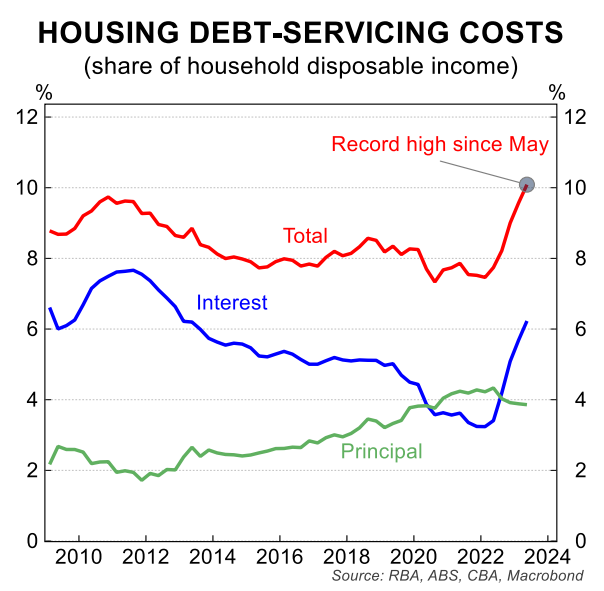

Australian households are already paying their highest share of income on record in debt repayments:

As shown above, around 10% of aggregate household income is being spent on debt repayments.

Given only around one-third of households in Australia are mortgage holders, this means that these households are carrying an unprecedented debt burden.

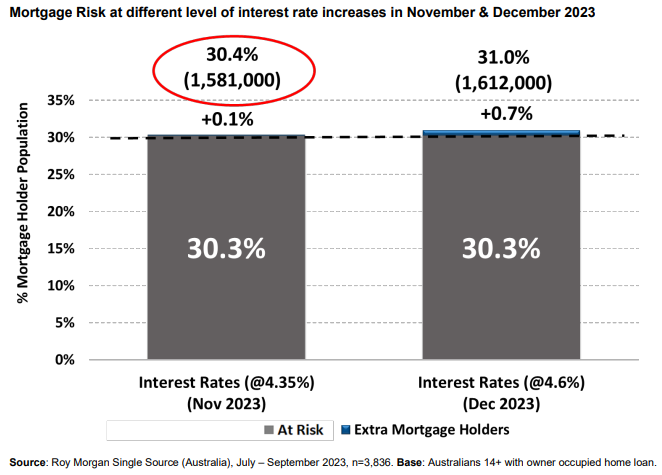

Earlier this month, Roy Morgan Research released data showing that 1.6 million households would fall into mortgage stress if the RBA lifted interest rates another two times:

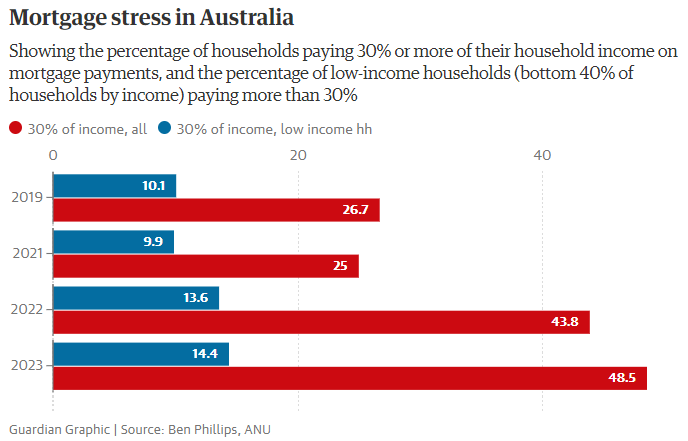

New research undertaken by the Australian National University (ANU) suggests that 48.5% of the nation’s mortgage borrowers will be in financial stress if the cash rate is increased on Tuesday.

This compares with 43.8% of mortgage-holders at the end of 2022, and just 26.7% in 2019:

Ben Phillips from the ANU’s Centre for Social Research & Methods says the bottom 40% of income earners who also have a mortgage are likely to be hardest hit if the cash rate rises to 4.35%.

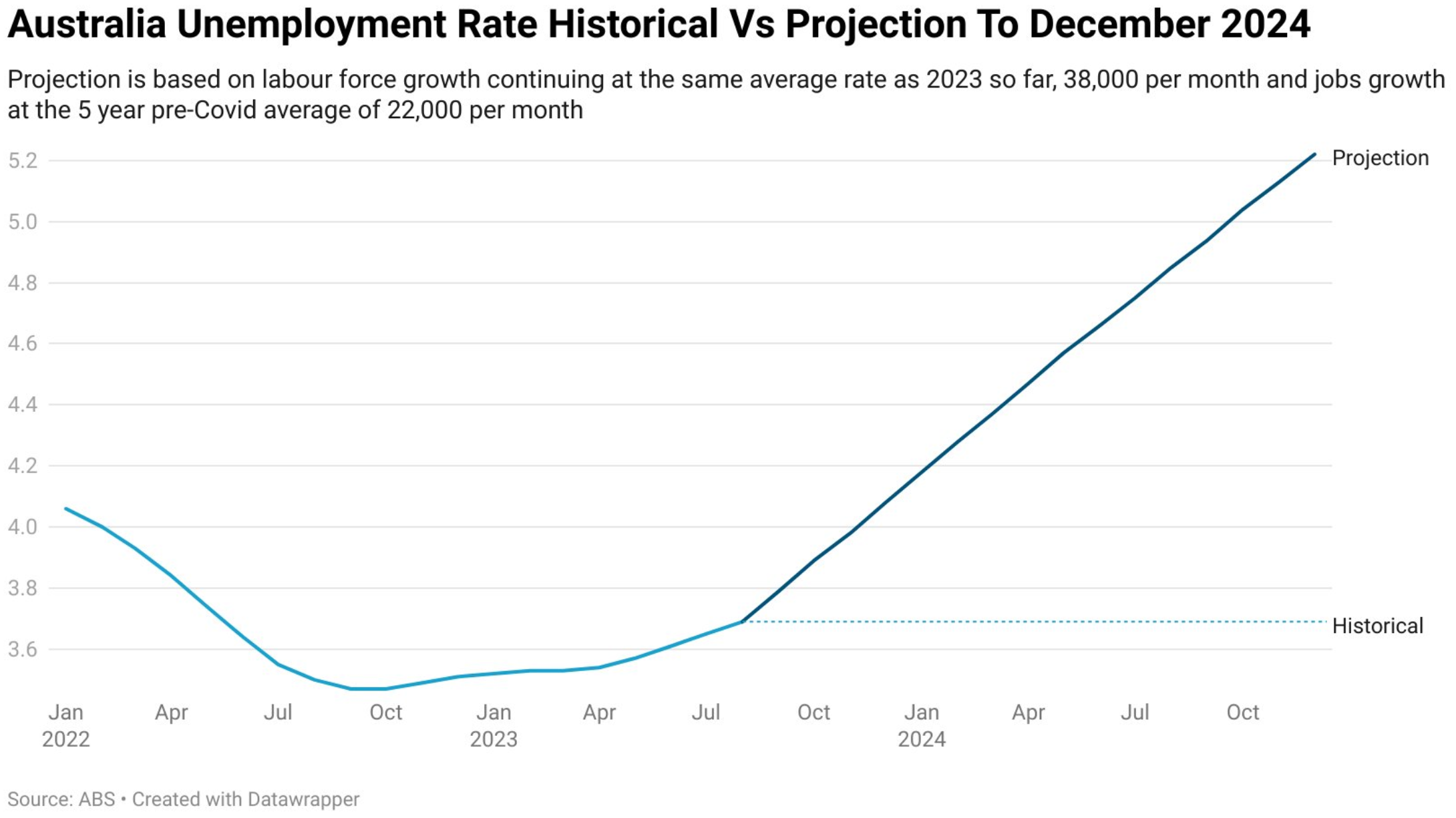

If Australia’s unemployment rate climbs as forecast by the RBA, then mortgage stress would deteriorate even further.

Independent economist, Tarric Brooker, estimated that if Australia’s labour supply continues to grow at around its current pace and jobs growth reverts to its five-year pre-pandemic average of 22,000 per month, then the official unemployment rate would increase to 5.2% by the end of 2024:

Source: Tarric Brooker

If the RBA lifts rates further and unemployment increases significantly, mortgage stress could surge.