SMM kicks us off.

According to the import ore profit table of SMM, the import ore loss is showing an intensifying trend. From a fundamental perspective, the blast furnace operating rate for this period (1.4-1.10) decreased by 0.59% to 88.11% on a month-on-month basis. The daily average iron production of 190 sample steel mills was 2.1247 million tons, a decrease of 0.7 million tons compared to the previous period and nearly 80,000 tons year-on-year. Iron production has been hovering at the bottom, and combined with the recent slow stock replenishment of steel mills before the holiday, the market sentiment is relatively pessimistic. Short-term or weak oscillation is expected to continue, and it is expected that the import ore profit will continue to weaken in the short term.

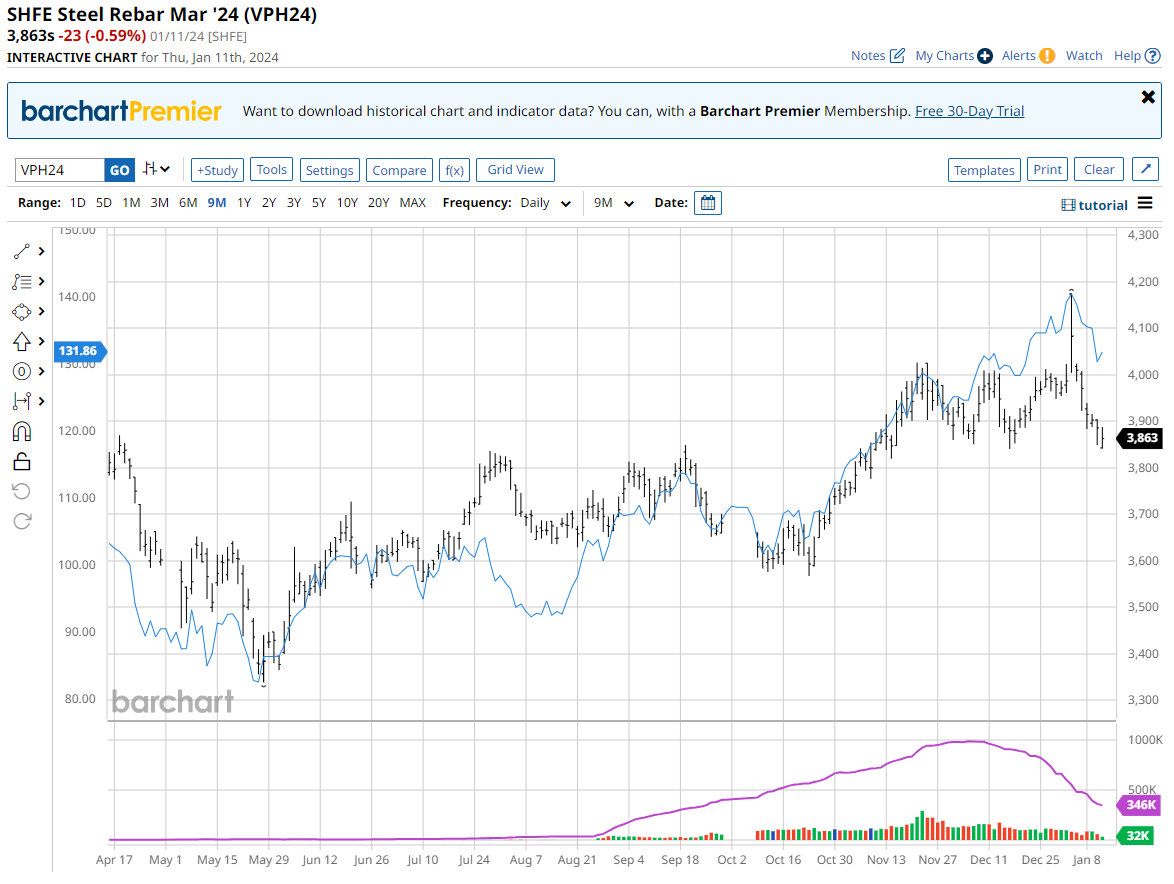

It is quite bearish that output is down so far yet rebar prices keep falling anyway:

It does make one wonder if we are not in the midst of another demand shock as the Chinese property crash has its way.

MySteel is likewise bearish.

Meanwhile, an extra 15 million tonnes of domestic iron ore will be mined this year, which will also contribute to China’s total iron ore supply. Within the additional domestic total, some 6 million tonnes will reflect the slow but gradual resumption of production at many miners in North China’s Hebei after they had suspended operations following a mining accident in September 2022, the report notes. The other 9 million tonnes of the on-year increment will be output from newly-commissioned domestic iron ore mines.

On the other hand, iron ore demand from Chinese steelmakers will weaken this year, with domestic production of hot metal seen declining by 8 million tonnes, the report predicts. Fundamentally, softening steel demand could result in the country’s crude steel output falling by 3 million tonnes from 2023, leading to a fall in hot metal output.

Also, the consumption of steel scrap among steelmakers will increase this year, impairing the mills’ overall usage of iron ore in turn, the report pointed out.

Last year, China’s imported iron ore prices experienced fluctuations but eventually strengthened from the level in 2022, chiefly boosted by a brighter macroeconomic outlook for the country and healthy fundamentals of iron ore, Mysteel Global notes. These included the mills’ high output of hot metal while keeping internal stocks of raw materials low.

For example, on December 29 last year, the Mysteel SEADEX 62% Australian Fines index was at $140.55/dmt CFR Qingdao, after climbing by a total of $23.3/dmt from January 3 the same year.

The high prices of imported iron ore caused the financial circumstances of Chinese steelmakers to substantially worsen, as Mysteel Global reported. For example, also on December 29, the average loss suffered by steel mills in Hebei on rebar sales was Yuan 191/tonne ($26.6/t), Mysteel’s monitoring showed, compared with the profit margin of Yuan 30/t they enjoyed at the beginning of last year.

Steel output will fall more than 3mt if that thesis plays out.

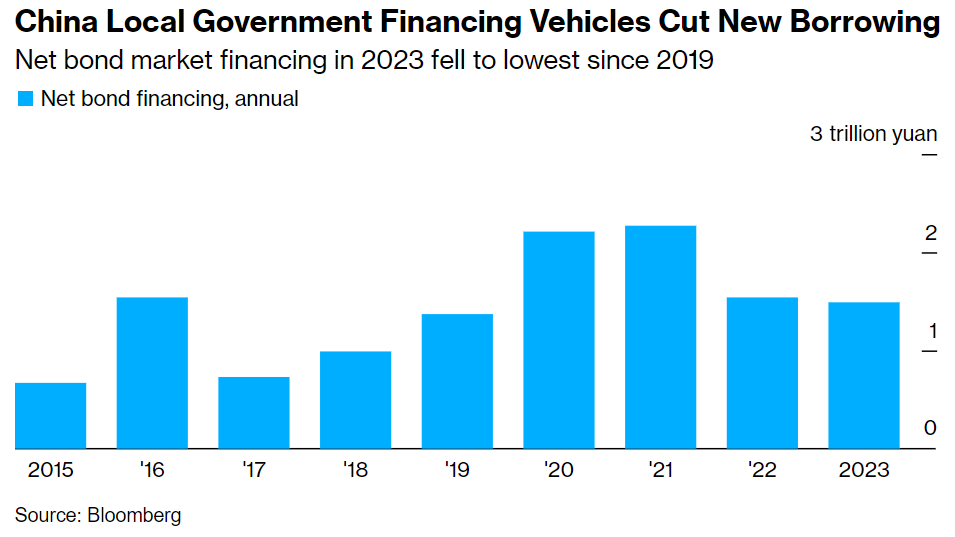

China may be printing money to build more public housing into the worst real estate glut in history, but infrastructure is a different story.

China’s efforts to lower risks from local government debt are likely to weigh on economic growth again this year as a national deleveraging campaign is expected to curb spending on investment projects.

The concern stems from a catch in the plan Beijing has put forth to lower the risk of disorderly defaults. China is helping local governments to refinance the off-balance sheet — or so-called “hidden” — debt accrued by state-owned financing vehicles. That seems to be mitigating the chance of a financial crisis this year, but those local authorities are also under unprecedented pressure to stop issuing additional debt.

Less borrowing by local government financing vehicles is “likely to be a drag on infrastructure investment and GDP growth this year,” said Adam Wolfe, emerging markets economist at Absolute Strategy Research.

We are still in the steel and iron ore peak season. Restocking and seasonal supply disruptions will not pass until April.

So, we may not see sustained price falls yet. Or, we will if the rebar demand crash is real.

My puts are timed for June.