Independent economist Tony Alexander has written a note explaining why New Zealand housing affordability will never strongly improve, which applies equally to Australia.

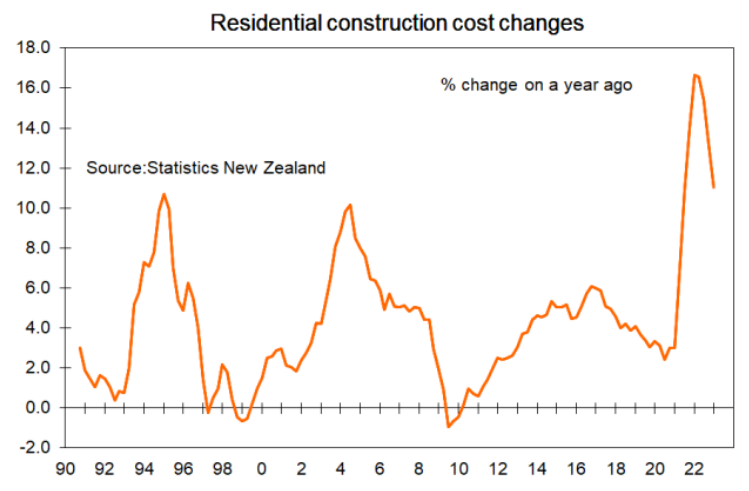

Basically, higher construction costs have been locked in by the pandemic. Building standards are increasing. New builds have more features than historically. Land supply is scarce and costs are inflated. And the population is growing quickly.

These factors point to house prices remaining on a permanently high plateau against incomes.

Will housing affordability ever strongly improve in New Zealand?

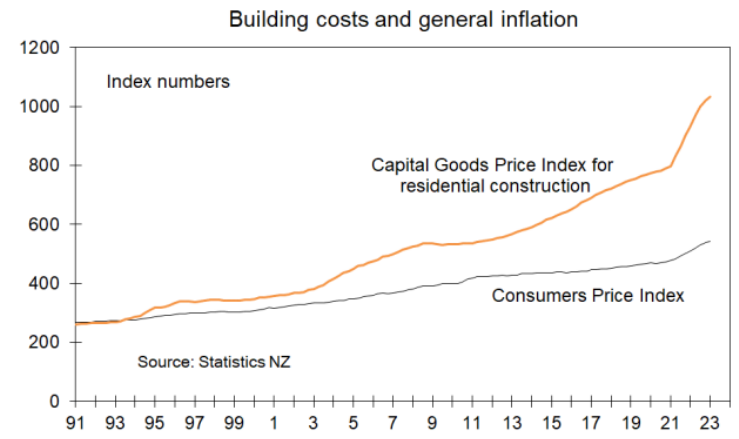

No. Construction costs have not sat unchanged while prices for existing dwellings have risen on average 7% a year for the past three decades.

Productivity growth in construction is about the worst of all sectors. Plus, the pandemic has created supply chain problems which although easing seem to have locked in higher costs for many construction inputs.

Houses are increasingly being required to meet higher, and therefore costlier, standards for many things. Insulation, earthquake standards, health and safety rules, council inspections, etc.

Councils charge more fees than in the past. People also want their new houses built to higher specs than in earlier decades. They want toilets to be on the inside and that there is more than one for instance.

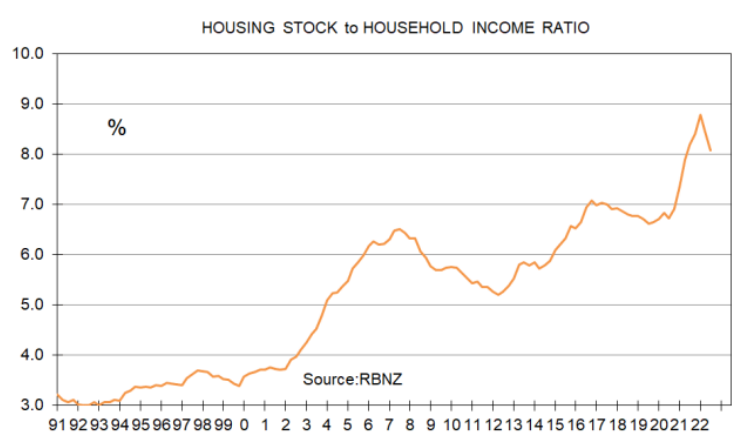

There is a fixed quantity of land available within any given distance from every city’s centre. Our population in 1973 was 3 million. Twenty years later in 1993 it had grown 18% to 3.5 million.

Now, 30 years beyond in 2023 it has grown another 46% to 5.2 million. The average annual growth rate for the past three decades as the ratio of average house prices to income has risen from three to near eight has lifted from 0.8% to 1.3%.

More people, same quantity of land = land prices much higher.

Even opening up swathes of land on the fringes won’t change this dynamic much.

Mortgage interest rates trended down from the early-1990s until two years ago. The ability to service a mortgage of any given size therefore improved and that improvement led to more people looking to buy and prices being bid upward.

Lower financing costs have been baked into higher house prices.

There are other reasons. But they add up to the ratio of house prices to incomes permanently shifting upward.

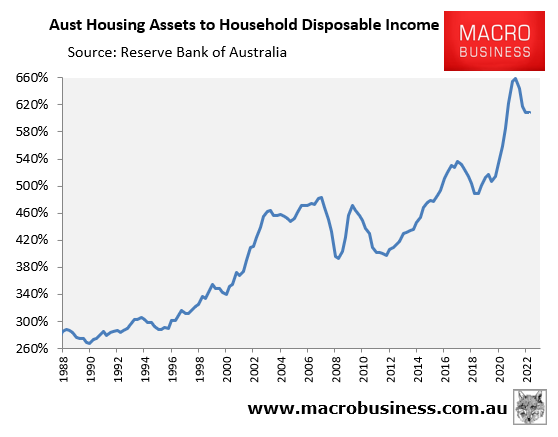

Australia’s housing stock to income ratio has increased in a similar manner to New Zealand’s; although homes are cheaper on average this side of the pond: