Iron ore is toast, says Australia via the Office of the Chief Economist.

- Spot iron ore prices have been volatile in the September quarter, but have generally moderated since the start of the year, driven by slowing global economic growth and China’s property sector weakness.

- Australian export volumes remain strong, with further greenfield supply from established and emerging producers expected to come online in the next few years.

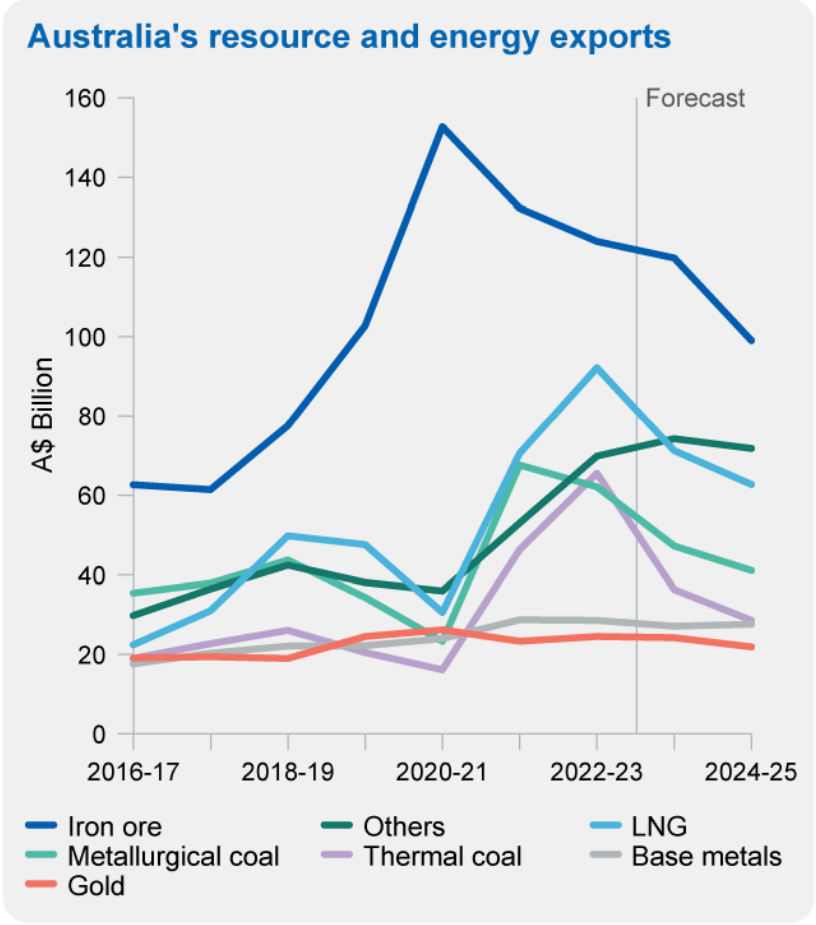

- Australia’s iron ore export earnings are expected to decline from $124 billion in 2022–23 to $120 billion in 2023–24, and to $99 billion in 2024–25 — driven by lower prices over the outlook period.

The property boom in China in the first two decades of the 21st century was underpinned by a growing population and large-scale urban migration.

Between 2002 and 2018, the growth in China’s urban population was stable at 20-22 million people each year (Figure 2.11). However, an apparent slowing in the rate of rural migration to cities, as well as a slowdown in fertility rates to 1.1 births per woman in 2022, has slowed overall urban population growth. In 2022, China’s urban population only increased by 15 million and the outlook suggests urban population growth will fall to 12 million by 2025.

Iron ore is only one of the projected falls. The same goes for the two coals and LNG, delivering a near halving of resource and energy revenues.

Resource and energy commodity prices fell (further) in the September quarter 2023, driven by supply and demand factors mostly pushing in the same direction. However, supply cuts by some major oil producers are helping to stabilise oil prices, and inventory replenishment by consumers is also helping support the prices of oil and other commodities.

Australia’s resources and energy export earnings during the outlook period are expected to be broadly in line with projections in the June quarter 2023 Resources and Energy Quarterly (REQ). After a record $467 billion in 2022–23, weaker growth in world demand and improving world commodity supply will cut prices and thus earnings to $400 billion in 2023–24, with another significant fall likely in 2024–25.

Despite the end of COVID restrictions, structural and cyclical factors are causing China’s growth to remain relatively weak. A weaker outlook for China is weighing on demand and commodity prices.

I agree with all of these forecasts. They will mean a substantial national income shock that:

- crushes nominal growth;

- hammers the budget, and

- pressures wages.

If the Albanese government’s response is to persist with mass immigration, the result will be the same after the 2012-15 shock.

The adjustment will be imposed on households as the budget and non-mining profits are protected.