Mortgage monster swallows one-in-five Aussie households

Chris Joye from Coolabah Capital believes “One-in-five borrowers is screwed” with debt repayments exceeding their incomes:

“13% of all borrowers have negative cash flows (or cannot afford to make their debt repayments after living costs, including private health and school fees). This is up from a mere 3% of borrowers in 2022”.

“If the RBA were to lift its cash rate to 5.1% in line with peers, it judges that 17-18% of all borrowers would have negative cash flow”.

“Whereas 13% of Aussie borrowers have negative cash flows net of essential living expenses, this jumps to an incredible 49% of borrowers with high loan-to-income (LTI) ratios and 32% of borrowers with high loan-to-value ratios (LVRs)”.

“These borrowers are much more likely to struggle to meet their essential spending needs”, the RBA says.

“In the RBA’s sanguine words, “there is also a smaller share of fixed-rate borrowers (less than 20%) who will roll off onto higher interest rates with much lower savings buffers, equivalent to less than three months of scheduled mortgage payments”.

“You can, therefore, spin this two ways: either most borrowers are fine or there are one in five who are screwed”.

“In particular, the RBA assesses that 18% of fixed-rate borrowers will have negative cash-flows once they roll to variable, assuming no more hikes (this number is 7% of borrowers if one uses a narrower definition of essential expenses excluding private health and school fees)”.

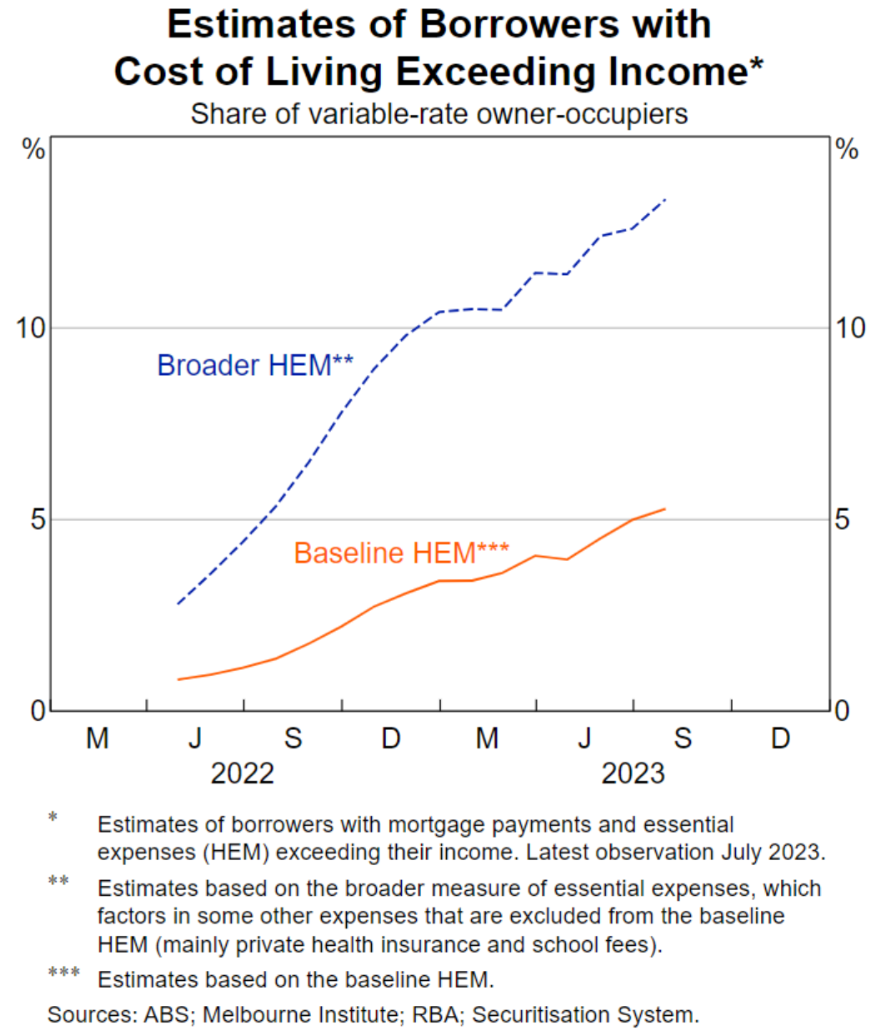

The below charts from the RBA’s Financial Stability Review tell the tale.

13% of variable-rate owner-occupier borrowers have essential spending and mortgage costs that exceed their income:

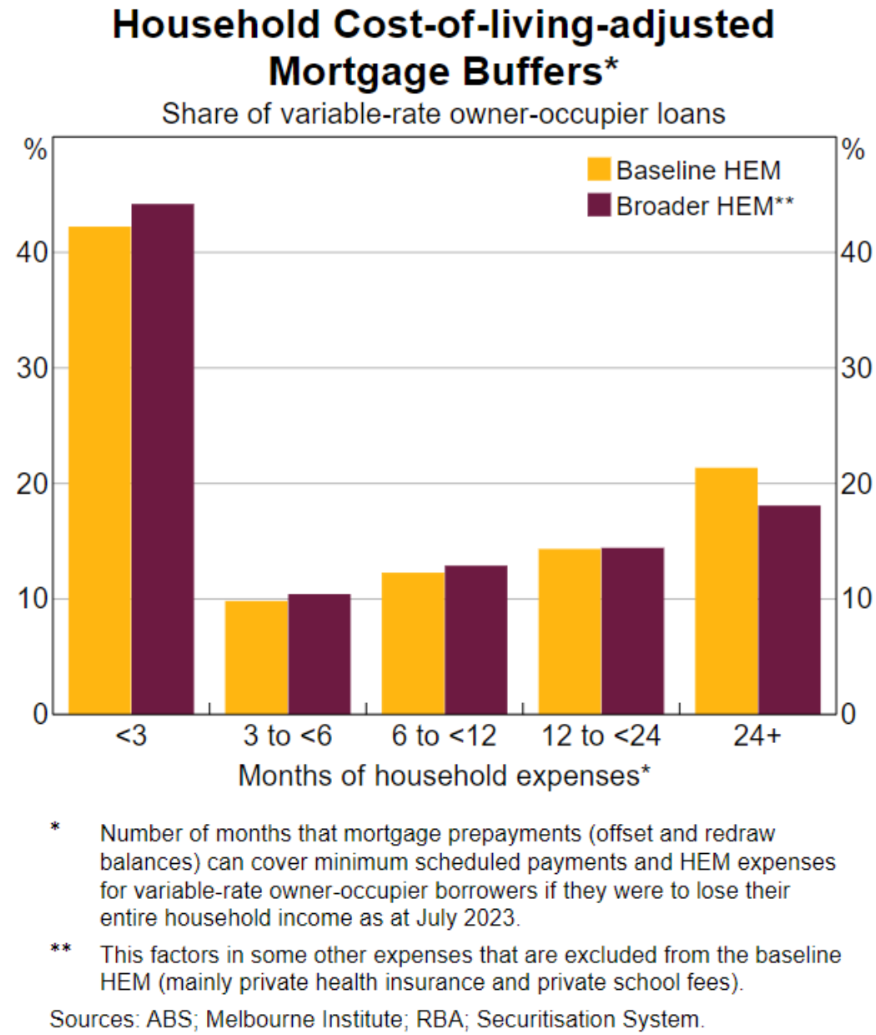

Moreover, more than 40% of households have less than three months savings buffer:

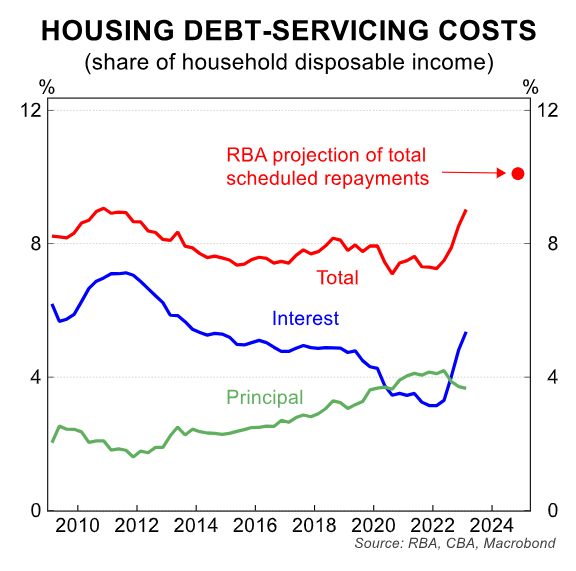

The fixed rate mortgage reset still has further to run, which means that average mortgage repayments will continue to rise until mid 2024 even if the RBA keeps the cash rate on hold:

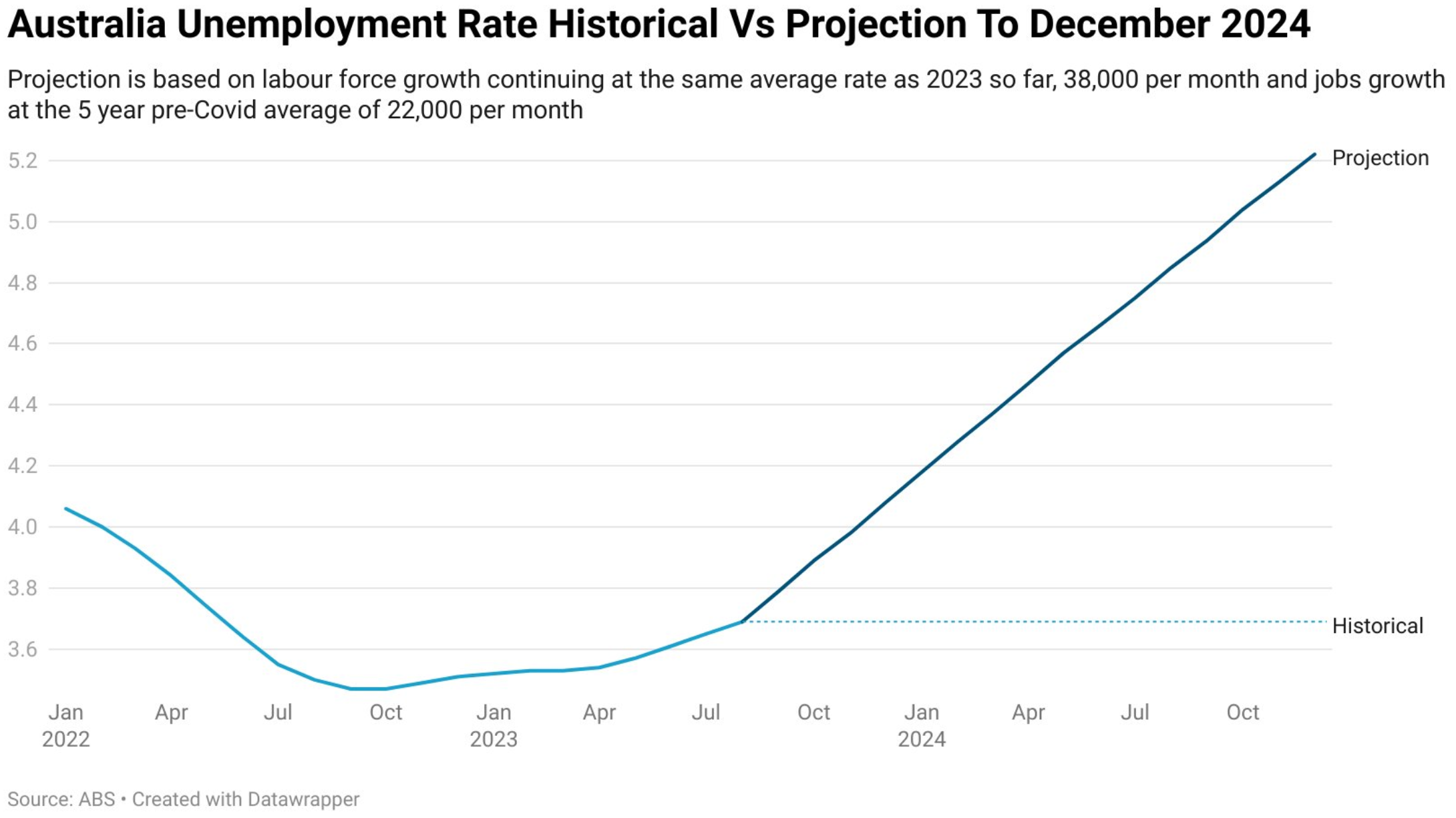

Ultimately, the biggest risk to Australian households is not further interest rate hikes from the RBA, but the prospect of a substantial rise in unemployment as the economy softens amid record labour supply growth from immigration:

If unemployment shoots back to 5%, then we could see large numbers of mortgaged households getting into deep trouble.