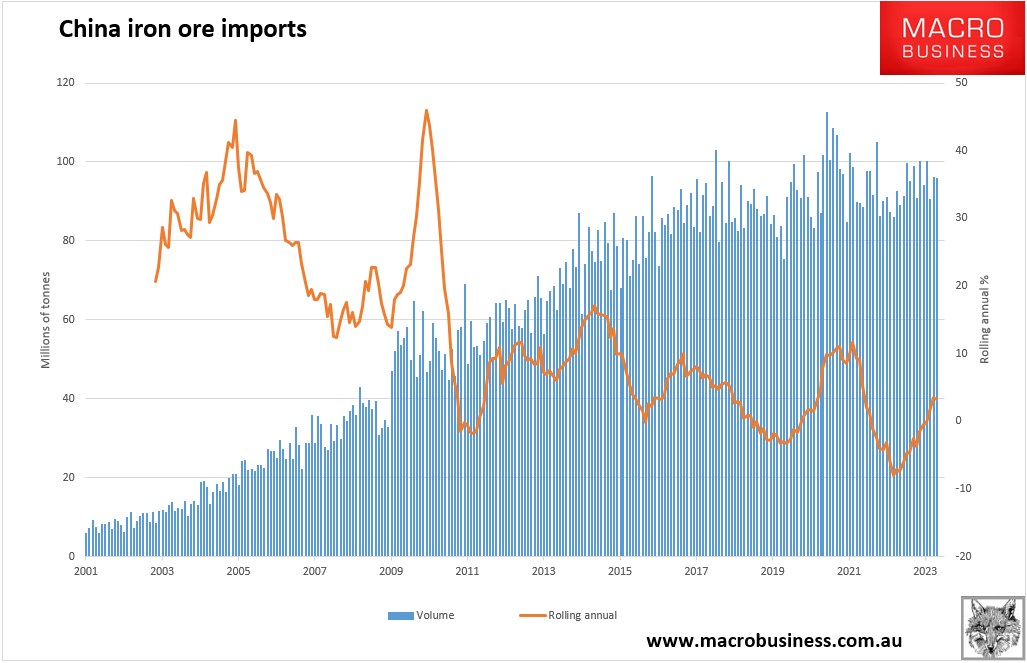

Chinese iron ore imports for June were out yesterday and remain thoroughly topped out with rolling annual growth beginning to fall:

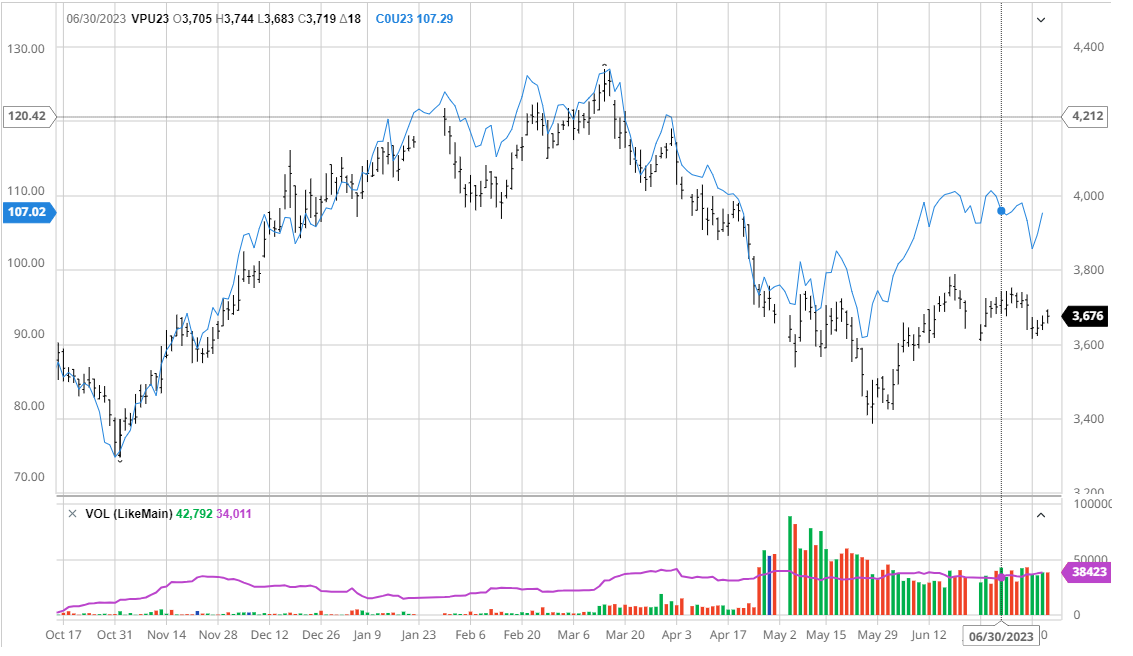

Both steel and iron ore were subdued as other markets went bang!

This is understandable. The options for Chinese stimulus are not bulk commodity positive:

Borrowing More

The government could raise its budget deficit, which was set at 3.88 trillion yuan ($541 billion) in March, excluding the amount of new special bonds regions are allowed to sell this year. Authorities may be wary of doing so given the long-term risks associated with rapidly building up debt, like what happened after 2008.

But short-term fiscal expansion could still help the economy, and moving fast would keep costs relatively low, according to former finance minister Lou Jiwei.

“The budget deficit should be raised in a timely manner to restore the economy to its normal state as soon as possible,” Lou wrote in an article carried Sunday on the front page of the Economic Daily, a newspaper affiliated with the State Council, China’s cabinet.

Broad Budget Deficit

Lou called on the government to raise this year’s fiscal deficit by up to 2 trillion yuan, which would boost the deficit-to-GDP ratio to as high as 4.6%, according to Bloomberg calculations based on official data. Beijing’s target is 3%.

The government is also weighing plans to allow the issuance of additional local bonds to help cash-strapped, high-risk areas pay down their hidden debts, people familiar with the matter told Bloomberg News earlier this month.

Sovereign Bonds

Any new debt should be mostly sold by the central government and used to help small businesses, Lou said. Some of the money could also go to strained local governments to stop them from going overboard on measures to find income, such as imposing excessive fines on people, he said.

…In an interview with the government-run China Newsweek, he argued the central bank should cast aside a “dogmatic” insistence about being independent, and start buying central government bonds directly to spur growth.

Rate Cuts

The central bank could also ease any burden the government shoulders from taking on new debt by continuing to cut interest rates to keep financing costs low. Injecting more liquidity into the banking system would also help absorb the issuance of debt.

Reserve Ratio

Far more likely than a massive policy rate cut: Additional trims to the reserve requirement ratio, or the amount of cash banks must keep in reserve.

At the end of June, the PBOC also increased the quota for relending and rediscounting programs that support the agricultural sector along with small and private firms. The central bank may be looking at more ways to funnel bank loans into targeted sectors via structural tools, according to the Shanghai Securities News.

Tax Incentives

Former Premier Li Keqiang oversaw the rollout of tax cuts to help companies weather the impact of the US-China trade war and the pandemic. Those measures were massive in scope: Tax income last year was nearly 14% of GDP, compared to 17% in 2018.

Cash Subsidies

Luo also suggested the government provide consumption coupons or cash subsidies to encourage household spending. Costs could be shared between the central government and local ones, with poor regions responsible for a lighter burden, he wrote in the China Finance article.

Nothing there helps bulk commodity demand much. There isn’t much that can be done now that China catch-up property growth period is over.

I expect we will see rate cuts (as the Fed eases off), limited infrastructure boosts, and various tax incentives on the supply side.

As well as a relentless slide in growth.