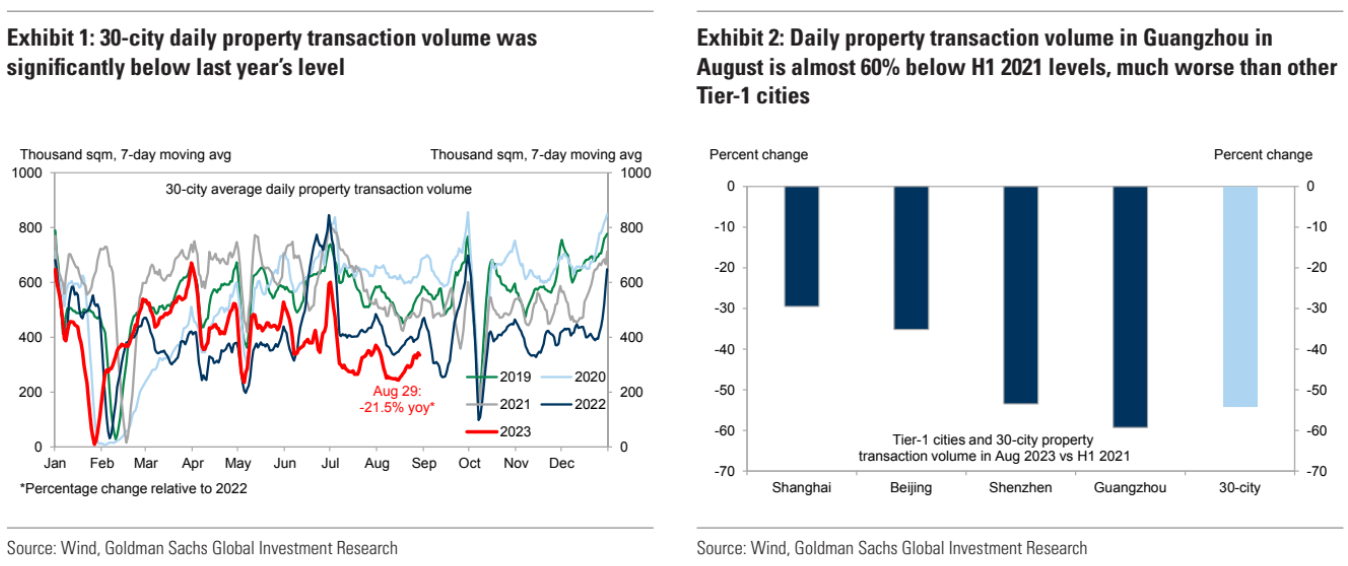

Two of China’s biggest cities lowered mortgage requirements for some homebuyers following central government guidance, fanning expectations that more will follow suit to arrest a record housing slowdown.

Goldman describes it:

What’s the likely impact? We believe this new housing easing measure (“认房不认贷”), if broadly implemented in large cities, may provide a modest growth impulse to the property market in large cities. The major beneficiaries will likely be upgraders in large cities, as they can sell their existing small homes first, and buy larger ones later, on more favorable mortgage conditions. However, the progress of home upgrading depends on whether their existing home sales can proceed smoothly. Moreover, we note not all cities have room to ease their local housing policies, as many lower-tier cities haven’t imposed such restrictions earlier, and some Tier-2 cities have already eased these restrictions early this year. That said, recent housing easing measures in Guangzhou and Shenzhen may carry meaningful signaling effect and boost market confidence to some degree. We see a high possibility that more Tier-1/2 cities will follow suit to ease their local housing policies in coming weeks, but given the persistent weakness with lower-tier cities and private developers, we maintain our view of an “L-shaped” recovery for the housing market.

China allowed large cities to cut down payments for homebuyers and encouraged lenders to lower rates on existing mortgages in its latest attempts to halt a slide in the country’s residential property market.

The nationwide minimum down payment will be 20% for first-time buyers and 30% for second-time purchasers, according to a joint statement from the People’s Bank of China and National Administration of Financial Regulation on Thursday. The mortgage-rate cuts will be negotiated between banks and customers. Both policies go into effect Sept. 25.

A modest rise in sales will do nothing, given developer business models need boom revenues to feed the ponzi business model otherwise starts will keep falling.

Moody’s Investors Service downgraded embattled Chinese developer Country Garden Holdings three notches to Ca, piling on more pressure on the distressed company whose liquidity crisis has shaken the nation’s financial markets.

The rating agency’s outlook on the developer remains negative, as it estimates that the company doesn’t have sufficient internal cash sources to address its upcoming offshore bond maturity, given its weakening sales and sizable maturing debt over the next 12 to 18 months, it said in a statement. Country Garden’s long-term corporate family rating was downgraded by Moody’s to Ca from Caa1.

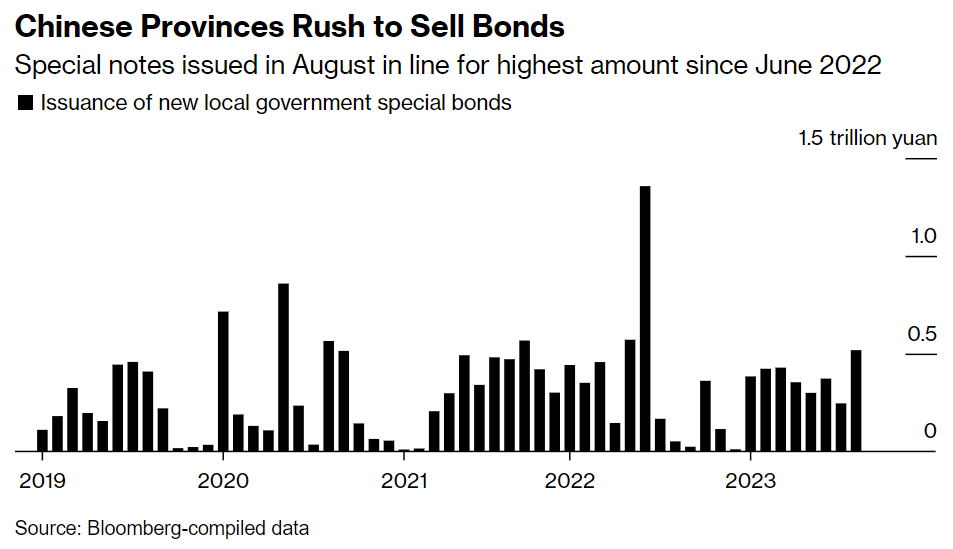

China’s local governments are accelerating the pace of borrowing for infrastructure investment, a move that could help lift economic growth while also putting pressure on financial markets.

Provincial governments sold the most amount of special bonds in more than a year this month, according to Bloomberg calculations. And with Beijing setting a September deadline for the regions to issue their remaining allocation for the year, analysts are expecting a boost to debt supply next month.

Advertisement

As often said, bond quotas are usually exhausted by the end of October. Moreover, the quota is 5% lower than in 2022.

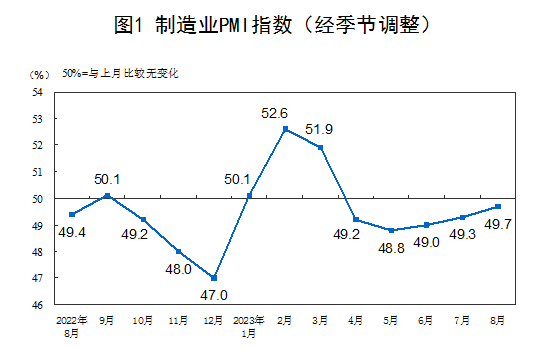

The manufacturing PMI improved marginally:

In August , the manufacturing purchasing managers index ( PMI ) was 49.7% , an increase of 0.4 percentage points from the previous month, and the manufacturing boom level further improved.

With some new domestic demand:

Advertisement

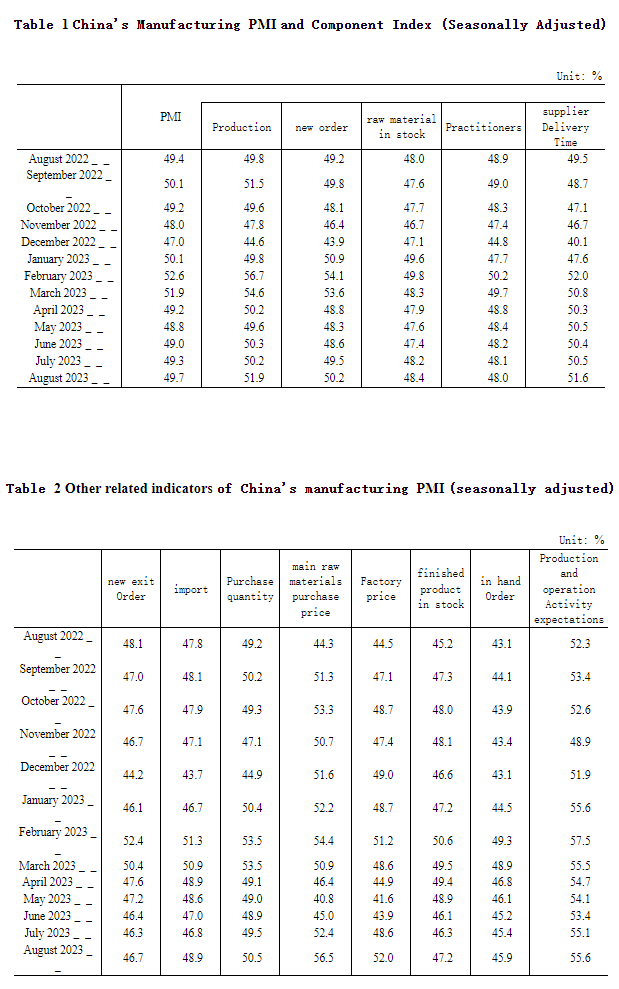

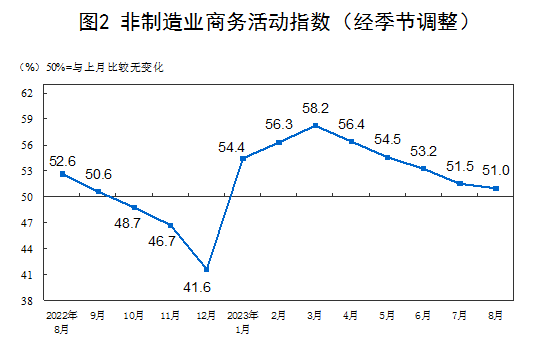

The Services PMI was less promising:

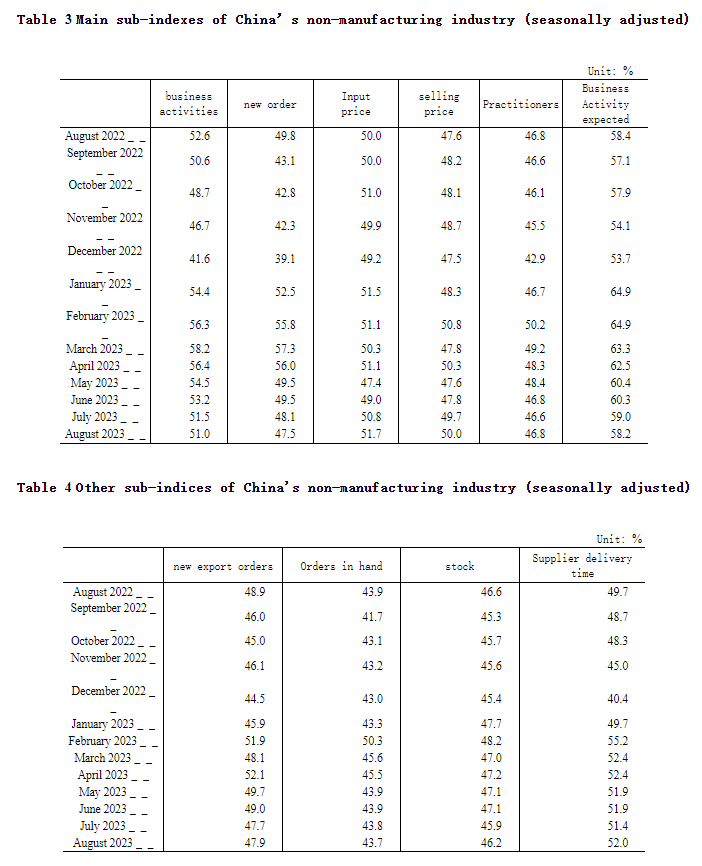

In August , the non-manufacturing business activity index was 51.0% , down 0.5 percentage points from the previous month and still higher than the critical point. The non-manufacturing industry continued to expand.

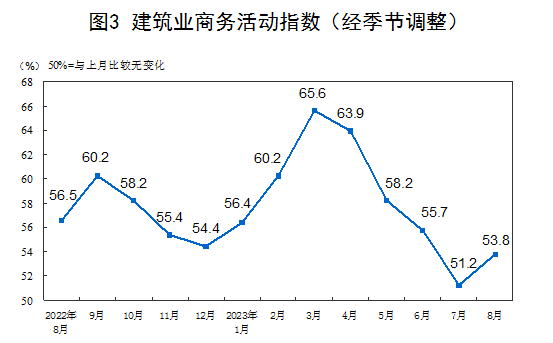

In terms of different industries, the business activity index of the construction industry was 53.8% , an increase of 2.6 percentage points from the previous month; the business activity index of the service industry was 50.5% , a decrease of 1.0 percentage points from the previous month.

Led by failing domestic demand:

There was a small lift in construction but it remains very weak in context:

Advertisement

Over the years of the property boom, the pattern was always the reverse of today. Relentless price rises and purchases of floor area ignored every prudential tightening and every rate hike. Until authorities were fed up with rising inflation and squashed the boom with a dramatic tightening.

Now, it is the reverse. Prudential easing, rate cuts, local government bonds, none of it is enough to raise the sinking ship. Only all-in will save it, and that is not coming.

Advertisement

However, the fake stimulus has sucked in some. Bloomberg has been cheerleading every unstimulus and its editors are now triumphant:

One reason China is failing to dislodge those feel-good vibes is it’s not actually that bad right now. Iron ore, the one commodity that should be getting hammered by the country’s property crisis, is actually doing rather well as central government investment on infrastructure like railways accelerates.

Meanwhile, the surprising strength of the US economy both papers over the cracks in global growth and also distorts the view of China’s markets.

A few more things may be dulling the impact of China’s slowdown. First, the retreat of international money we’ve already seen from Chinese markets means exposure among fund managers is lower than before and probably still bearishly positioned, so any bad economic news has less impact on global portfolios.

Second, there may be some “bad news fatigue” as the credit crisis and slower economic growth have been rumbling on for years now. You could argue the economy is still more or less on target for the government’s goals — it’s just less good than we’ve been used to.

Third, there’s some good news in that Chinese officials are introducing an array of incremental steps to support markets, relations with the US have eased and local-government financing vehicles, which top the market’s worry list, have mostly performed well so far.

There’s also the view that a China slowdown is helpful for the rest of the world in terms of disinflation. The impact may be slight but every little helps feed the “soft-landing” narrative.

So China may just bump along the bottom from here or even form a base from which markets can climb. The PMIs had hints of optimism and — though the longer-term view may suggest a lack of upside — for now it would need an unexpected shock to catch global attention.

I’ll take that bet. I don’t know how it will all end. But it does not take Albert Einstein to understand that the outright collapse of the largest asset class on earth, the implosion of the greatest construction boom and demand source for commodities in history, and the seizure of the worst credit excesses the world has ever seen will end in pain.

Advertisement

It may not break out as a global credit shock as the CCP buries the bodies as furiously as it did during COVID. But that will come at the price of the end of Chinese growth.

40% of S&P500 revenues come from offshore. 60% of tech. China drives that growth everywhere.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.