The incredibly underwhelming Chinese stimulus got the treatment it deserved. A few more voices are recognising the reality. Barclays:

China property–bad, and getting worse

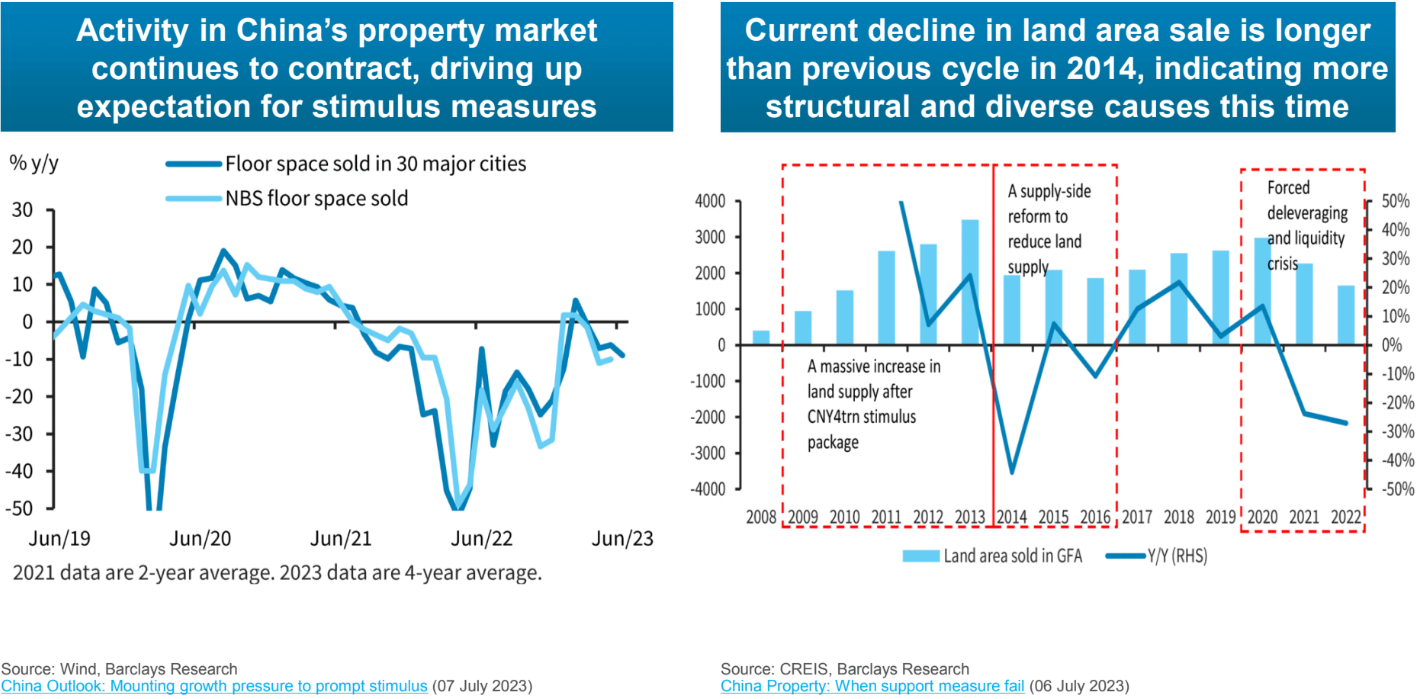

•Record low mortgage rates and low down payments have failed to revive China housing

o The 2% m/m drop in June contracted sales was the first such in at least 12years

o Y/y, contracted sales fell 40% in June, during the traditional peak season for homebuying

•We believe China’s property market faces more problems than in past downturns

o High unsold inventory and developer defaults are weighing on sentiment

o Structural issues are also a drag, including high ownership rates, weak confidence, changed expectations for home prices, etc.

•At this point, policy help is required just to prevent things from getting much worse

o In our base case, we expect contracted sales to decline 25% y/y in the second half

o In our bull case, we expect a fall of 10% y/y in contracted sales in H2

o Our bear case assumes a 35% y/y decline in contracted sales in H2

•China property is going from bad to worse, and the late July Politburo meet will need to announce sizeable support

Weak property sales are only half of the problem. H1 enjoyed a good rise in sales but starts kept crashing anyway.

That’s the second issue. With the development sector cut off from credit, especially dollar bonds, yesteryear’s ponzi-developers can’t leverage into enormous over-building.

Advertisement

Weak sales have delivered an underlying glut of inventory and weak credit means there’s no way for developers to extend and pretend over it.

So, floor area starts are the mechanism of adjustment for the market to clear the glut.

Which is the worst case for iron ore.

Advertisement

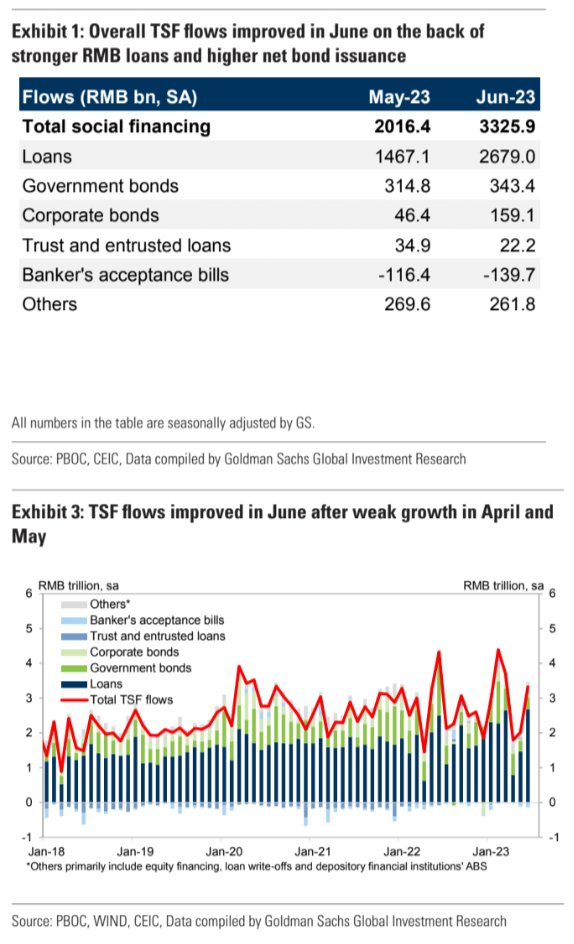

Late yesterday, things improved for a moment with June’s new yuan loans. Goldman:

RMB loan, TSF and M2 data in June all came in above expectations after the disappointing credit data in April and May. RMB loan month-over-month annualized growth was 12.7% in June, higher than 7.8% in May. The composition of loan data suggests broad improvement and stronger credit demand – household loan growth accelerated slightly to 7.7% month-over-month annualized from 7.2% in May, and corporate medium to long term loans grew 20.3% month-over-month annualized in June, vs 14.7% in May. Overall total social financing month-over-month annualized growth was 7.3%, marginally higher than 7.1% in May, mainly on stronger RMBloans. We think stronger policy support likely contributed to the higher loan and credit growth towards quarter-end. PBOC vowed to intensify counter cyclical adjustment and cut policy interest rates in the middle of June. The combination of a large decline in fiscal deposits and higher government bond net issuance also pointed to faster fiscal expenditures in June.

However, this loan mix is not good either. Weak demand and further supply-side industrial expansion is the last thing that China needs and it won’t benefit iron ore much, either.

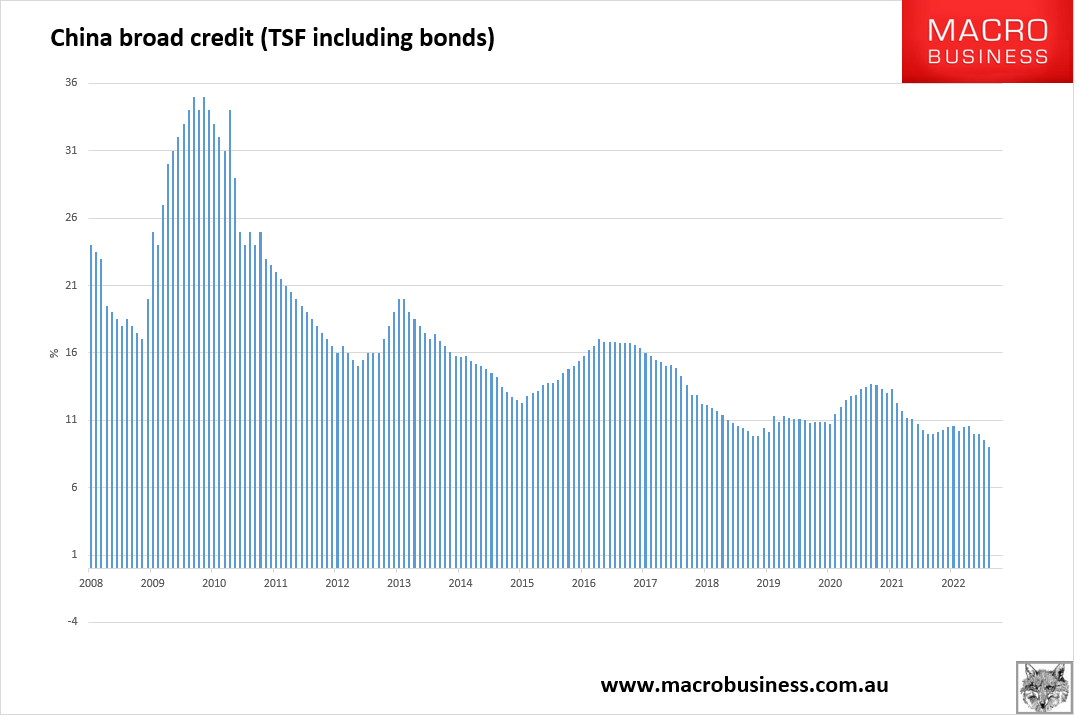

Nor does one better month of credit a summer make. My measure of broad credit stock is now at a record low of 9% year-on-year growth:

Advertisement

For perspective, that is the same rate of credit growth as Australia in October last year.

China is ex-growth, property is going to keep getting worse, and there is nothing anybody can do about it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.