There are irrational markets, and then there is iron ore.

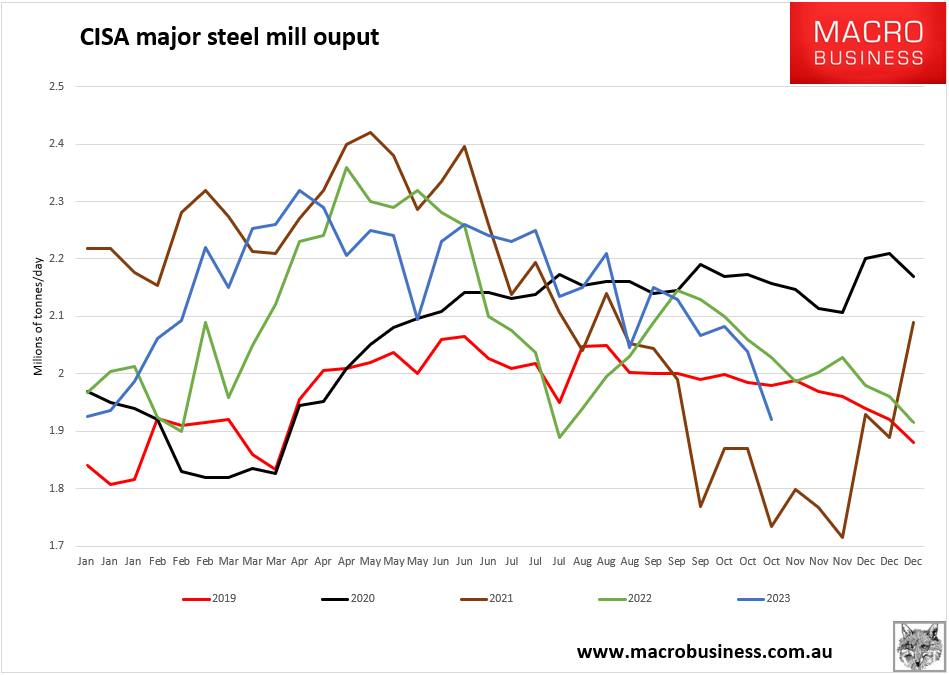

While iron ore has been spiking to prices silly enough to trigger a new supply response, Chinese steel output has been falling through the floor:

This is the classic Q3 destock that usually crashes prices. Not so this year, thanks to the Beijing policy panic.

Advertisement

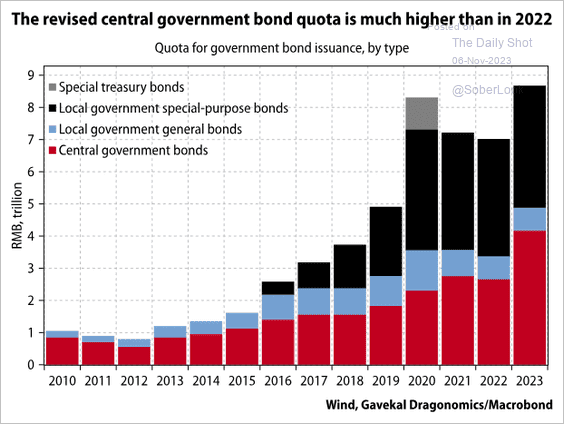

We will get some more infrastructure going into 2024 thanks to Beijing:

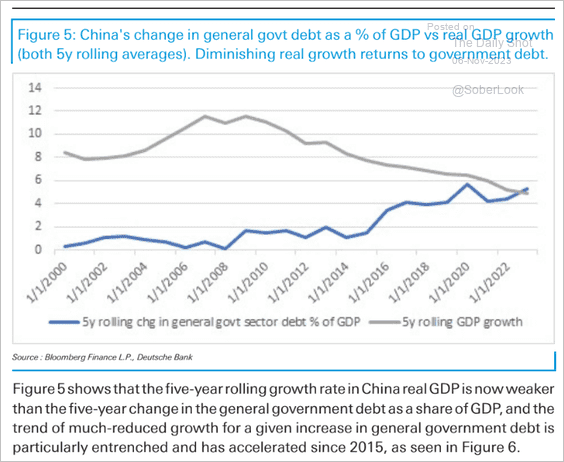

Not that it will really help anything:

Advertisement

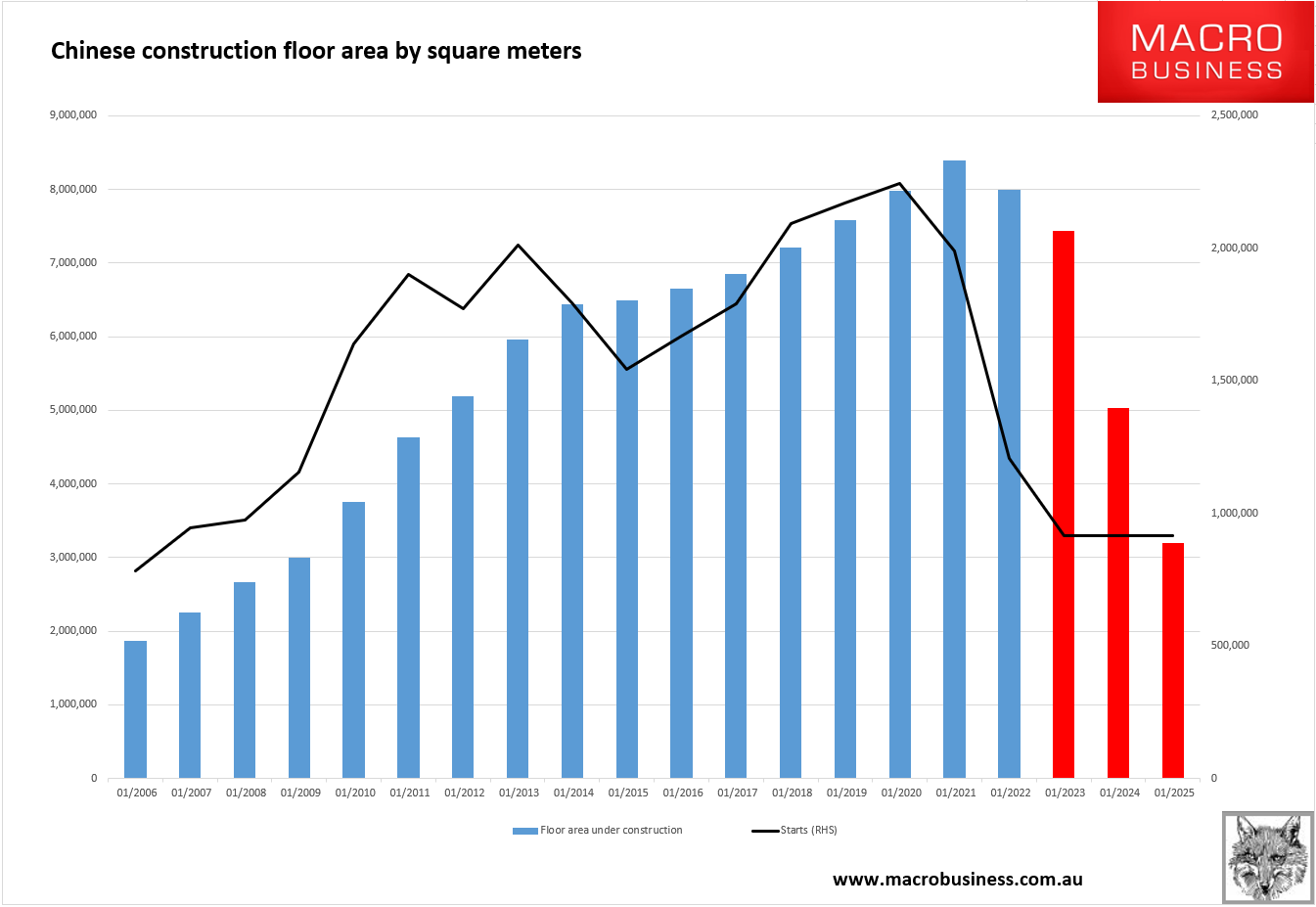

And the looming downdraft for construction remains immense:

Go figure.