It’s official. The Reserve Bank of New Zealand’s ultra aggressive interest rate hikes, which have lifted the cash rate by 5.25% since August 2021, have driven the economy into a ‘technical recession’.

After New Zealand’s real gross domestic product (GDP) fell by 0.7% over the December quarter of 2022, GDP fell another 0.1% over the March quarter, fulfilling the definition of a technical recession – i.e. two consecutive quarters of negative real GDP growth.

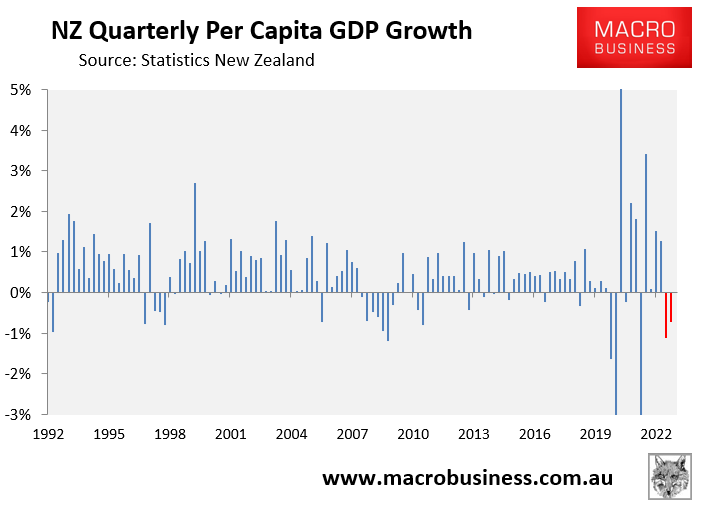

The story is worse with respect to per capita GDP.

With New Zealand’s population growing strongly on the back of historically high net overseas migration:

Real GDP in per capita terms plunged by 1.1% in the December quarter and a further 0.7% over the March quarter (see red bars in the below chart):

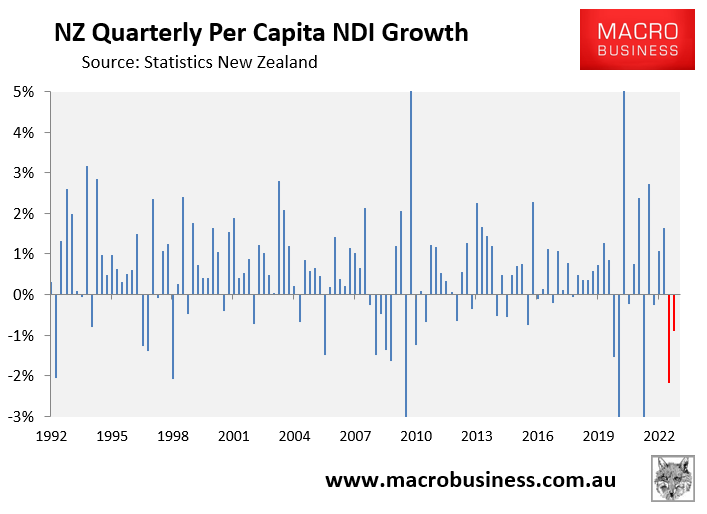

To add further insult to injury, New Zealand’s per capita real gross national disposable income (NDI) also fell by 2.2% and 0.9% respectively over the December and March quarters:

Real gross national disposable income measures the volume of goods and services that New Zealand residents have command over. That is, the real purchasing power of the country’s disposable income.

Therefore, it is a better measure of welfare than GDP, which simply measures economic activity.

These results are obviously backward looking as they are only current to 31 March.

Since then, the Reserve Bank has hiked the official cash rate another two times (i.e. a cumulative 0.5%).

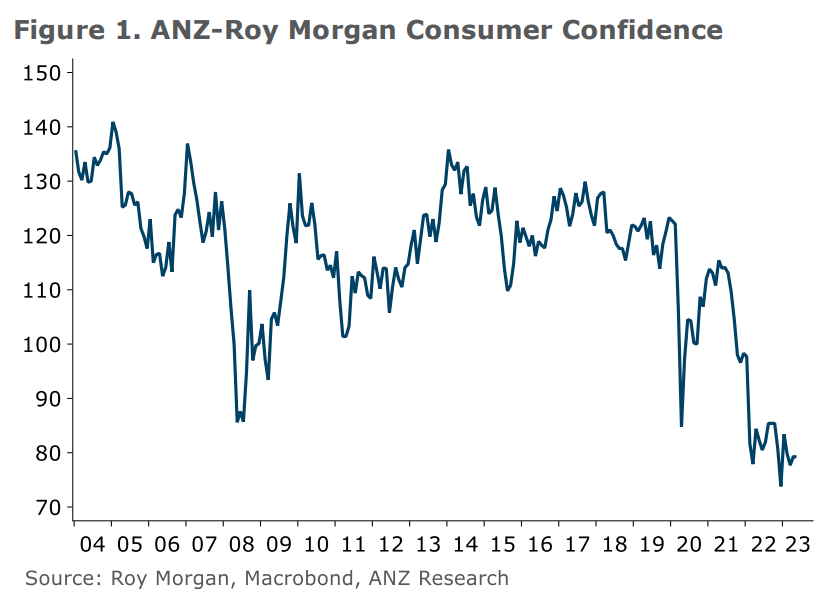

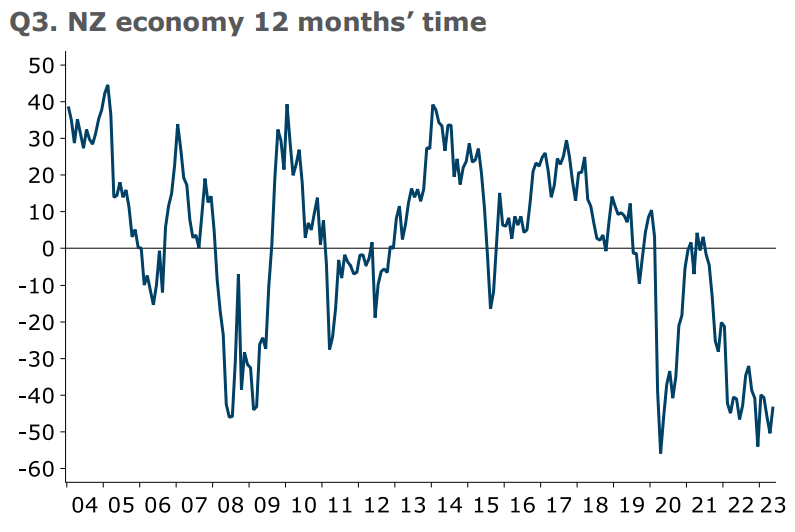

Consumer confidence remained at recessionary levels as at May:

With consumers expecting the economy to remain in the doldrums for the next 12 months:

Capital Economics analyst Abhijit Surya also notes that more recent indicators show household consumption diving in New Zealand.

“It increasingly appears that activity will have weakened further in Q2”, Surya noted.

“According to StatNZ’s monthly activity index, output growth slowed from 1.3% y/y in March to 0.7% in April”.

“Meanwhile, more timely data show that electronic card transactions fell by a sharp 2% m/m in May, which suggests private consumption is in fact on shaky ground”.

The Reserve Bank has already succeeded in delivering a mild technical recession, but a severe per capita recession.

Moreover, the economy is likely to get worse before it gets better.