Goldman has got one commodity right at last.

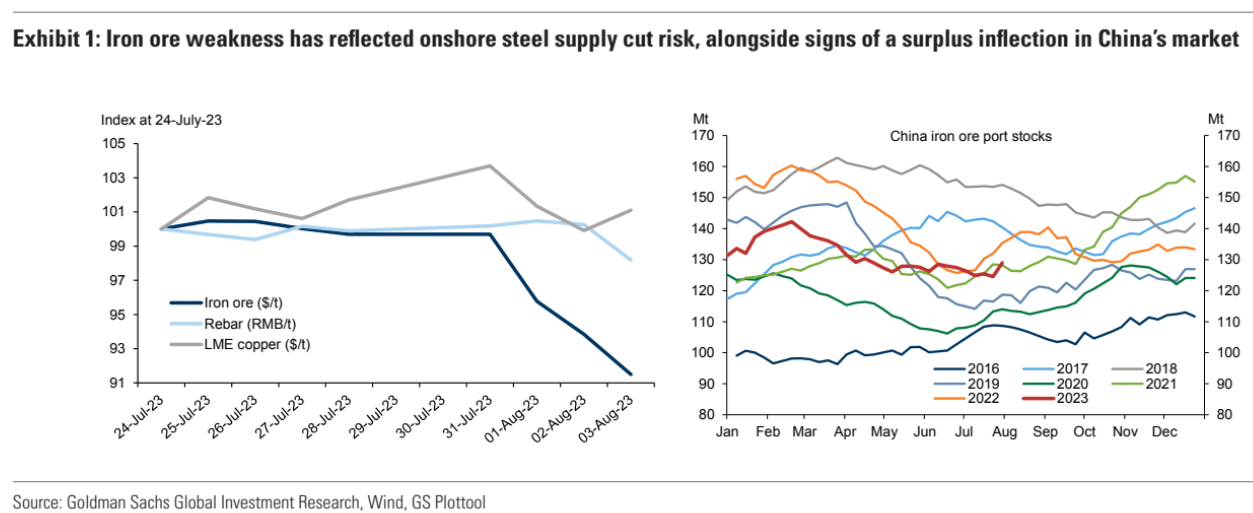

Iron ore downside. Amidst the broad industrial metals post-Politburo fade, the most significant sell-off has been in iron ore.

The benchmark active SGX contract has now fallen 11% from its late July high, now standing just above the $100/t level.

The immediate catalyst for this move lower has been related to increasing risk of China policy intervention impacting steel production and in turn iron ore demand.

There have been media reports this week that China’s NDRC have been communicating with provincial governments in the country regarding enforcing steel production cuts.

Thus far the only province known to have communicated on cuts to steel producers has been Yunnan, with a flat (or lower) full year production target.

If that was replicated at a national level, it would imply just over a 50Mt cut in crude steel output in H2-23 versus H1-23, in turn a 65Mt loss in iron ore demand on the H/Hbasis.

So far that remains a risk, though if such cuts were to take place this would provide a clear bearish demand shock to the iron ore market.

Indeed, even without these policy cuts, we continue to base case a 68Mt iron ore surplus in H2.

Crucially we see a weaker margin environment for China’s steel exports now acting alongside negative seasonality as a headwind to onshore steel production over H2, which set against stronger supply trends, should inflect the market into surplus from now.

We continue to expect a lower price environment to prevail from here with 62% iron ore averaging $90/t over H2.

My own view is it is the weakness of stimulus that is doing it but bring on the cuts!