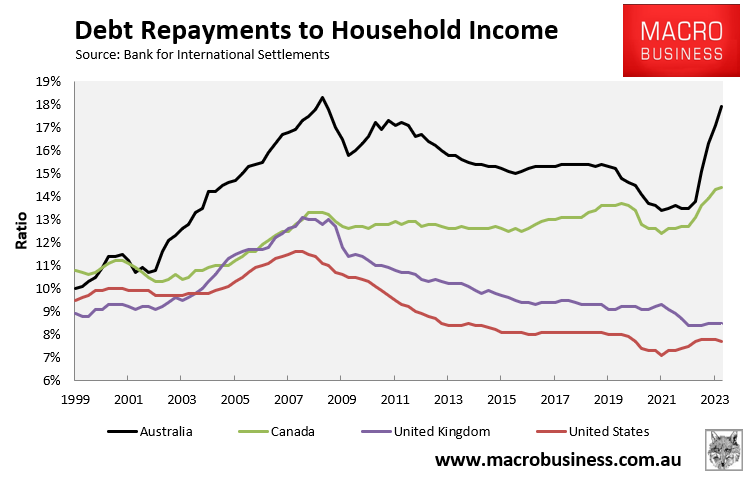

Separate data from the Bank for International Settlements (BIS) shows that the aggregate share of household income going to debt repayments (i.e. both principal and interest) has risen especially quickly in Australia:

Again, the predominance of variable-rate mortgages has resulted in Australia’s OCR being passed on to mortgage holders more swiftly than elsewhere.

These above charts also explain why the RBA doesn’t need to lift interest rates as high to reduce demand and inflation.

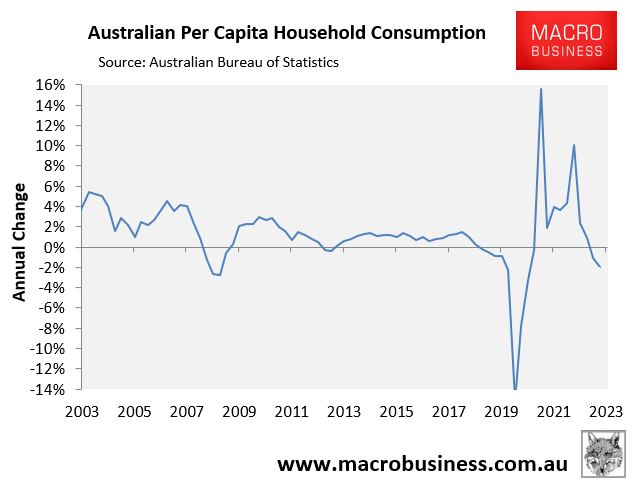

Australian households have already being hit hard. This is evidenced by the BIS chart above, as well as the national accounts data showing falling household consumption.

Ignore pundits like The AFR’s Jonathan Kearns. Watch the economy instead, which is weakening fast.

The RBA will very likely cut rates in the second half of the year.