Lol, this is fun to watch. During the GFC, the arrogant CCP was all “look at the decadent West fail”. Now, its property crash is far worse.

China’s escalating push to have its banking behemoths backstop struggling property firms is adding to a maelstrom of woes for the $57 trillion sector.

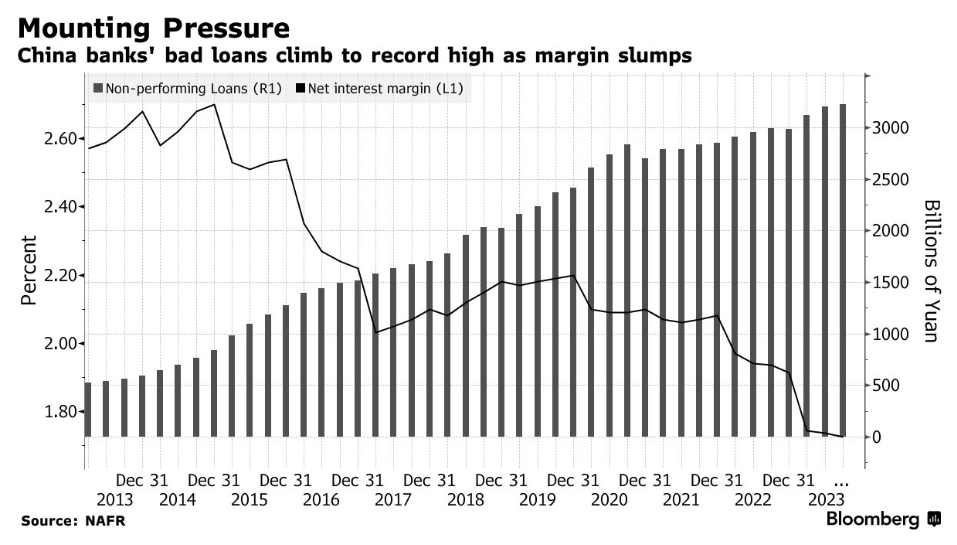

Already stung by soaring bad loans and record low net interest margins, lenders such as Industrial and Commercial Bank of China Ltd. may soon be asked for the first time to provide unsecured loans to developers, many of whom are in default or teetering on the brink of collapsing.

The risky lifeline threatens to exacerbate an already bleak outlook. ICBC and 10 other major banks may next year need to set aside an additional $89 billion for bad real estate debt, or 21% of estimated pre-provisions profits in 2024, according to Bloomberg Intelligence. Lenders are now weighing lowering growth targets and cutting jobs among possible options, according to at least a dozen bankers who asked not to be named discussing internal matters.

I cannot believe Beijing thinks this is a solution. The short-term unsecured debt will disappear down the credit black hole like rain on the moutainside. Sure, it may allow developers to complete a few extra projects, but that will not be enough to stabilise sales amid the ENORMOUS structural downdraft of falling prices, oversupply and crashing demographics.

This is treating an essential and unavoidable structural adjustment like a cyclical blip. All it will do is draw the banks closer to the black hole as bad loans rise and margins fall with falling interest rates:

Authorities have offered some relief to the banks, guiding them to trim deposit rates three times in the past year to ease margin pressures, and slashing reserve requirements twice this year to boost their lending capacity.

Those changes won’t be enough to offset the lending rate cut and arrest a margin slide, according to Fitch Ratings Inc. Bloomberg Intelligence expects the margin squeeze to deepen into 2024 and weigh on earnings, capping the profit growth at a low-single-digit at best.

Higher reserves for these ponzi-loans will have to come out of leading elsewhere as well.

If the banks acquiesce to the madness at all.

The PBoC is making far more sense:

China’s central bank governor stressed tolerance for slowing growth in the short term as the world’s second-largest economy transitions away from property and infrastructure toward new drivers of activity.

In an address to bankers in Hong Kong, People’s Bank of China Governor Pan Gongsheng said he was confident the economy will enjoy “healthy and sustainable growth” in 2024 and beyond, citing rising sectors like renewable energy. He also downplayed concerns over risks related to property and local government debt issues, after earlier meeting with top executives from banks including HSBC Holdings Plc. and Goldman Sachs Group Inc.

“The traditional model of relying heavily on infrastructure and real estate might generate higher growth, but it would also delay structural adjustment and undermine growth sustainability,” Pan said at the conference, organized by the Hong Kong Monetary Authority and the Bank for International Settlements.

“The ongoing economic transformation will be a long and difficult journey. But it’s a journey we must take.”

Sure is. But is the central bank speaking with forked tongue? In its quarterly statement, via Goldman:

On property and construction, the Q3 statement mostly repeated the recent measures. For example, the PBOC said it would step up financial support to the “three major projects”, namely urban village renovation, public facility construction and social housing construction, same as the Q2 report. Looking forward, the PBOC would focus on implementing existing policies. There is no mentioning of additional Pledged Supplementary Lending (PSL) despite the recent media report of RMB 1 trillion new PSL to the property sector. The release of November PSL data in early December can shed some light on the reliability of this media report.

Even in China’s centralised system, the titanic losses of an imploding $60 trillion market must land somewhere. But you have to accept what it is that you’re dealing with. Treating the issue like some cyclical blip and risking the core financial stability of the banking system is lunacy.

If you accept the adjustment is structural, then the response would be slashed interest rates combined with a massive fiscal intervention that separates and ringfences between good and bad developers, as well as providing broad and offsetting economic growth support. The housing market itself will shake out until affordability returns. The currency is let go.

But Beijing wants to keep up appearances, so it is risking a far worse outcome of permanently choked core bank balance sheets, deflation and ungrowth.

Japanication 101 on what not to do!

China is done.