As expected, the Reserve Bank of New Zealand held the official cash rate (OCR) at 5.50%.

In its commentary on the decision, governor Adrian Orr noted the marked slowdown in the economy as evidenced by a range of macroeconomic data:

“Recent data suggest that tight monetary conditions are constraining domestic spending as expected”.

“Residential building activity has started to ease and falling consent numbers suggest it will continue to slow”.

“Economic activity contracted slightly in the March 2023 quarter. Recent indicators suggest that growth is likely to remain weak in the near term, despite some support from repair and rebuild work underway in regions of the North Island due to severe weather events”.

“Broader government spending is anticipated to decline in inflation-adjusted terms and in proportion to GDP”.

The Monetary Policy Committee also flagged that rates would remain on hold at the current “restrictive level” for an extended period “to ensure consumer price inflation returns to the 1 to 3% target range while supporting maximum sustainable employment”.

The Reserve Bank has made the right decision here.

New Zealand’s economy entered a “technical recession” on 15 June after Statistics New Zealand reported a 0.1% decline in GDP in the March quarter, which followed the December quarter’s 0.7% fall.

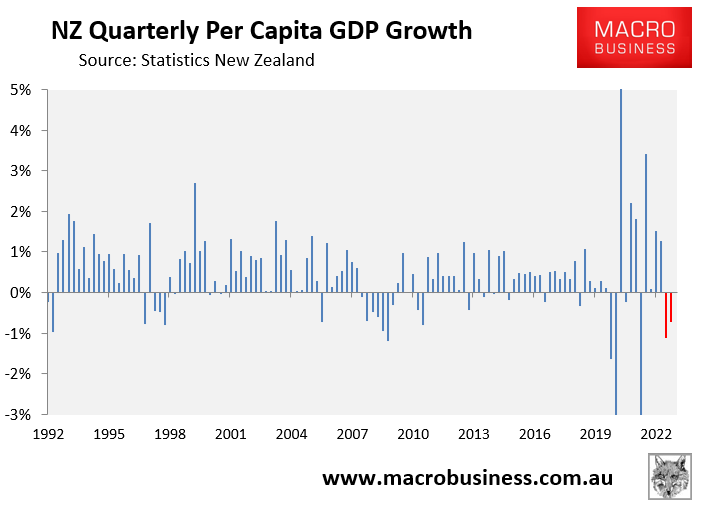

Moreover, because of New Zealand’s strong population growth, real GDP in per capita terms plummeted by 1.1% in the December quarter and a further 0.7% over the March quarter (see red bars in chart below):

Other macroeconomic data has also been soft.

Card spending was “much weaker than expected” in May, with a 1.9% seasonally adjusted fall marking the beginnings of a significant contraction.

In the last few weeks, we’ve seen a sharp increase in the number of non-performing mortgage loans, a NZIER Quarterly Survey of Business Opinion indicating some significant declines in labour market and capacity pressures, credit bureau Centrix’s latest monthly Credit Indicator Report indicating higher consumer arrears and mortgage delinquencies, and the latest Crown Accounts for the 11 months to May 2023 indicating a deteriorating financial position, with tax revenues falling more than $2 billion short of forecasts.

In short, the Reserve Bank’s tightening cycle looks done.