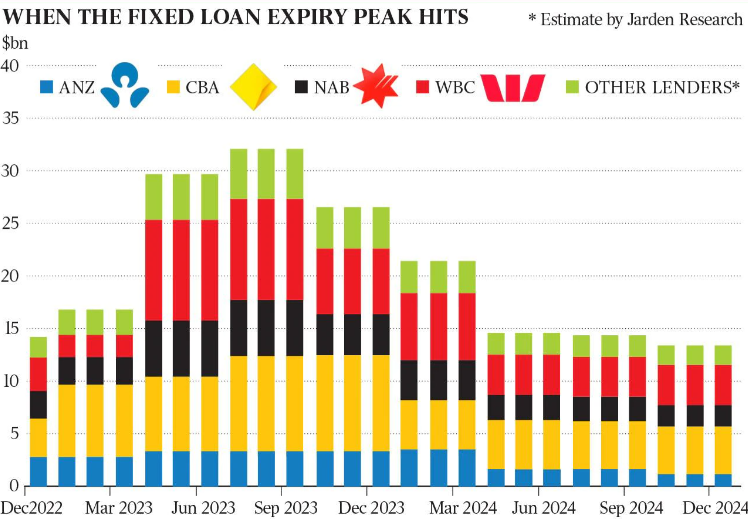

Jarden’s chief economist Carlos Cacho says an estimated $32 billion worth of mortgage loans are expected to be refinanced each month during the September quarter, in what has been described as the “peak of the mortgage shock”.

Meanwhile, some $550 billion worth of fixed-rate loans are slated to roll over to significantly higher variable interest rates over the 15 months to March 2024.

This rollover will increase the average monthly repayment on a $750,000 mortgage from $3,180 to $4,830. This assumes a borrower moves from a fixed rate of 2% to a variable rate of 6%.

“There is still a tightening policy coming in the next six months, even if the RBA sits on its hands”, Cacho said, citing that only around 75% of the RBA’s dozen interest rate hikes have been passed onto borrowers.

NAB chief economist Alan Oster likewise said that the number of people rolling off ultra-low-interest home loans in the second half of this year will be double that of the first half:

Oster warned that the overhang of fixed-rate mortgages made predicting the depth of the spending downturn exceedingly difficult.

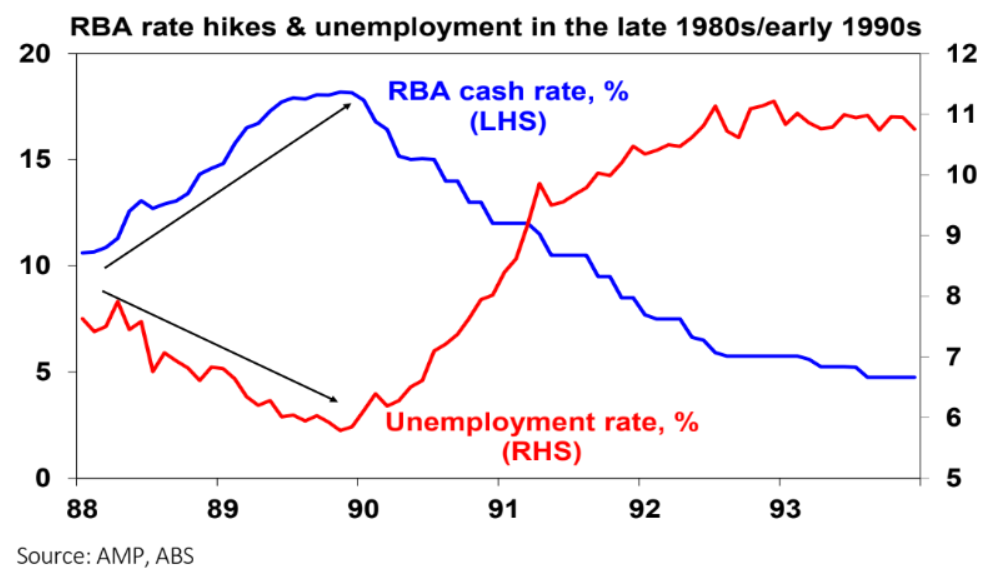

“A lot of this worries me, as I’m old enough to have been in the federal Treasury in the late 1980s, when we kept increasing rates and nothing happened – and then something happened”, Oster said.

“We are forecasting no growth in consumption in the second half of this year, and not even sure you would get in the June quarter”.

Alan Oster makes a pertinent point. As noted recently by AMP chief economist Shane Oliver:

“Despite the RBA progressively hiking rates to 18% over 1988 and 1989 the unemployment rate kept falling prompting many to argue the economy was impervious”.

“But then in late 1989 and early 1990, the lagged impact of rate hikes hit and the economy went into deep recession with the RBA having to rapidly reverse course. It was a classic case of the economy being ok until it’s not!”:

Blind Freddy can see that there is already substantial monetary tightening ‘built in’ owing to the fixed rate mortgage reset.

Therefore, the RBA would be foolish to continue hiking rates.