Back from holiday and the much anticipated new boom in steel output is caput:

The benchmark March iron ore SZZFH4 on the Singapore Exchange slid 2.91% to $127.45 a ton, as of 0706 GMT, in part due to fading bets of early U.S. rate cuts amid stronger-than-expected U.S. producer prices in January.

The weakness in the Singapore benchmark came after it had climbed by over 3% over the holiday break when Chinese bourses were closed.

“Such a steep price fall is out of my expectation as we thought prices would consolidate today; the sharp drops in the coal market might have given a blow to market confidence, dragging down ore prices as well,” said Cheng Peng at Sinosteel Futures.

Iron ore inventory at major Chinese ports surveyed rose 4% during the holiday break to 136.76 million tons as of Feb. 18, while profitability among mills surveyed slid to 25.54%, the lowest since mid-November, data from consultancy Mysteel showed.

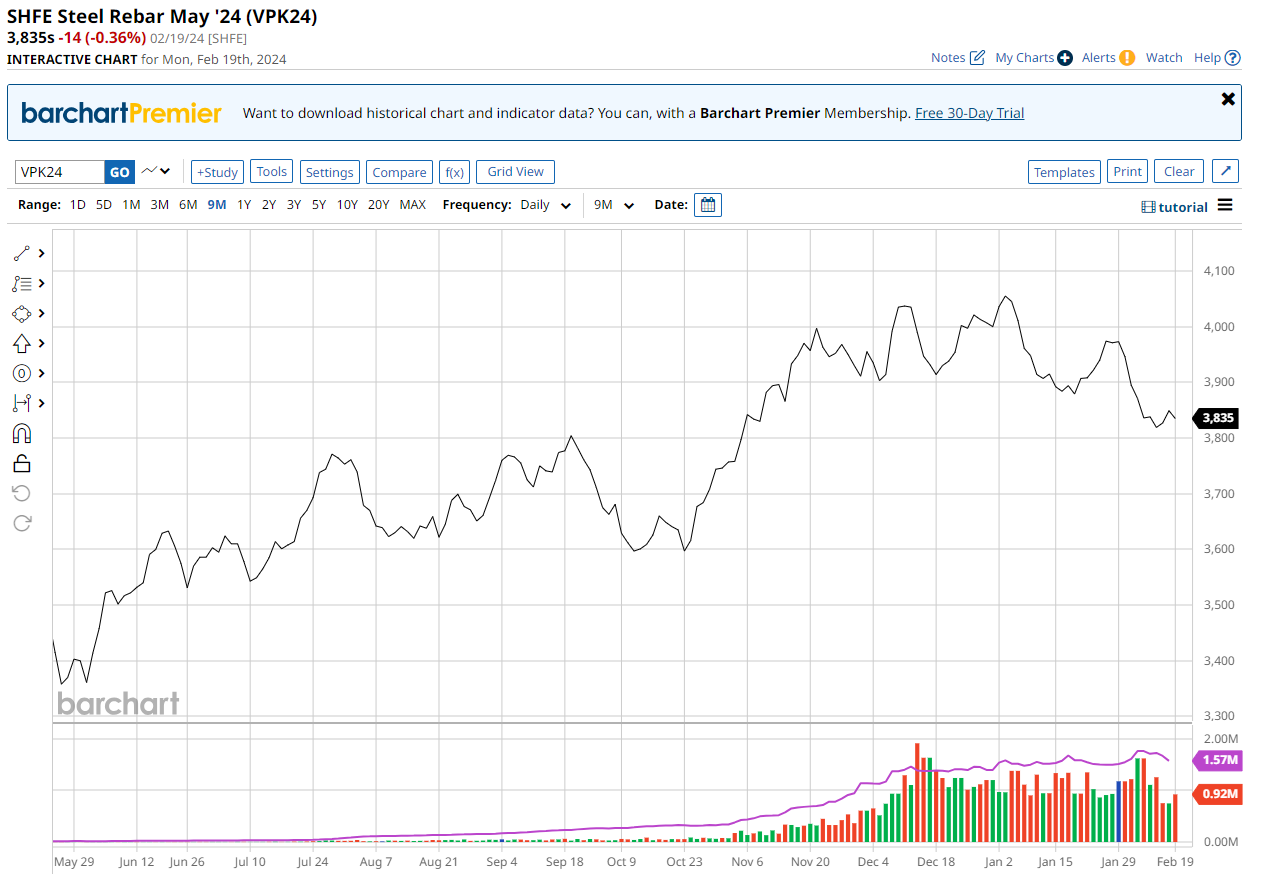

Rebar futures were soft:

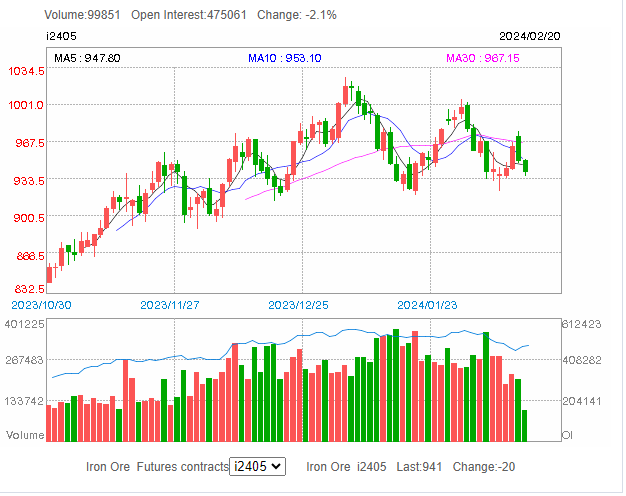

Likewise fell out of bed for both iron ore and coking coal:

Weak demand, steel ruined margins and rising inventories of inputs. Yuck!

It’s probably still too early to expect a significant price drop, but when seasonal tailwinds turn headwinds in Q2, such a mix will be toxic.