TSLombard with the note. China is over. The future is friend-shoring.

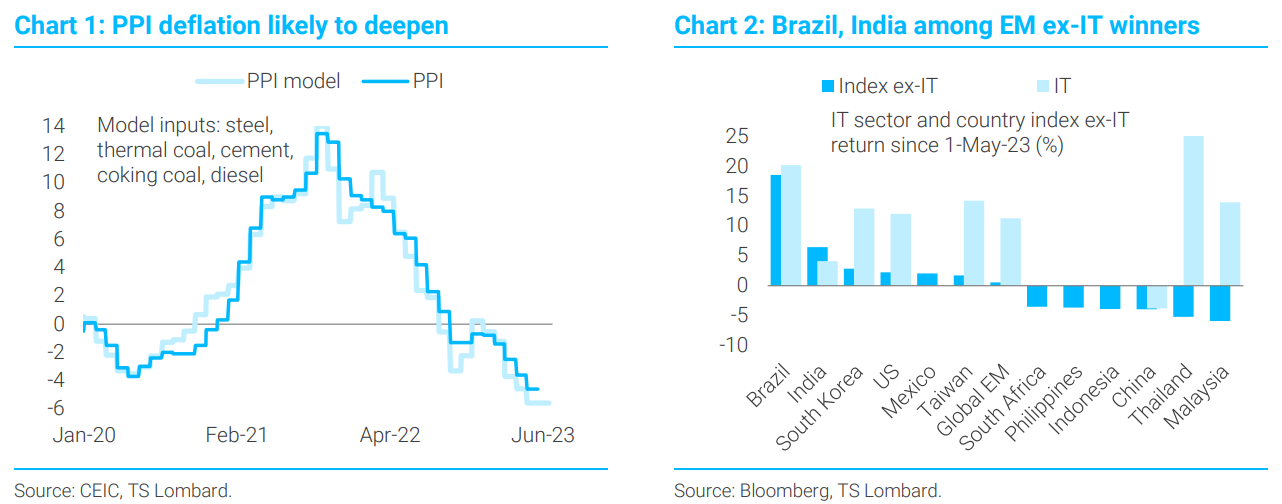

China’s slowdown deepens amid scarring and ideological shift. The economic recovery in China has faltered as weak manufacturing demand, illustrated by deepening PPI deflation, has overwhelmed relatively robust services (see Chart 1). China’s equity market has nonetheless rebounded amid hopes of fiscal and monetary stimulus. We caution, however, that scarring from Covid and the property collapse will reduce the efficacy of any stimulus, while ideological constraints mean that the scale of easing seen in previous slowdowns is much less likely this time around.

There is little chance of meaningful reform in China. The question for investors is what the authorities plan to do about the economic shortfall. In our view, the reforms needed to turn the economy around will immediately run into the political roadblocks the leadership has set up in the name of national security. We expect the equity rebound to quickly run out of steam, while the economic slowdown and deteriorating interest rate differentials will further weigh on the renminbi. Outflows from China will be redeployed to other EM as well as to advanced economies Tech sector momentum boost to EM will eventually slow.

The full text of this article is available to MacroBusiness subscribers