Chinese regulators have sought for years to get to grips with the $2.9 trillion trust industry, a corner of the country’s shadow banking sector that offers bigger returns than regular bank deposits but can be fraught with risk. Their fears were underlined in August when trust companies linked to financial giant Zhongzhi Enterprise Group Co. missed payments on several high-yield investment products. The revelation comes at a sensitive time, with many investors already worried about the state of the world’s second-largest economy.

1. What are these trust companies?

They are loosely regulated firms that pool household savings to offer loans and invest in real estate, stocks, bonds and commodities.

2. What is Zhongzhi?

Zhongzhi is a shadow banking giant with interests in trust companies, wealth management and private equity.

3. What’s gone wrong at Zhongzhi and Zhongrong?

Three firms said on Aug. 11 that they had failed to receive payments on products issued by companies linked to Zhongzhi, including Zhongrong.

4. What is the government doing about it?

China’s banking regulator, the National Financial Regulatory Administration, set up a task force to gauge the outstanding debt and risks at Zhongrong, according to people familiar with the matter.

5. Why does it matter to China?

Investors have been alarmed by the country’s slow pace of recovery from Covid-related restrictions and persistent weakness in its giant real estate sector. Loans extended by Chinese banks fell to the lowest level since 2009 in July, in a sign of waning demand from businesses and consumers. One of the nation’s largest property developers, Country Garden Holdings Co., is on the brink of default. The crisis at Zhongzhi feeds perceptions that poorly regulated parts of China’s banking industry may be ill-equipped to cope with those problems…

6. Is the property crisis at the root of Zhongzhi’s problems?

It’s not yet clear. What we do know is that China’s trust companies offer investment products linked to real estate developers, and in the past have defaulted on them.

Does the Pope shit in the woods?

Has anyone heard of a situation like this before? A real estate bubble going bust followed by sudden problems in a shadow banking system? Caixin reveals more:

Since the turn of the millennium, there has been a mushrooming of infrastructure construction, real estate investment, and mineral resource projects in China. This comes as the country successfully hosted the 2008 Beijing Olympics, implemented the 4 trillion yuan economic stimulus plan in 2008, and released the National Mineral Resource Plan (2008-2015) in 2009. Traditional banking loans, bonds, and stocks, or standardized financing channels, fell short of meeting the burgeoning demand.

Given the potential high returns of these projects, as well as the rising demand for capital, the issuance of non-standard asset management products through trust channels became increasingly popular. The trust industry, legally licensed by the government, experienced explosive growth in China. Meanwhile, a special “pooling” practice (资金池业务) in financial products emerged, gradually extending its influence from trust industry to broader financial sectors such as banking, securities, and insurance. (Editor’s note: Pooling refers to the consolidation of funds raised through separately issued wealth management products into a big pool of funds, and investing it as one or several portfolios)

Regulators have flagged the flaws in the “pooling” model in wealth management, which include using new borrowings to repay old debts, mixing financial product operations, short-term fundraising for long-term investment, and separation from the actual yield of the underlying assets. But, despite repeated attempts by regulatory bodies to issue directives to standardize or even prohibit such practices outright, they’ve often been loosely enforced, likely due to the numerous financial institutions involved in regulation or due to the model’s previously positive role in promoting market development. In any case, pooling became a grey area in China’s financial regulation.

However, a broader financing channel has emerged — asset management companies. Subsequently, the emergence of third-party financial advisory firms and private wealth management companies from these asset management entities has propelled the industry to an entirely new level.

Over the past decade in China, asset management, especially private wealth management, has grown dramatically. This boom not only filled investors’ coffers but also offered lucrative returns for sales personnel, far outstripping those in other financial sectors. The accumulated wealth effect from the industry’s growth catalyzed a shift, with a surge of trust and bank wealth management staff embracing the private wealth management wave. The industry also attracted a vast number of high-net-worth individuals as investors, further fueling its rapid development.

Initially, these wealth management products had underlying assets with credit enhancement guarantees. However, as the industry rapidly expanded, the scale demanded more “innovative” solutions than just single trust plans for fundraising.

The previously halted “pooling of funds” model resurfaced in a more covert fashion, gradually transforming into a sort of pseudo-pool model, with funds raised not tied to any specific projects. Funds under the guise of so-called “subscription-based trust product investments” transitioned from wealth management companies to the group company’s headquarters, then were directed to various investments under the group. Hence, a closed-loop of self-financing and self-investment within those financial groups was formed.

The trust defaults may set off a vicious cycle on POE (privately-owned enterprise) developers’ onshore debt.

This follows that rising concern of developer defaults weakens investment sentiment and, as a result, trust companies may not be able or willing to roll over existing real estate-related products.

The probability of banks bailing out trust investors is low, in our view. But if funding support from trusts on work-in-progress housing projects recedes, banks may be asked to fill the funding gap. We consider this another form of national service risk for banks.

The prospect of bailing out trust investors is high. There is no way Beijing can let the shadow banking system implode. But while it farts around thinking it will not have to, it will get much worse. Remember Lehman.

Advertisement

Meanwhile, the real economy is dying as credit demand shrivels. Goldman:

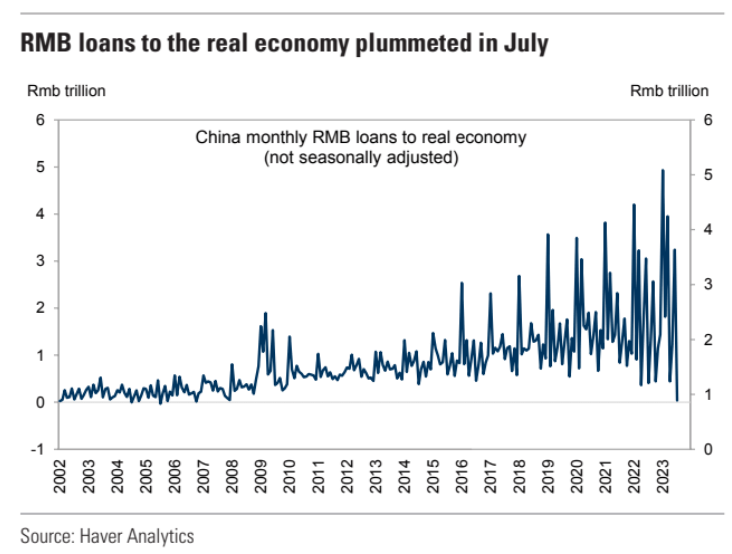

Very weak credit growth: The July money and credit data released last Friday missed expectations by a large margin. New flows of Total Social Financing (TSF)were only RMB 528bn in July, not even half the size of consensus expectations(RMB 1100bn). RMB loans to the real economy plummeted to RMB 36.4bn, the lowest since 2006. Even taking into consideration the more pronounced seasonality observed in recent years, last week’s print was no doubt soft. It underscores the weak demand in the economy and the need for the government to implement more easing measures.

Are you getting the picture? China’s property bubble supply chain, from credit to mining construction inputs, is the largest Ponzi scheme in the history of the cosmos. This is how China grew so fast for so long.

Advertisement

It is going bust. Anybody thinking that it is contained is delusional. Nobody knows how bad it will get, but the risk is there for it to touch every corner of the global economy.

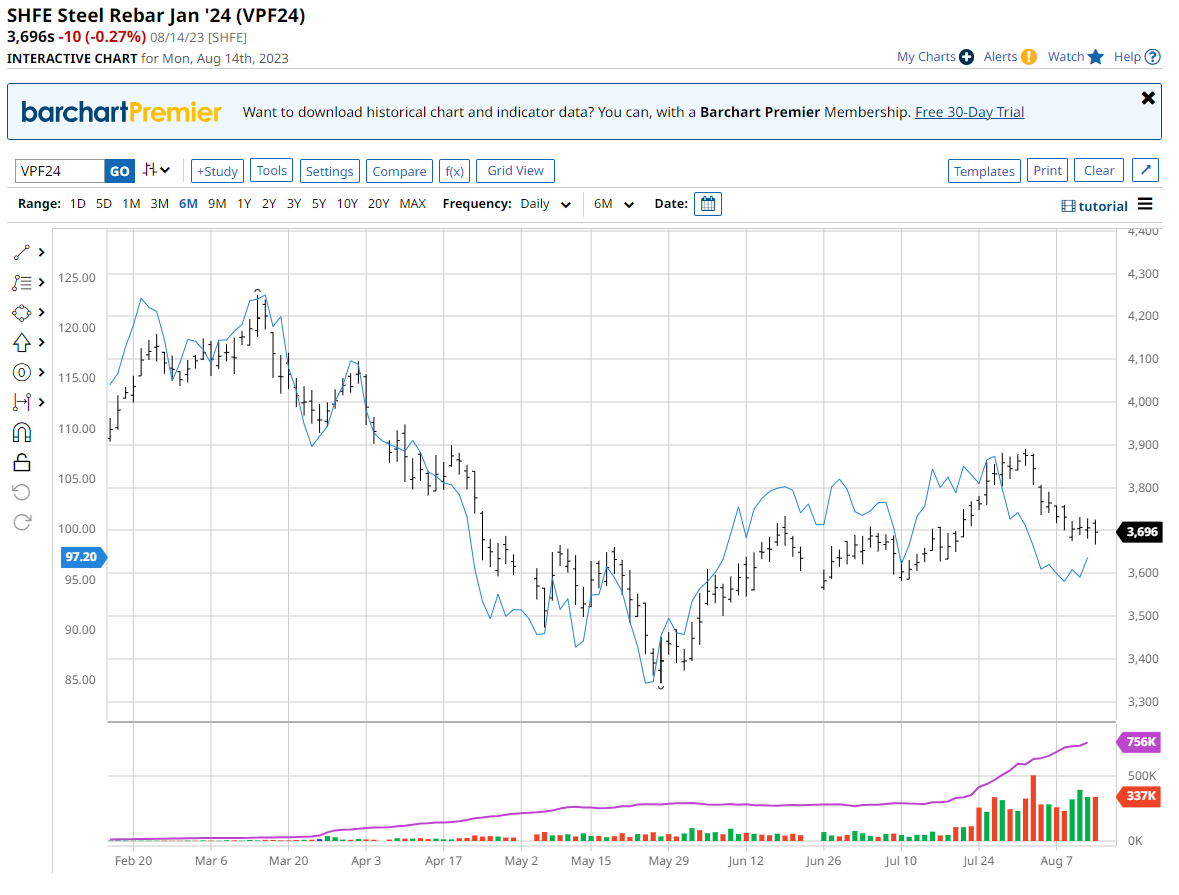

Meanwhile, the number one beneficiary of said Ponzi scheme continues to trade as if it knows what nobody does:

Advertisement

Iron ore at $100 has discounted nothing but sunny uplands of forever Ponzi.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.