Prices for rebar and iron ore futures broke yesterday:

The newsflow may appear promising but it is not:

“China will extend policies to support cash-strapped developers and shore up the ailing real estate sector, including allowing the postponement of loan repayments by a year”.

“Financial institutions will be encouraged to negotiate with real estate firms to extend outstanding loans in order to ensure the delivery of homes under construction, according to a joint statement from the People’s Bank of China and National Financial Regulatory Administration”.

“Some outstanding loans including trust loans due before 2024 will be given a one-year repayment extension, it said”.

Either Beijing does not want to fix property or it does know how because this won’t do it.

This policy was needed two years ago when the market still had a pulse. Now, it will do nothing to lift animal spirits because it does nothing to cure the two structural ills:

- Failing demographics have overhauled Chinese property fervour as the young can’t afford to breed and the old know the cities are built out.

- The policy risk of Xi Jinping’s mood swings is an insurmountable barrier to recovery.

- The first two add a third: a balance sheet shakeout in which the marginal real estate buyer is underwater and must deleverage.

It was a relentless twenty-year Chinese bull market in property construction but it is over and now we will see a relentless 20-year bear market.

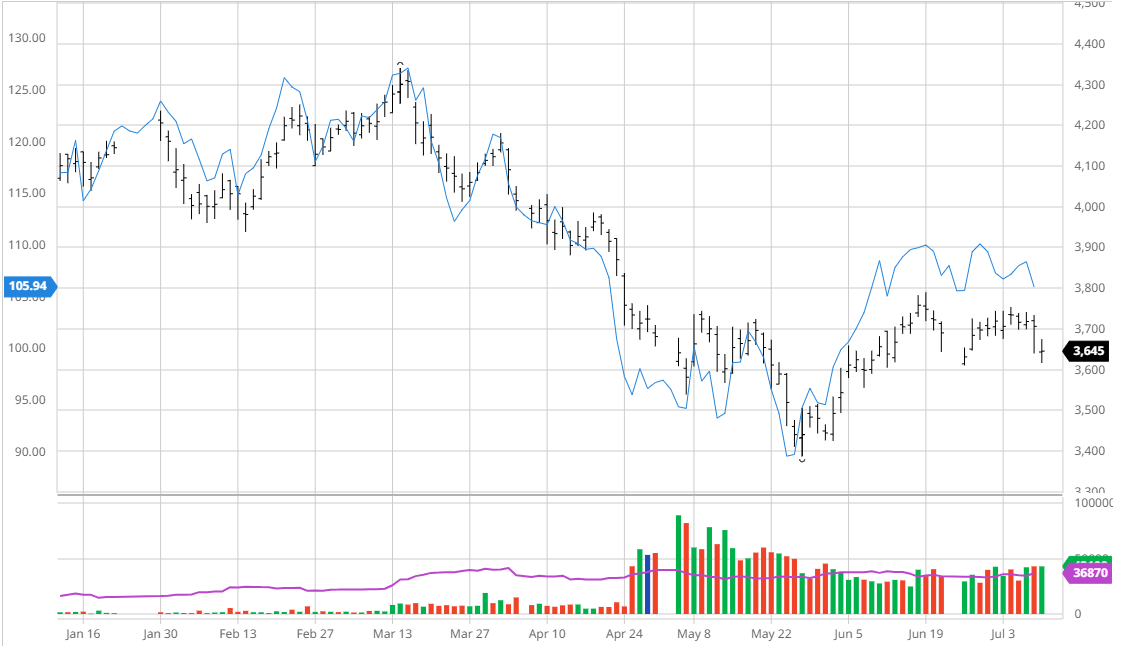

As for steel and iron ore, the signs are beyond bad:

RIO has turned to mining and smoking crack as urbanisation ends but it “feels good”:

There’s a twenty-year bear market ahead for RIO as well.