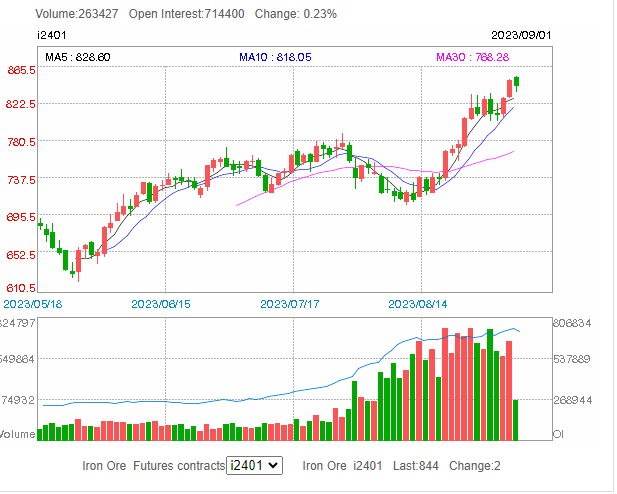

The crazy iron ore futures rally flamed out overnight:

Hooray!

“The latest flurry of macroeconomic stimulus largely boosted sentiment … and attention needed to be paid to the low inventories in the industrial chain,” analysts at Huatai Futures said in a note.

“If steel consumption improves further, demand for iron ore from steelmakers will be sustained.”

What stimulus?

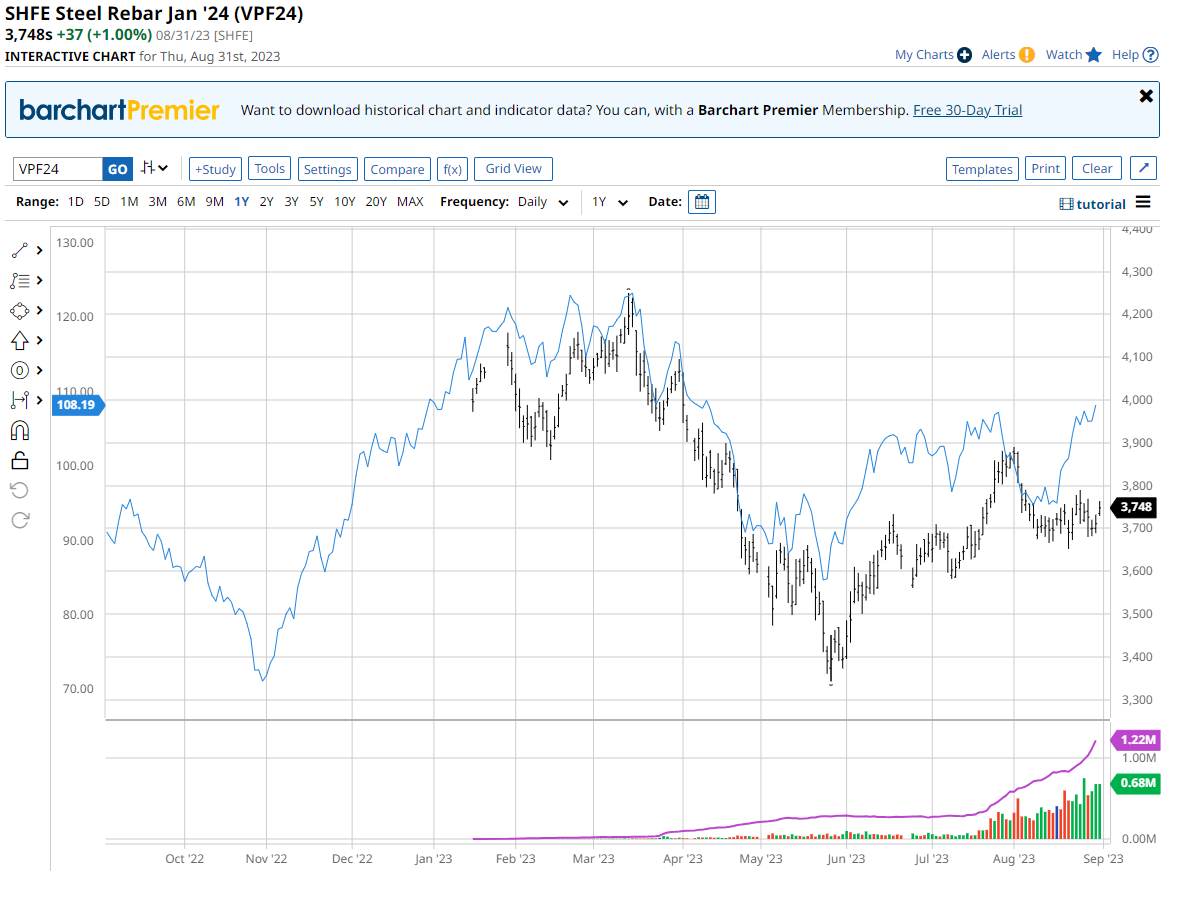

While iron ore futures have been having their private party, steel prices in China have hardly raised an eyebrow:

And steel inventories have been piling up:

Ironically, the one commodity that should be weakening by China’s worsening property crisis is actually performing well–iron ore has climbed to its highest in a month after a rally that has defied deepening pessimism over China’s debt-laden economy. Better demand prospects from the Chinese steel industry and rising speculation that steel mills in China will ramp up production ahead of the seasonal pick-up in construction activity (September-October) is supporting the market. Falling iron ore port inventories in China, which are currently hovering at their lowest levels since the end of August 2020, might also encourage domestic mills to start restocking. However, Chinese onshore steel demand remains heavily pressured–as data shows that steel inventories rose to 16.6MT in mid-August, up 3.6% compared to early August. As we documented last week, we believe it would be wrong to look at this recent iron ore price strength as evidence of a sustainably tightly fundamental pattern.

Which is why the Steel PMI is sagging again:

In summary, steel is piling up as demand falls away. Margins are negative as iron ore parties.

This is a recipe for official or unofficial material production cuts:

“I still believe some major Chinese mills will have to start slowing production in September or October, but it remains unclear to what extent China’s total steel output cuts will actually be implemented for the rest of the year,” a mill source said.

…”Even if some mills start cutting back in September, I don’t think steel prices could rise significantly, as deteriorating property investment and new home construction starts will undermine seasonal demand recovery,” a southern Chinese trader said.

Yep.