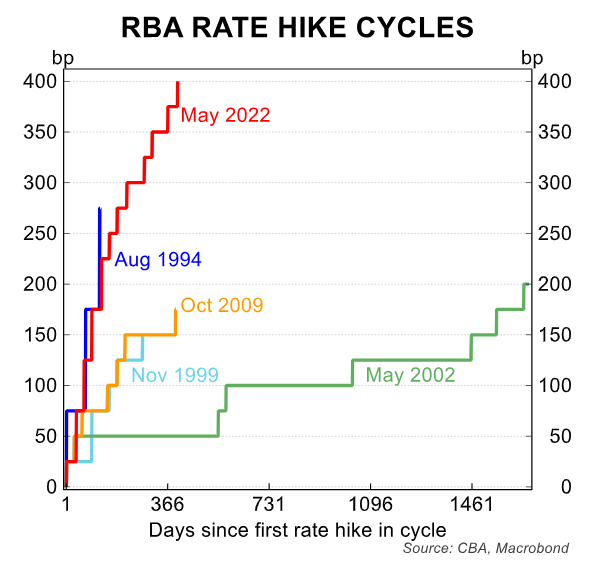

RBA sledgehammer crashes down on economy

AMP chief economist Shane Oliver believes Australia’s economy will slow sharply into 2024 as the lagged effect from the Reserve Bank of Australia’s (RBA) aggressive rate hikes send household consumption crashing.

Oliver notes that “interest rate hikes normally impact with a lag of up to 12 months as its takes time for rate hikes to be passed through to borrowers, for borrowers to cut spending and for companies to cut their workforces”.

Moreover, “this time around, the lag is likely longer thanks to massive pandemic fiscal stimulus which left many households with much higher than normal savings balances, the release of pent-up demand with reopening, 40% of home borrowers at record low fixed mortgage rates (compared to a norm of 15%) and a highly competitive mortgage market that has blunted the flow through of rate hikes”.

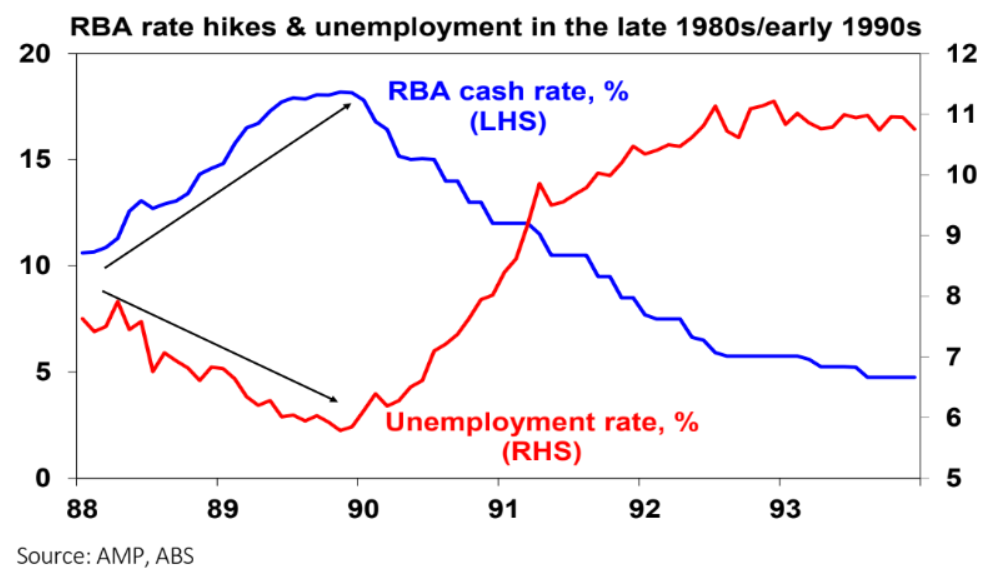

Oliver notes that the interest rate lag was evident in the lead up to the early-1990’s recession.

“Despite the RBA progressively hiking rates to 18% over 1988 and 1989 the unemployment rate kept falling prompting many to argue the economy was impervious”.

“But then in late 1989 and early 1990, the lagged impact of rate hikes hit and the economy went into deep recession with the RBA having to rapidly reverse course. It was a classic case of the economy being ok until it’s not!”:

Oliver warns that the RBA’s monetary tightening is beginning to bite down hard on households and the economy:

“The protection provided households by fixed rates is now ending with borrowers seeing rates reset to levels two or three times what they were and at some point the saving buffers and the reopening boost will have been exhausted”.

“And we are now seeing increasing evidence rate hikes are biting with falling real retail sales, falling building approvals, slowing business investment, slowing GDP growth, more negative corporate commentary, rising insolvencies and indications of a slowing jobs market”.

AMP has already revised down its growth forecast for this financial year to just 0.7%, implying a fall in per capita GDP of around -1.3%.

Oliver also places the risk of an outright technical recession late this year at 50% “as a result of ongoing rate hikes”:

“Consumer spending is almost certain to start going backwards later this year as the 4% plus cash rate will push debt servicing costs into record territory as a share of household income and on the RBA’s analysis 15% of households with a variable rate mortgage (about 1 million people) will be cash flow negative by year end at a 3.75% cash rate and we are now well beyond this”.

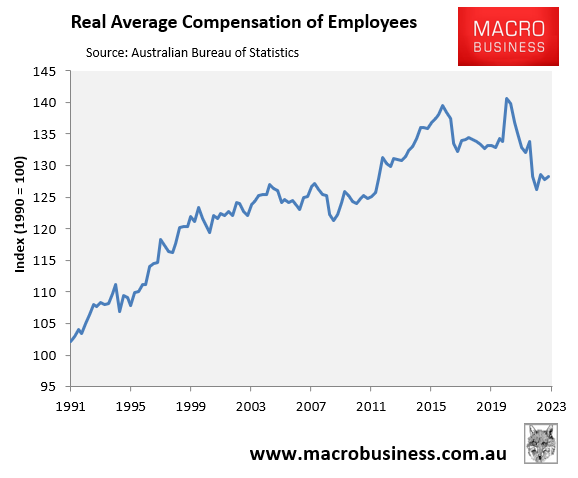

It is difficult to fault Shane Oliver’s reasoning.

With real incomes falling precipitously (see chart below), the prognosis for discretionary retail sales and overall consumption spending remains bleak:

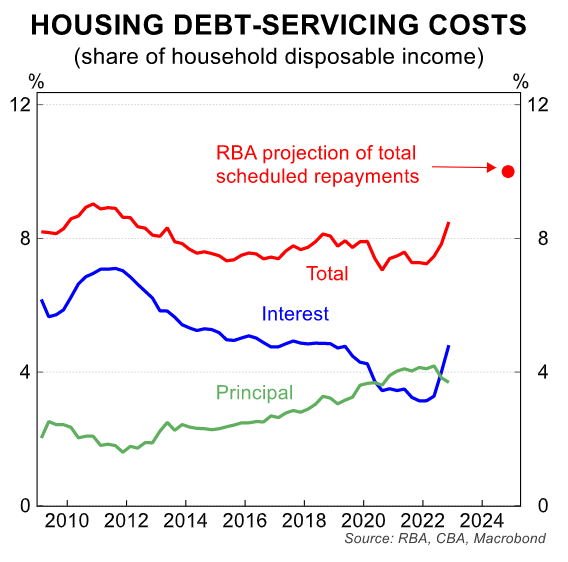

Furthermore, with the RBA still likely to raise interest rates and a huge number of fixed-rate mortgages resetting to higher variable rates, Australian homeowners will soon be spending a record proportion of their income on mortgage repayments:

The only thing preventing Australia from entering a ‘technical recession’ is the Albanese Government’s unprecedented immigration deluge.

‘Quantitative peopling’ has once again ‘saved’ the Australian economy, at least in aggregate terms.

However, everyone’s share of the economic pie is falling, while Australia’s predicted 917,000 population increase over the next two years will destroy living standards by crush-loading everything in sight.