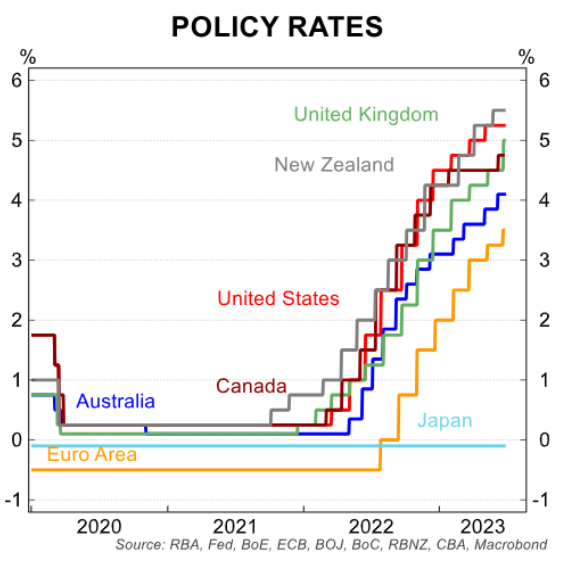

The Reserve Bank of New Zealand has lifted the official cash rate by 5.25% since August 2021, beating most other central banks:

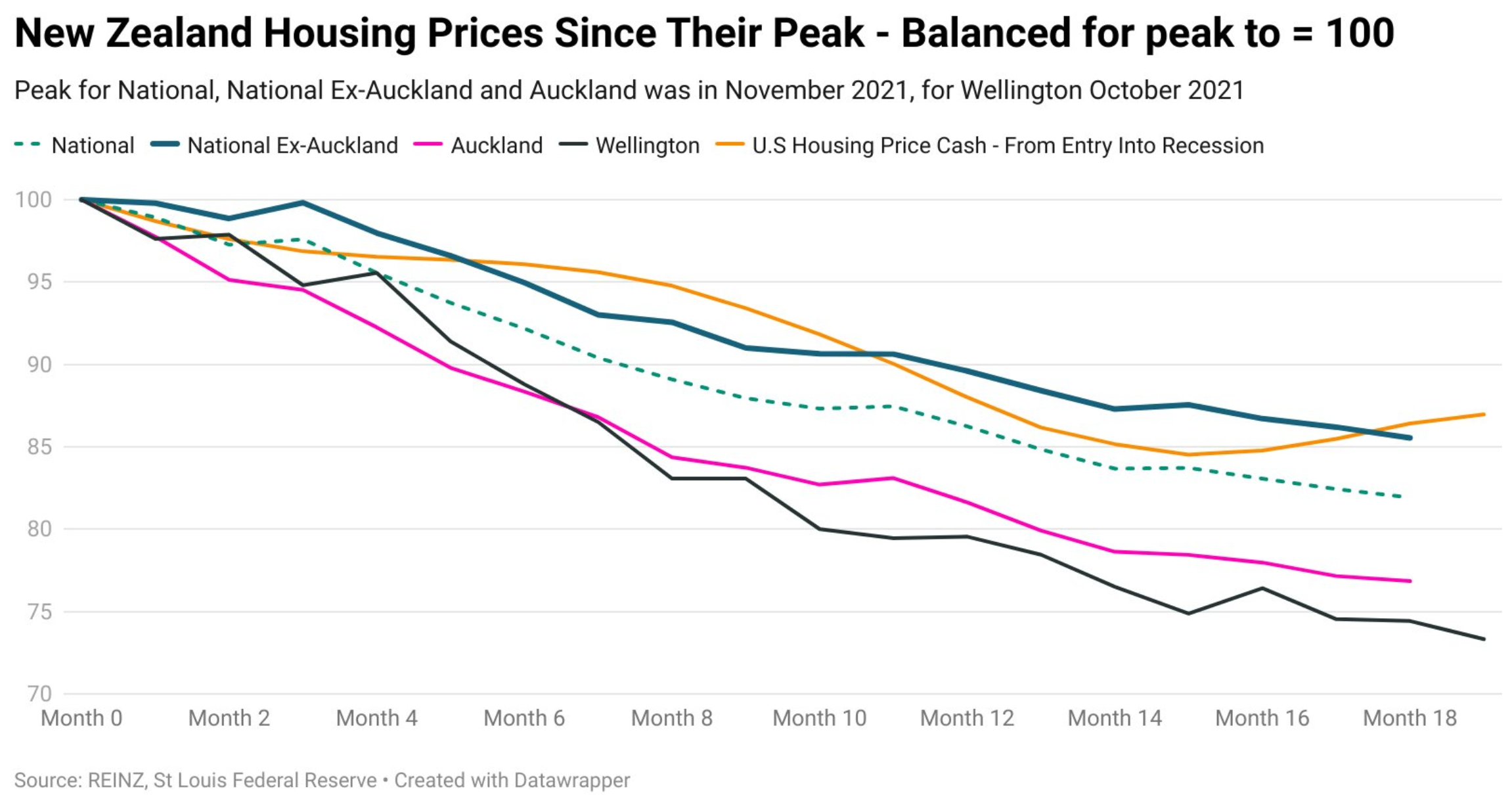

This aggressive monetary tightening has roughly doubled New Zealand mortgage rates, which has sent house prices down 18% nationally and hammered household consumption.

Chart created by Tarric Brooker

The Reserve Bank meets this week to decide whether to hike again. It signalled at its last meeting on 23 May that the official cash rate was likely at its peak.

Since then, a range of data has arrived that supports holding rates at 5.50%.

The March quarter national accounts were released on 15 June. The Reserve Bank had forecasted 0.3% GDP growth, but instead a negative 0.1% print was recorded.

This gave New Zealand two consecutive quarters of ‘negative growth’, thereby placing it into a ‘technical recession’.

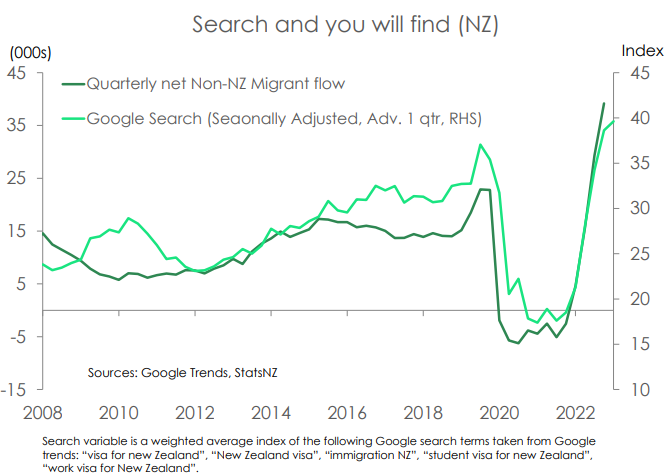

Like Australia, New Zealand is currently experiencing strong net overseas migration and population growth:

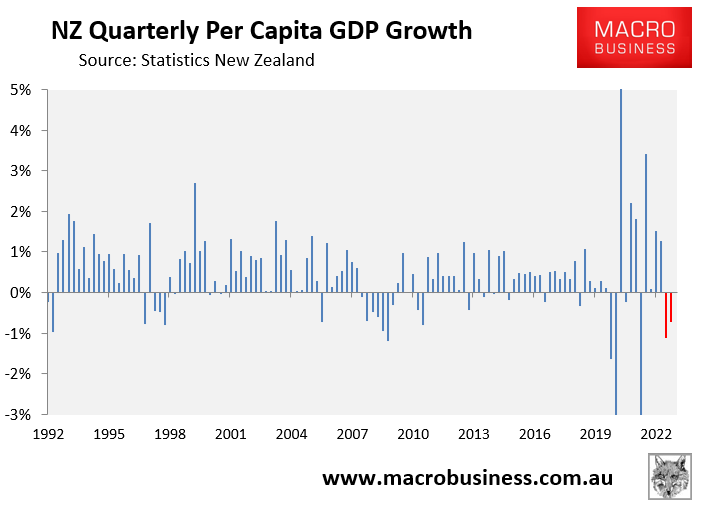

Real GDP in per capita terms has, therefore, plummeted by 1.1% in the December quarter and a further 0.7% over the March quarter (see red bars in chart below):

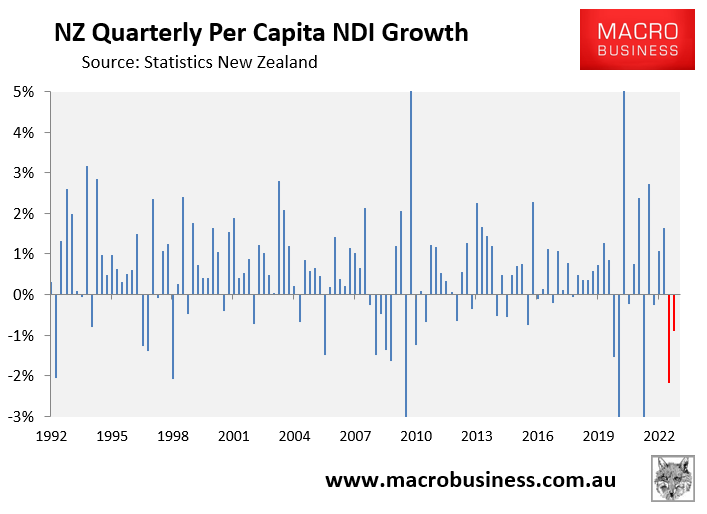

Worse, New Zealand’s per capita real gross national disposable income (NDI) – a better indicator of living standards – collapsed by 2.2% and 0.9% respectively over the December and March quarters:

Other macroeconomic data has also been weak.

Card spending numbers for May were “much weaker than expected”, with a 1.9% seasonally adjusted fall indicating the start of a substantial slowdown.

Then, in the last week or so, we’ve witnessed a sharp increase in the number of non-performing mortgage loans, a NZIER Quarterly Survey of Business Opinion indicating some marked declines in labour market and capacity pressures, credit bureau Centrix’s latest monthly Credit Indicator Report indicating higher consumer arrears and mortgage delinquencies, and the latest Crown Accounts for the 11 months to May 2023 indicating a deteriorating financial position, with tax revenues falling more than $2 billion short of forecasts.

In short, there is more than enough evidence to support the Reserve Bank saying ‘no more’ to official cash rate hikes.

That is, at least until the data changes and turns bullish.

We’ll find out whether the Reserve Bank shares my view on Wednesday at its next monetary policy meeting.