On Tuesday, RBA governor Michele Bullock gave her maiden speech where she claimed that just 5% of variable rate mortgage borrowers in Australia have expenses that outweigh their incomes:

According to Bullock:

“The pressure facing indebted households is much greater for a small group of highly leveraged borrowers than for those with more modest levels of debt”.

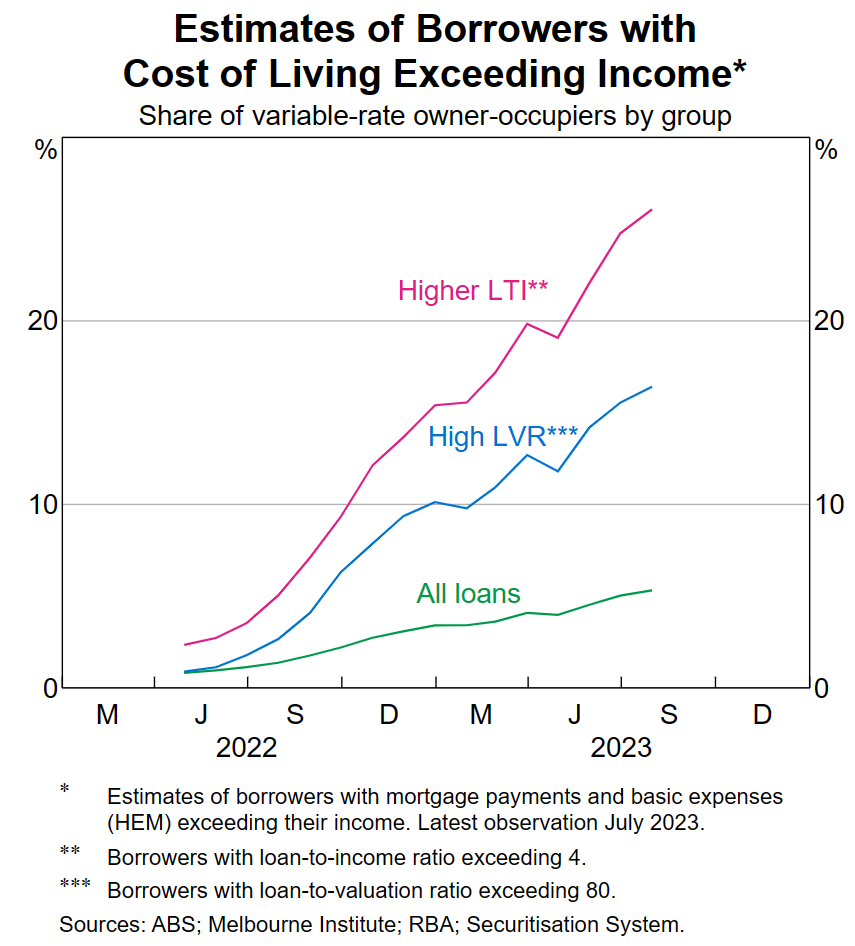

“About 5% of all variable-rate borrowers are estimated to be paying more for essential expenses and housing than they receive in income. But this rises to about 25% for highly leveraged borrowers – those with loans amounting to at least four times their income”.

It is important to note that the RBA has downplayed the situation by using the Household Expenditure Measure (HEM), which is a net-of-housing costs measure reflecting the median spend on absolute basics plus the 25th percentile spend on discretionary basics.

Rents and mortgage payments are not included in the HEM.

The HEM is based on the most basic standard of living, which would not be representative of most households with mortgages.

The above chart also assumes that households have no other debts, which seems unrealistic.

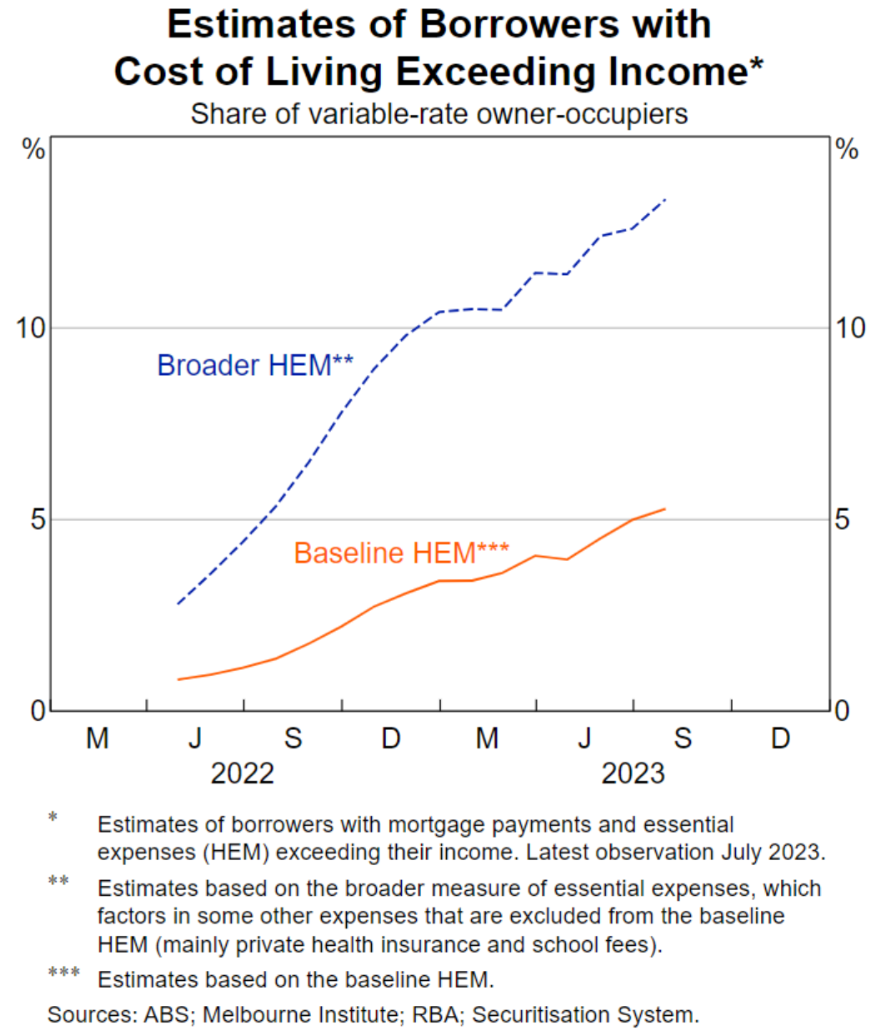

It is also worth pointing out that the latest RBA Financial Stability Review estimated that 13% of variable rate borrowers have a cost of living that exceeds their incomes once private health insurance and school fees are included:

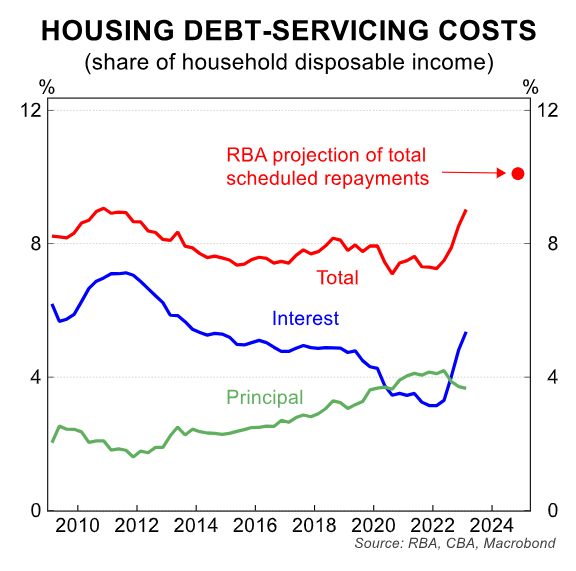

Australia’s fixed rate mortgage reset still has further to run. This means that average mortgage repayments will continue to rise until mid-2024, even in the unlikely event that the RBA keeps the cash rate on hold:

Given that Wednesday’s CPI inflation data came in hot, this seems unlikely. And if the RBA hikes further, it will obviously pull more households underwater.

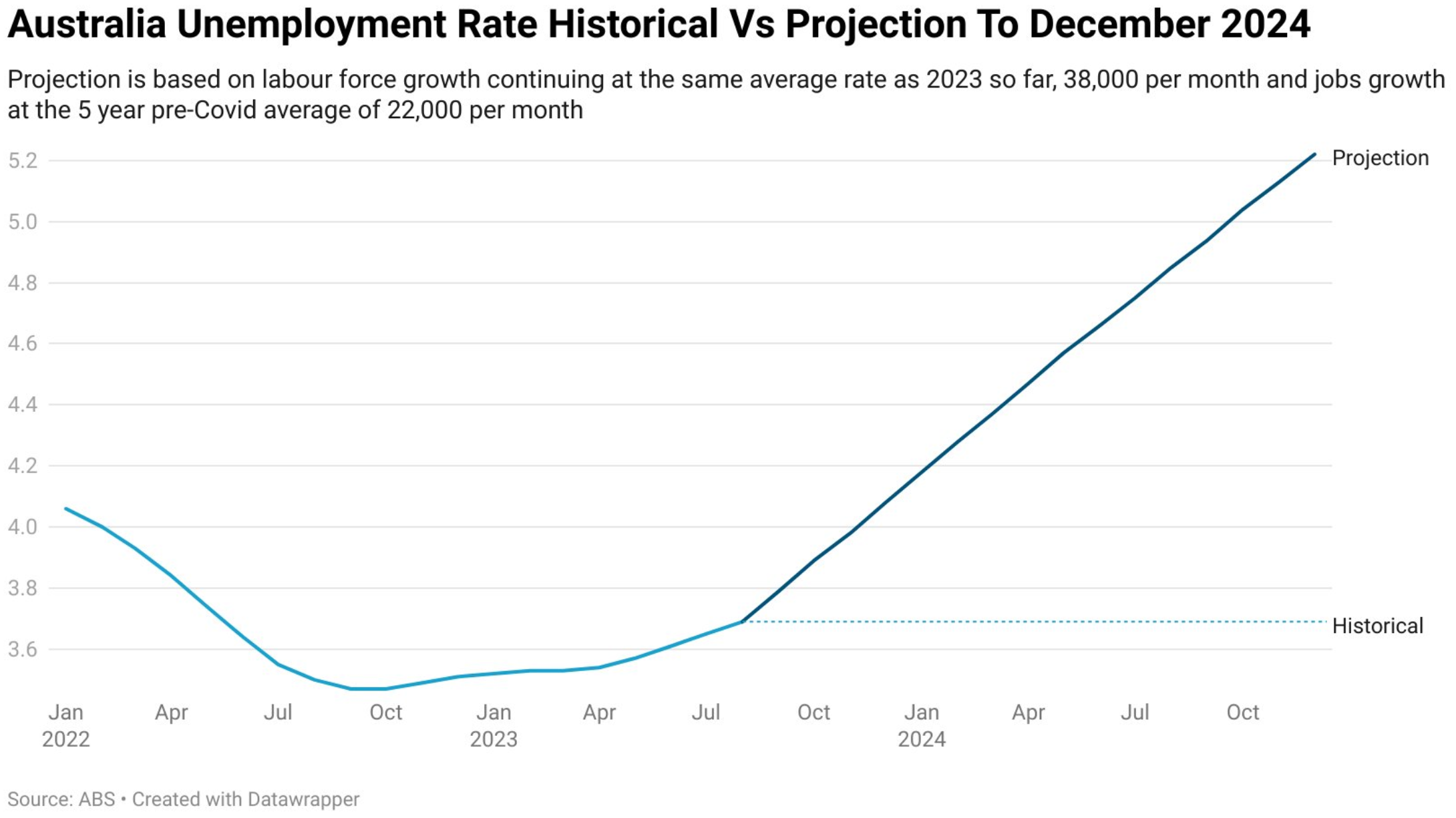

Finally, the biggest risk to Australian households is rising unemployment.

With record immigration, Australia needs to create around 37,000 jobs per month just to keep the unemployment rate stable (assuming a flat participation rate).

However, even if job growth was merely to slow to the pre-pandemic average of 22,000 a month, then Australia’s unemployment rate could easily surpass 5% within a year, as shown by the below chart from independent economist Tarric Brooker:

Source: Tarric Brooker

The prospect of further mortgage rate rises and rising unemployment could see large numbers of Australian mortgaged households get into deep strife.