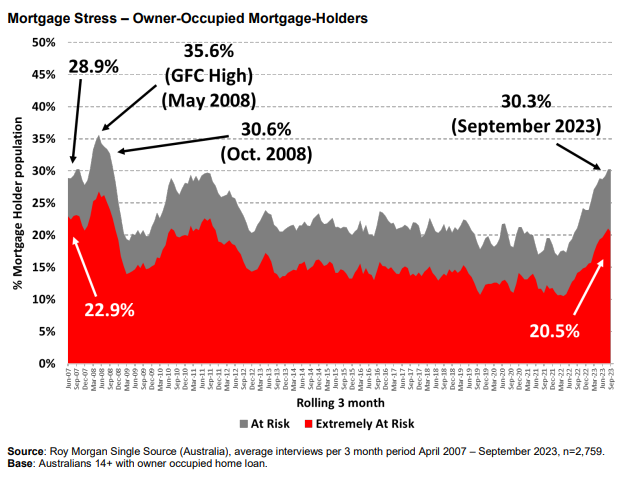

According to Roy Morgan’s September mortgage stress survey, 30.3% of owner-occupied families with mortgages are “stressed,” the highest level since October 2008, when the official cash rate (OCR) was 3.0% higher at 7.25%.

The number of Australians who are ‘At Risk’ of mortgage stress (1,573,000) has reached a new all-time high:

The number of mortgage holders considered ‘Extremely At Risk’ has now risen to 1,043,000 (20.5%), much higher than the long-term average of 15.3% over the last 15 years.

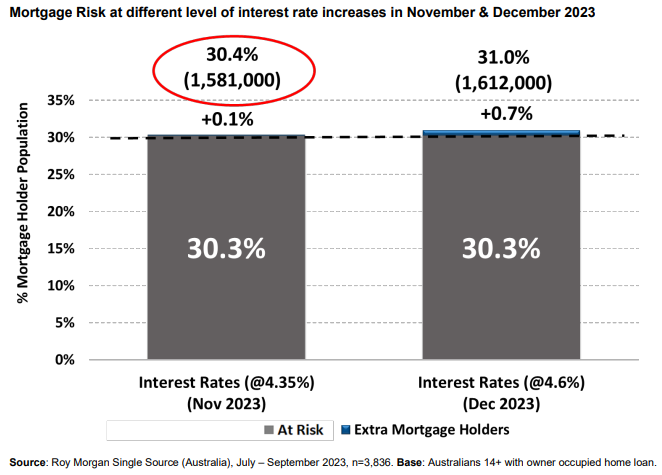

Roy Morgan has calculated the impact of two RBA interest rate rises of +0.25% in November (+0.25% to 4.35%) and December (+0.25% to 4.6%):

If the RBA raises interest rates by +0.25% in November to 4.35%, 30.4% (up 0.1% points) of mortgage holders, or 1,581,000, will be classified as ‘At Risk’ in November 2023, an increase of 8,000.

If the RBA raises interest rates by another +0.25% in December to 4.6%, 31.0% of mortgage holders, or 1,612,000, will be classified as ‘At Risk’ in December 2023, a 39,000 rise.

Morgan’s method is “a conservative model, essentially assuming that all other factors remain constant”.

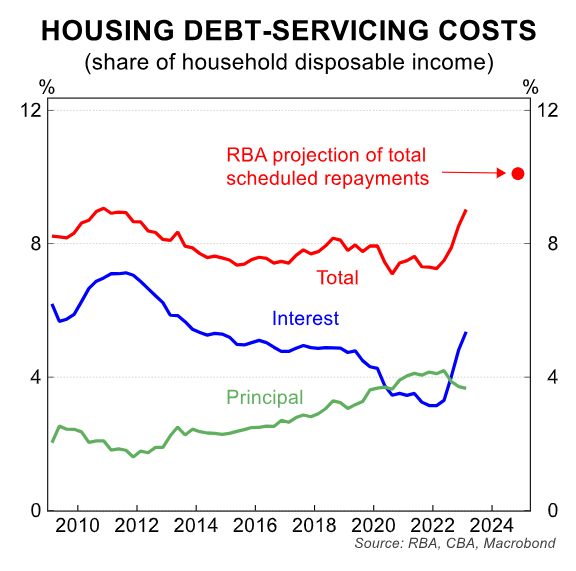

As a result, mortgage stress will increase as more borrowers migrate from fixed to variable rates.

The fixed rate mortgage reset still has further to run. This means that average mortgage repayments will continue to rise until mid-2024, even in the unlikely event that the RBA keeps the cash rate on hold:

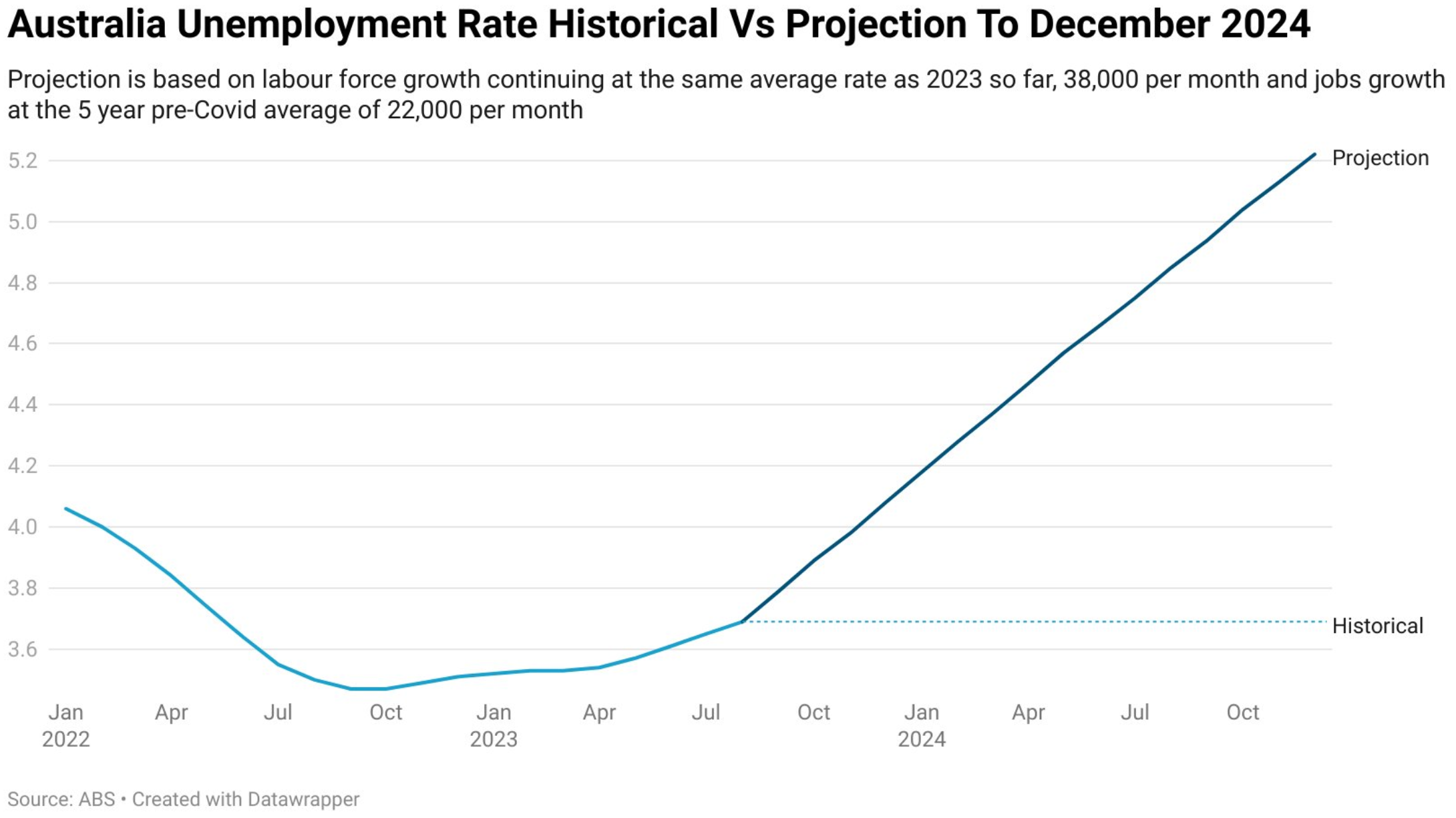

Furthermore, if Australia’s unemployment rate climbs as predicted by the RBA, then mortgage stress would worsen.

Independent economist, Tarric Brooker, estimates that if Australia’s labour force continues to grow at around its current pace and jobs growth simply reverts to its five-year pre-pandemic average of 22,000 per month, then Australia’s official unemployment rate would rise to 5.2% by the end of 2024:

Source: Tarric Brooker

Therefore, if the RBA tightens further and unemployment rises materially, mortgage stress could rocket.