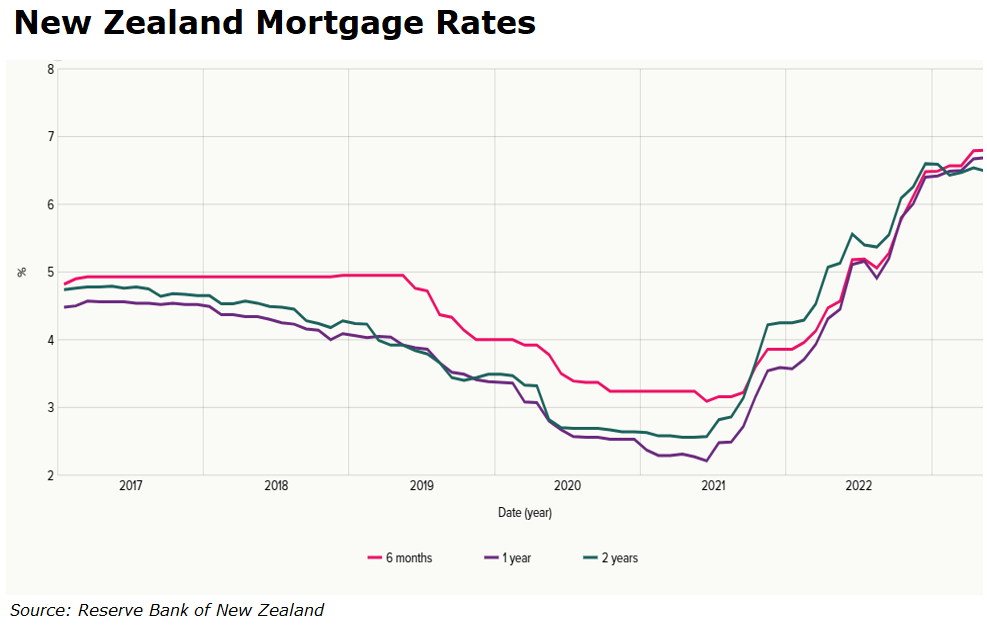

The Reserve Bank of New Zealand has been one of the world’s most aggressive central banks, lifting the official cash rate an extraordinary 5.25% since October 2021.

This aggressive monetary has more than doubled mortgage rates across New Zealand:

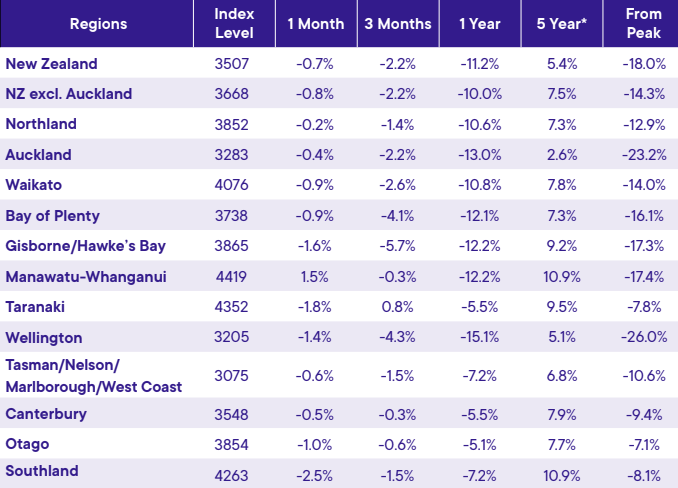

The impact on the nation’s housing market has been brutal, with the Real Estate Institute of New Zealand’s (REINZ) leading house price index (HPI) falling another 0.7% in May, with prices nationally down 18.0% from its November 2021 peak:

The REINZ HPI adjusts for differences in the mix of properties sold each month and is the preferred index of the Reserve Bank.

As shown above, Auckland (-23.2%) and Wellington (-26.0%) has led the nation’s decline, with both markets experiencing genuine house price crashes.

To add further insult to injury, May’s sales were the lowest for the month of May in 12 years (excluding the 2020 lockdown).

May’s sales remained down by around a quarter (-23%) compared to pre-pandemic levels in May 2019.

Therefore, the housing market remains in a deep slump at the start of winter.

Homes are also taking longer to sell, with the median number of days taken to achieve a sale rising to 49 in May, up six days from May last year.

Commenting on the results, REINZ chief executive Jen Baird said that high mortgage rates continues to weigh on the market.

“It’s clear that current high interest rates combined with a tight economy, are still influencing the market as buyers continue to act with caution while economic headwinds play out”.

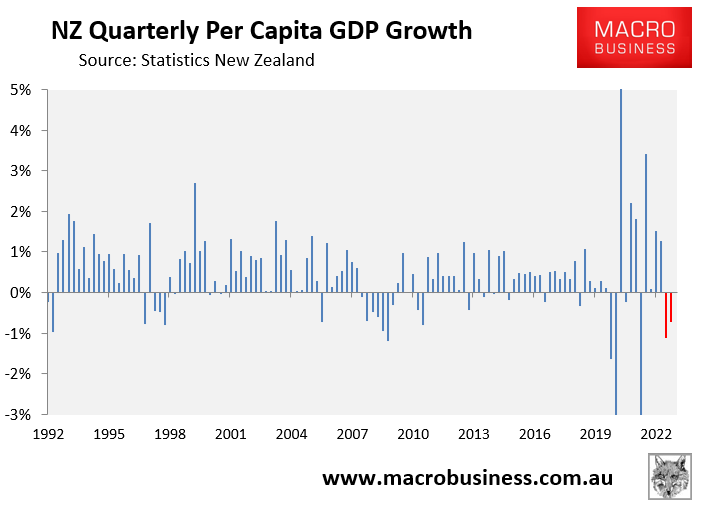

The economy has also fallen into a technical recession, as well as a deep per capita recession (see red bars below):

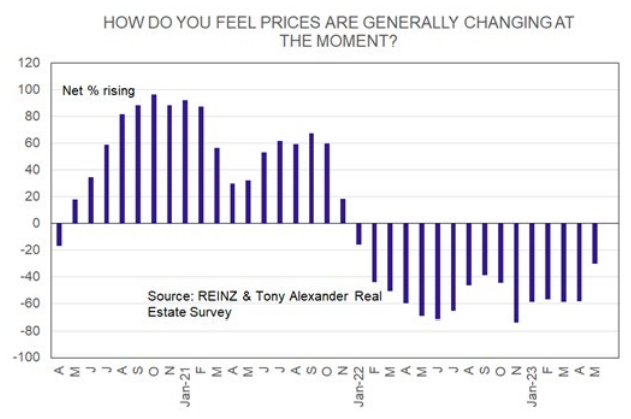

Tony Alexander’s monthly survey of real estate agents also revealed “a net 58% of agents were seeing prices still falling”:

That said, Alexander’s survey did show some green shoots, with “the net proportions of agents seeing more people attending auctions and open homes are at their highest levels in over two years”.

Moreover, “FOOP – the fear of overpaying – has fallen to its lowest level since January 22”, according to the survey.

I expect prices to rebound after the 14 October general election.