Last year, China increased steel output via expanding exports, infrastructure, and public support for housing completions.

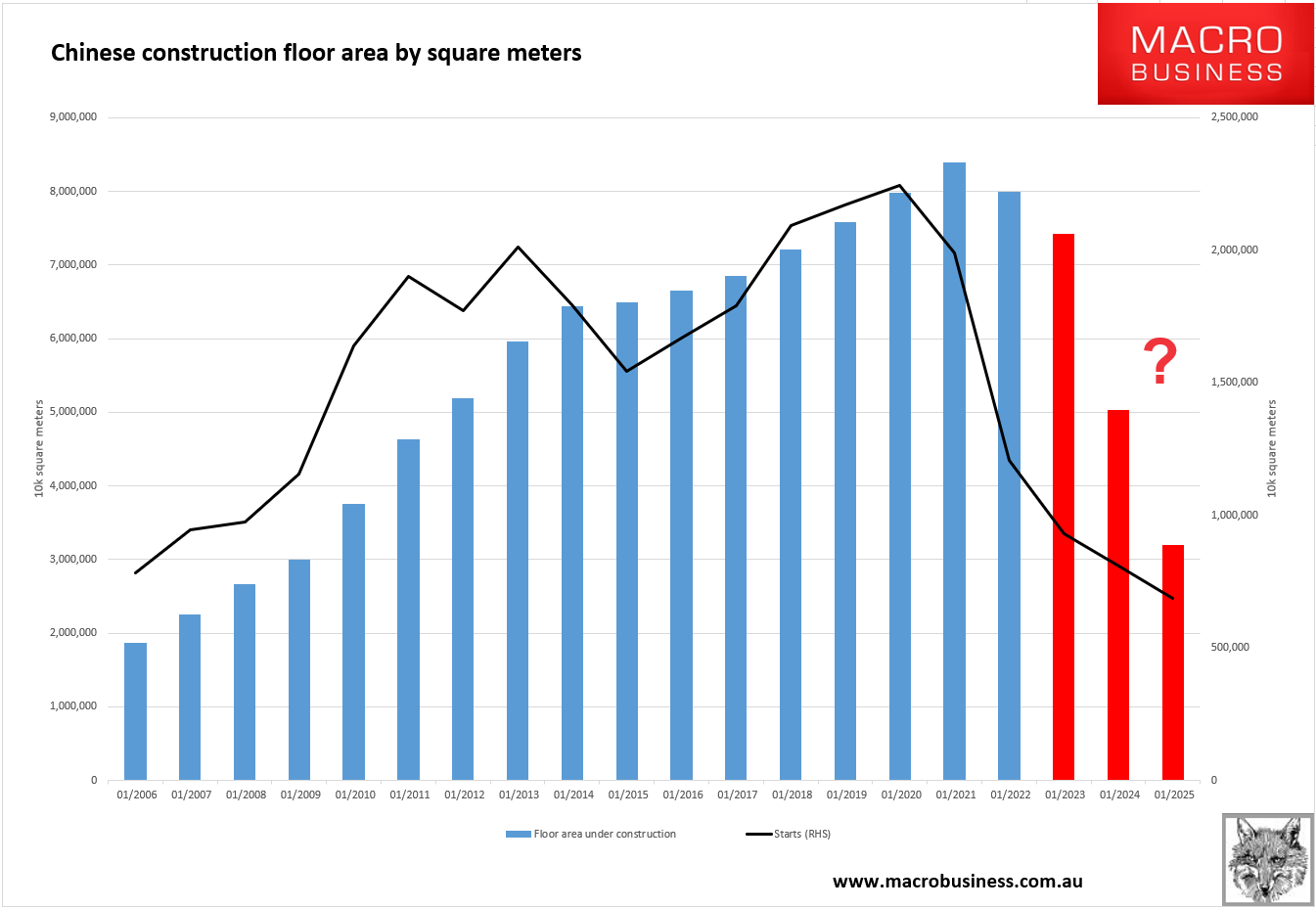

To do so again will be difficult. Floor space under construction must track cratered starts lower at some point:

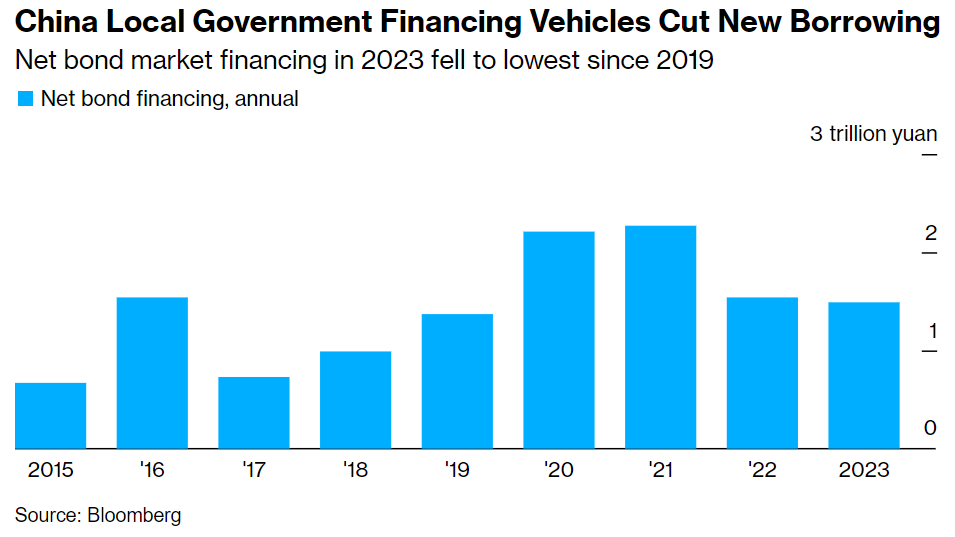

Local government deleveraging and exhausted projects will inhibit infrastructure. The federal budget can step in, but growth will be tough:

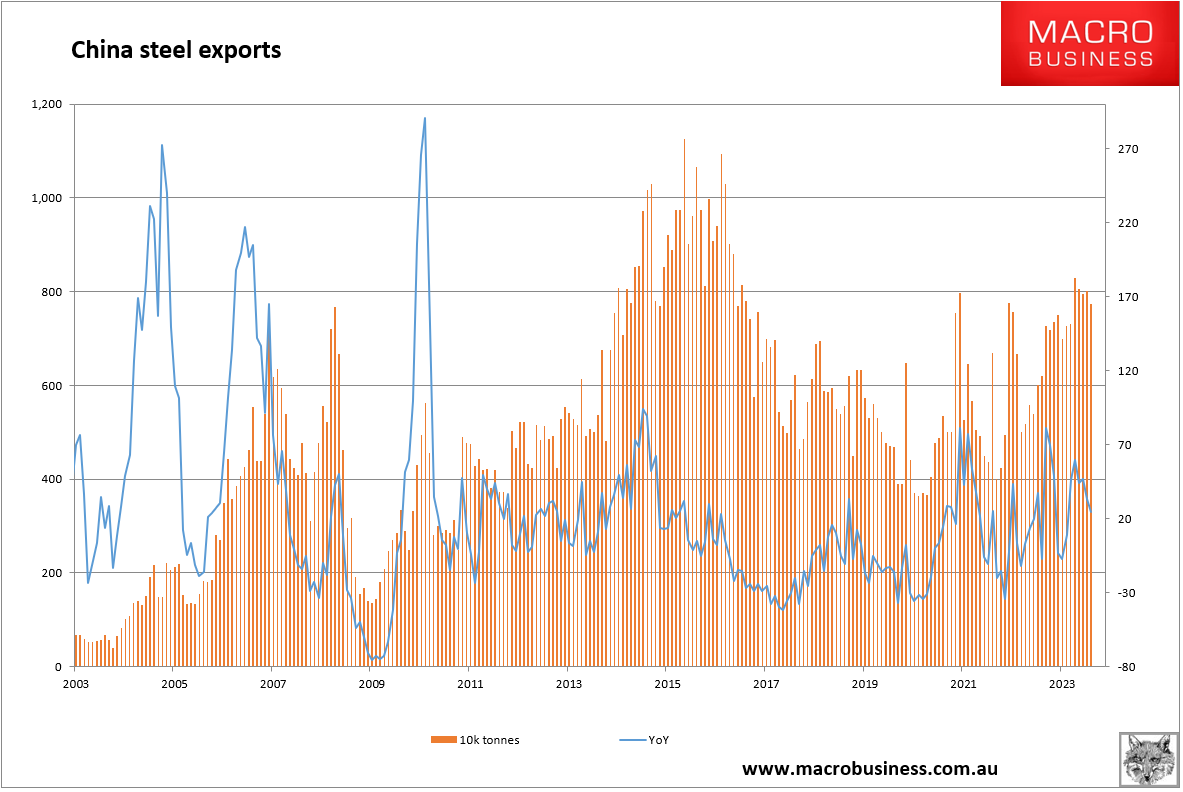

Rising steel exports were a story of substituting for falling Ukrainian exports. For more growth this year, steel will need to take market share via lower prices:

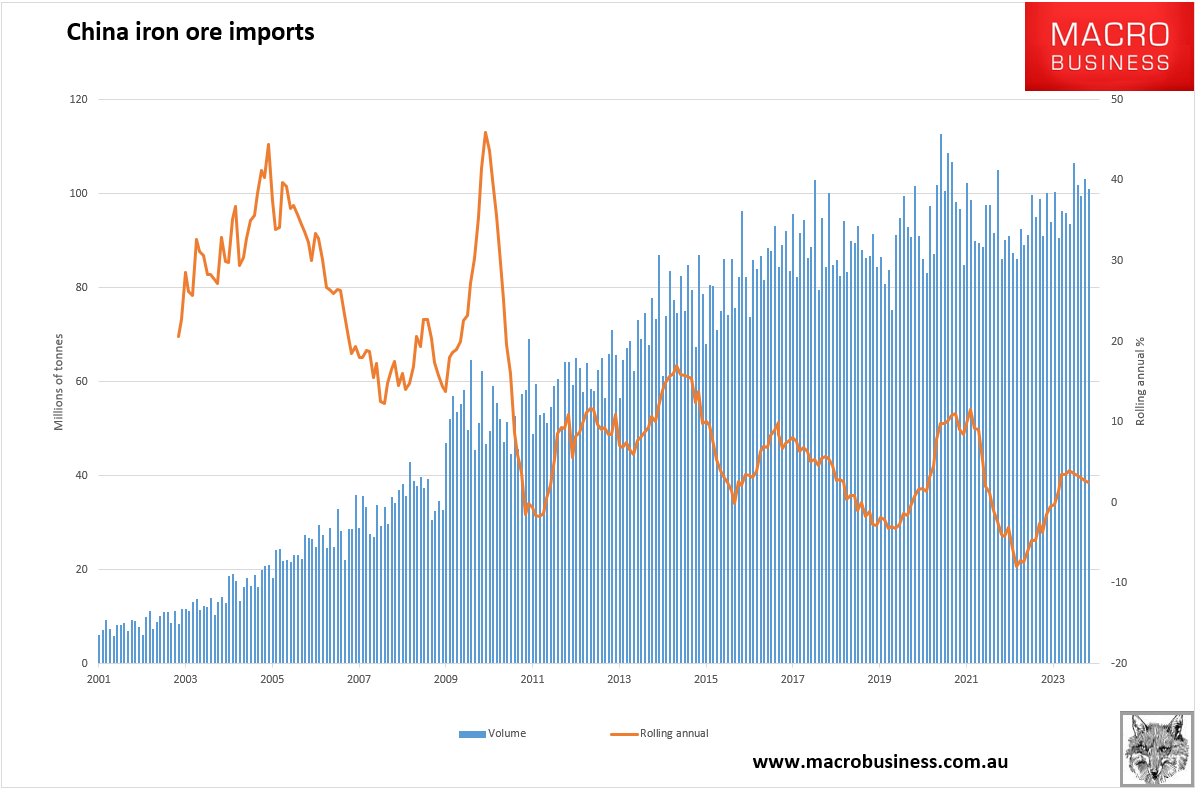

Iron ore imports finished the year at 100.9mt for a record year:

However, this was largely a story of declining steel recycling output, which fell from 217mt in 2020 to 144mt in 2023. That’s 100mt of iron ore equivalent.

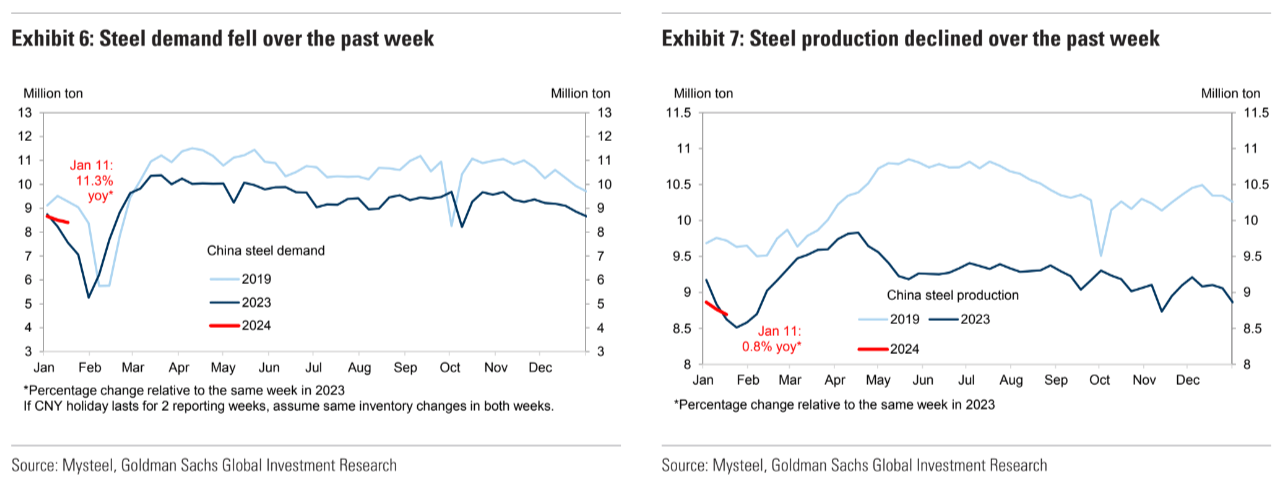

MySteel indexes don’t look too bad to start the year, but it’s too early to judge and notoriously distorted before CNY:

The base case is that Chinese steel output shrinks materially in 2024, and some steel recycling returns as power markets normalise with coal costs.

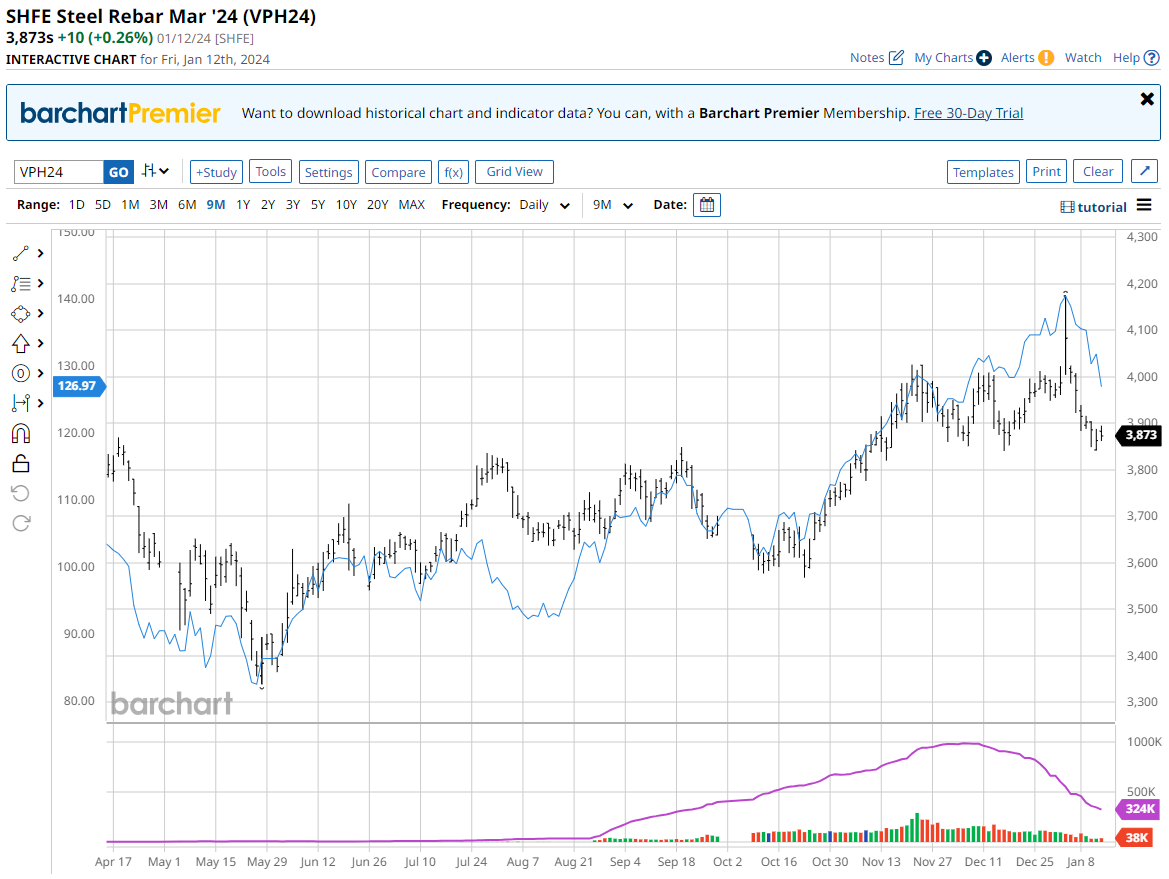

Iron ore was clubbed 4% Friday but rebar stabilised:

I expect both to trend lower around the usual seasonal patterns as the year progresses.