On Monday I explained why the Reserve Bank of New Zealand is likely to hold the official cash rate (OCR) at 5.50% at its upcoming monetary policy meeting on Wednesday.

In a nutshell, the data flow since the last monetary policy meeting on 23 May has been negative, with the economy sliding into a technical recession (and falling heavily in per capita terms), house prices continuing to fall, and a range of household data all coming in soft.

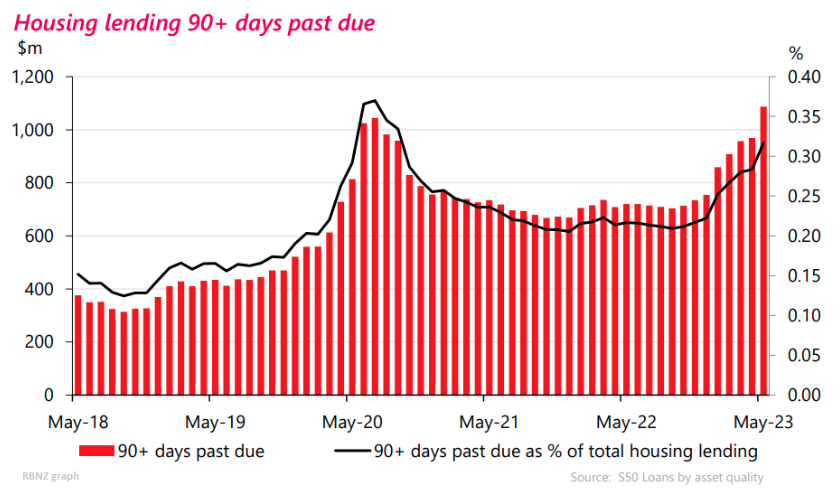

The latest Reserve Bank figures showed that non-performing home loans surged nearly 12% in May, climbing to levels last seen around eight years ago:

In its biannual Financial Stability Report released at the beginning of May 2023, the Reserve Bank said that debt servicing costs “have risen significantly from historically low levels during the pandemic”.

“For a household with a mortgage, the share of disposable income required to service the interest component of their mortgage debt will more than double from its recent low of 9% to around 22% by the end of this year”, it said.

“This increased debt servicing burden is distributed highly unevenly, with some borrowers, such as those who fixed at the low of mortgage rates in mid-2021, seeing far greater rises in their debt servicing costs than others”.

The Reserve Bank also warned that “for households that borrowed during the period of very low interest rates between late 2020 and late 2021, current interest rates exceed some of the test rates used by banks during this period”.

“Therefore, some of these borrowers and other borrowers with high debt-to-income levels may begin to struggle to meet their repayment obligations as they reprice onto the higher rates”.

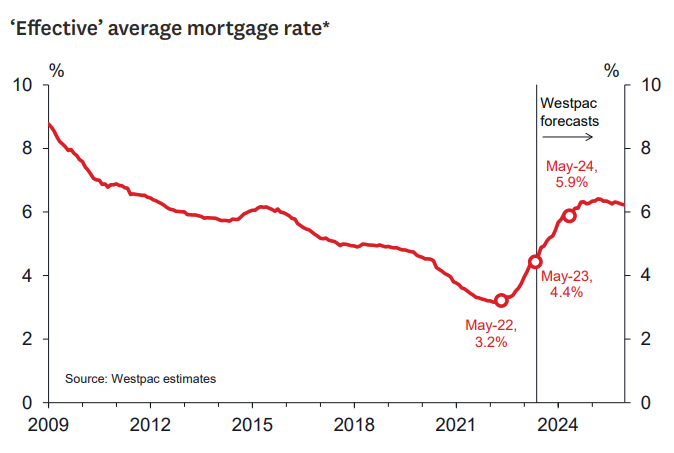

This week, Westpac released data showing how the average mortgage rate paid by New Zealand households will rise by more over the coming year than it has so far due to the expiry of swathes of fixed rate mortgages.

“With 90% of New Zealand mortgages fixed for a period, the pass through of rate hikes has been gradual”, Westpac notes.

“In fact, accounting for the extent of mortgage rate fixing, we estimate that the average mortgage rate households are actually paying has only risen by around 120 bps to date (as a comparison, the OCR has risen by 525bps since late 2021)”.

“Over the coming year around 50% of all mortgages will come up for repricing and will expose increasing numbers of borrowers to higher rates”.

“As a result, the average mortgage rate that households are paying is set to rise by a further 150 bps”.

The next chart from Westpac tells the tale, with the average mortgage rate for households set to rise from 4.4% currently to 5.9% over the coming year:

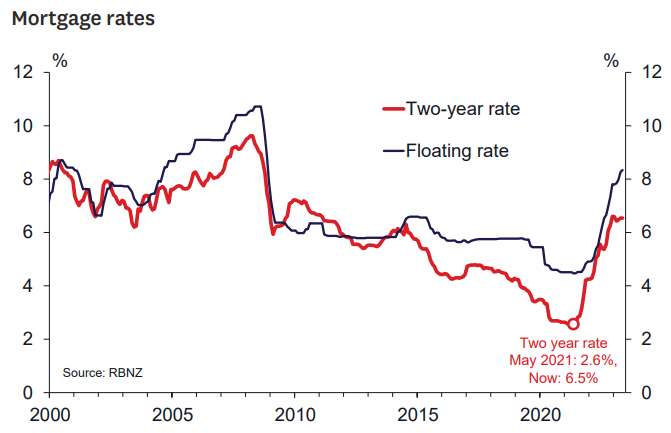

The impact is expected to be brutal, according to Westpac, amid “the great re-fixing”.

“Over the past year, increasing numbers of borrowers have rolled off the very low fixed mortgage rates that were on offer in the early stages of the pandemic, and on to much higher interest rates”, Westpac notes.

“For instance, borrowers who fixed their mortgage for two years back in May 2021 might have secured a rate of around 2.6%. But when those same borrowers go to refix now, they’ll be looking at a rate of over 6%”.

“To put that in context, if you purchased an average priced home in most parts of the country with an 80% mortgage two years ago, the rise in interest rates could add around $900 to your monthly mortgage payments”.

“In Auckland, where house prices tend to be higher, that rise in mortgage interest costs could be closer to $1600 per month”.

In short, the Reserve Bank would be crazy to hike the OCR further.

It is already facing a wave of housing defaults as the average mortgage rate paid by New Zealand households finally catches up with the 5.25% of OCR hikes delivered since August 2021.