Goldman has a great note on the Chinese long-cycle credit event:

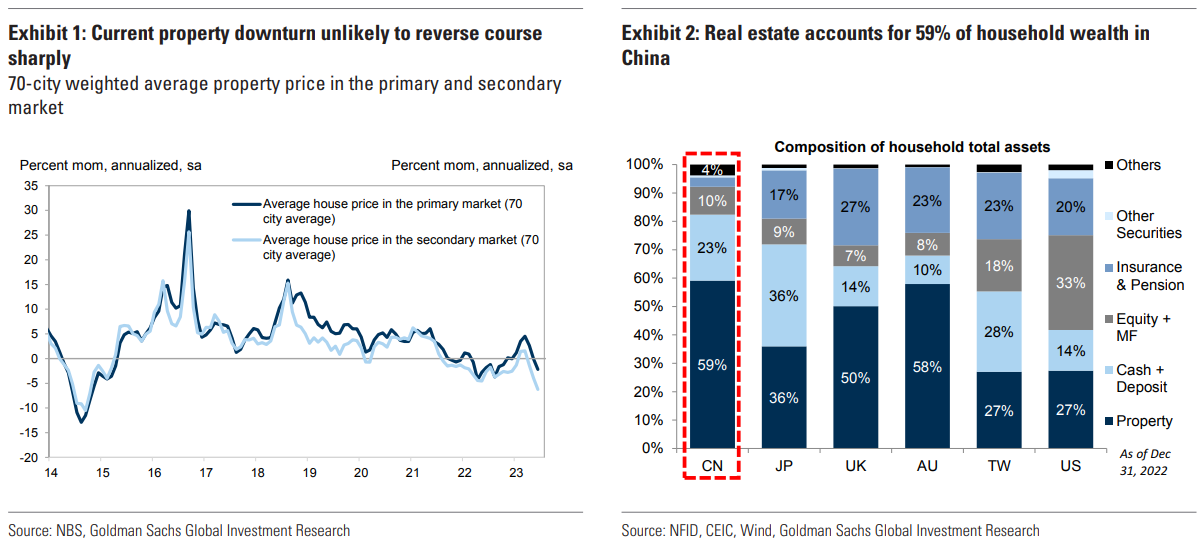

This time is different – adjusting to an L-shaped path. The latest downturn in the China property sector originated in late 2020 with the introduction of the “Three Red Lines”, measures aimed at restricting the amount of financing available to property developers based on satisfying three leverage metrics. But unlike previous downturns, policymakers have not introduced significant policy easing to reflate the sector and reverse the slump. To us, it is clear that this time is different. We believe policymakers are unlikely to revert to large stimulus, as they seek to diversify away from credit-driven real estate development as a major engine of growth, and given that the demographics fundamentally point to the need for a smaller developer/property sector. Furthermore, there have been meaningful shifts in sentiment from homebuyers, as expectations of pricing appreciation have been eroded and heightened defaults have led to reduced appetite to purchase pre-sold, unbuilt properties. Our China economics team are assuming an “L-shaped” path for the property sector in coming years, estimating that the property weakness will likely be a multi-year growth drag for China, with continued (but diminishing) negative impact to headline GDP growth in the coming years.

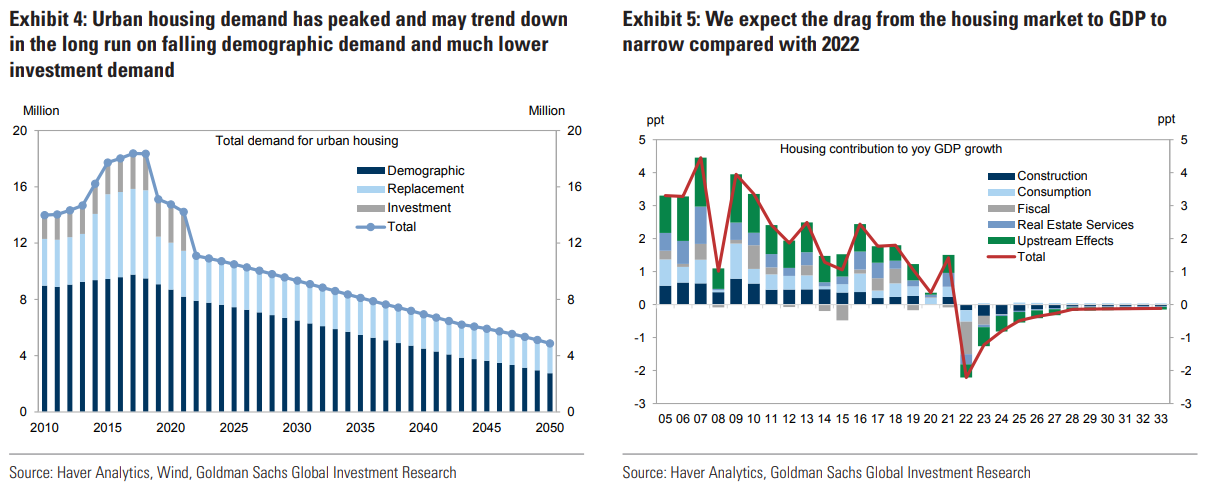

Adjusting to the oversupply. One important challenge facing China policymakers is the long-term demand outlook. Our China economics team estimates that annual urban housing demand peaked at 18mn units in 2017, will fall to 11mn in 2023, and reduce further to 9mn units by 2030. On the supply side, estimates from our China property team shows that on average over the past decade, the number of urban housing units increased by 13mn units per annum. With falling demand, the supply of residential properties will need to contract to prevent aggravating the oversupply of housing. That said, adjustments to lower supply have already begun, as the growth in property new starts have been in negative territory since the start of 2021. With new starts falling, the supply of new homes should fall in the coming years.

USD 8.4tn of property sector debts, stresses concentrated amongst developer borrowings. In 2008, mortgage borrowing and developer indebtedness were relatively low, with total real estate sector debt equating to 16.6% of GDP. The subsequent years saw very sharp increases, with total property related borrowing rising to 48% of GDP at the end of 2022. The total amount of property sector debts outstanding reached RMB 58tn (USD 8.4tn) at the end of last year, of which RMB 39tn (USD 5.4tn) are in mortgage loans and RMB 19tn (USD 2.6tn) are from developer borrowings. Although the growth in mortgage loan has outpaced that of property developer debts, we see the risks from mortgage loans as manageable, as they are full recourse in nature, have relatively high down-payment ratios, and with no mortgages allowed beyond the second home. The focus of our analysis, therefore, concentrates on property developers’ borrowings.

Near-term focus on ensuring sufficient flow of credit. Over the past two years, a major focus by China policymakers has been on ensuring sufficient financing to developers for project completions on presold but unbuilt properties. That said, whilst there has been progress made on ensuring the delivery of housing, the magnitude of such development appears insufficient to meaningfully boost buyers’ confidence. Amidst tight financing conditions for developers and mounting local government debt concerns, construction risks persist. Our China property team estimates RMB 1.77tn funding will be needed for project completions in 2H23 and 1H24, and of that, RMB 740bn relate to privately owned developers that face high liquidity pressures. Our micro level analysis on privately owned developers’ balance sheets indicates significant deterioration in liquidity over the past two years, reinforcing our view that near term support will unlikely deviate from providing sufficient credit flow for project completion needs.

Over USD 2tn in inventory liquidation needed to handle the stock problem. With nationwide project completions for 6M23 rising by 16% yoy and GFA new starts down 30% yoy, the excess supply is gradually normalizing. To us, policymakers should shift their attention from dealing with the “flow” credit issues towards the “stock” problem – namely, the excess inventory currently sitting on developers’ balance sheets, including raw land and undeveloped projects. Our China property team has estimated the liquidation value for the inventory sitting on stressed developers’ balance sheets is between RMB 15tn (USD 2.2tn) in their base case scenario, and RMB 20tn (to USD 2.9tn) in their bull case. For stressed developers to engage in comprehensive restructurings of their balance sheets, we believe large-scale asset liquidations will be needed. This will require liquidating projects amongst mostly privately owned developers, and with many of the projects located in lower tier cities.

A piecemeal or big bang approach? Awaiting direction from central government. Restructuring efforts towards the China property sector have, thus far, been largely piecemeal. Much of the policy easing has been directed towards project completions, and forbearance has meant banking sector NPL recognition has been slow. The inability of stressed developers to liquidate their inventories means that many are operating as “zombie” companies. With existing institutions unable to absorb the volume of potential stressed assets, a continuation of this piecemeal approach would suggest a long timescale to restructure the industry and their indebtedness – not dissimilar to what occurred during Hainan’s real estate bubble in the 1990s. In turn, this very gradual pace of deleveraging would suggest a longer, multi-year drag on the country’s economic performance. A faster approach would require bolder action by the central government, with possible solutions including setting up new nationwide asset management companies and/or recapitalizing existing institutions to acquire stressed assets, amongst others. Furthermore, given the lower risk buffers amongst smaller banks, it may also require a broader approach to inject capital into weaker parts of the banking system. At the current juncture, we see no indications from policymakers that they will shift towards a more “big bang” approach – and therefore, we maintain our view that restructuring the China property sector will likely be on a gradual, multi-year approach.

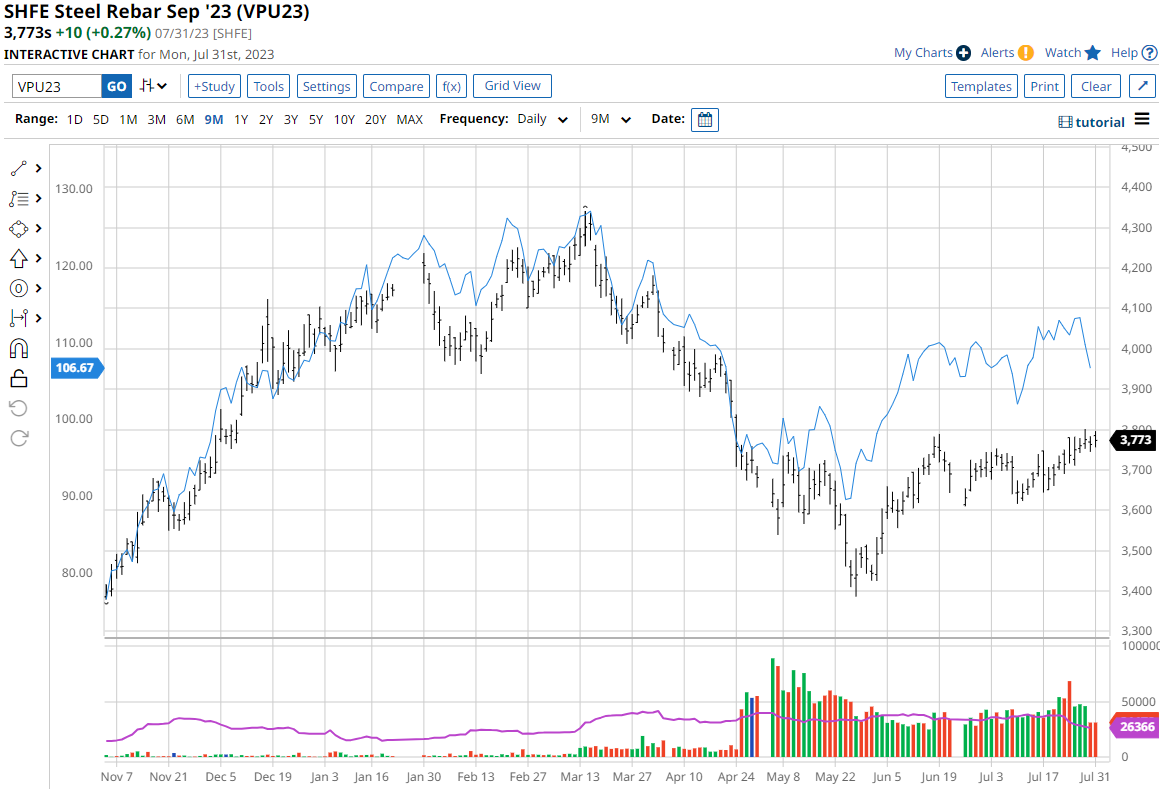

China property USD bond prices reflect a multi-year downturn. We believe current market pricing reflects the “L-shape” path forecast by our economists, highlighting a significant amount of credit differentiation. For China property HY, spreads are at 4,629bps, and above levels seen in late 2021 when Evergrande concerns first emerged; for China property IG, the current spread level of 423bps is largely back to late 2021 levels. We see value in China Property IG, in particular the longer-dated bonds, and adopt a neutral stance for China Property HY, with an emphasis on the strongest developers. The YTD default rate for China Property HY is at 16.2%, and we forecast FY23 default rate to reach 28%, though with risks firmly tilted higher. For the defaulted bonds, recovery prospects are highly idiosyncratic, and much will depend on each company’s capital structure, quality of assets, and support from major shareholders, amongst other factors. We believe restructuring prospects will only become clearer once there are indications of how policymakers will address the “stock” problem of excess inventory. Without a clear picture on a comprehensive plan to manage the stock problem, we see limited catalysts for the distressed bonds to rally at the current juncture.

There’s the truth for you. An immense imbalance needs to be rationalised. The only question is fast or slow. My guess is slow, which will sap growth endlessly rather than deliver shock and recovery.

Advertisement

For twenty years, iron ore has shocked bullishly. The next twenty will be the bearish mirror image.

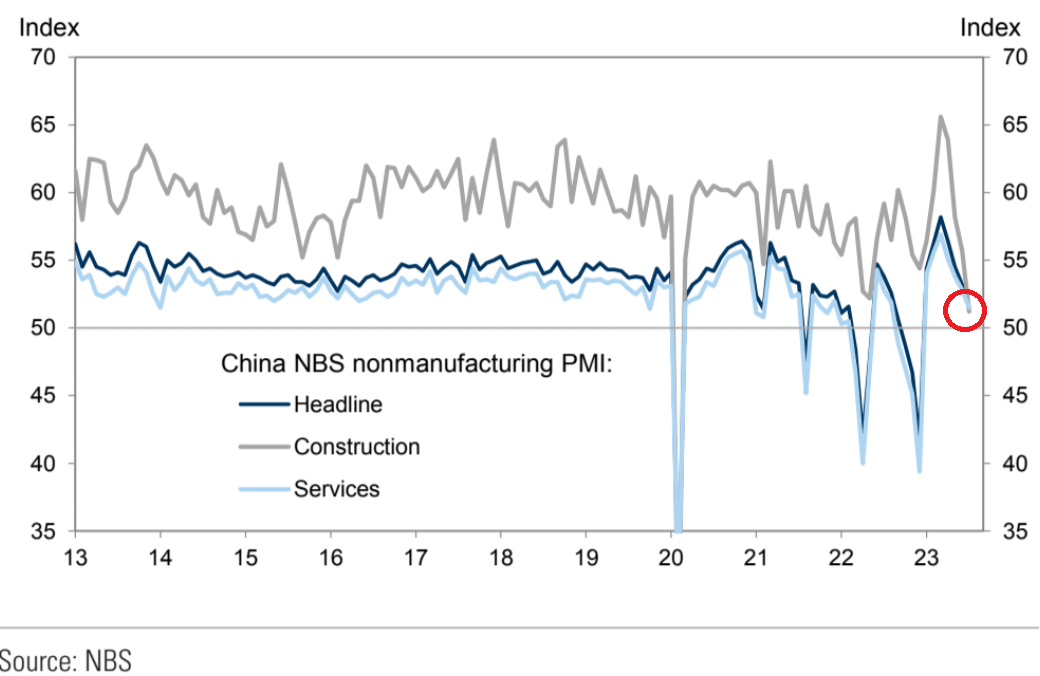

In the short term, the only chart that mattered in yesterday’s PMIs was this one:

Advertisement

The Construction PMI is the lowest anybody can remember outside of the initial COVID shock and is about to turn negative, signalling contraction.

This is consistent with the completions and infrastructure pulse running down just as we head into iron ore seasonal weakness in Q3/4.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.