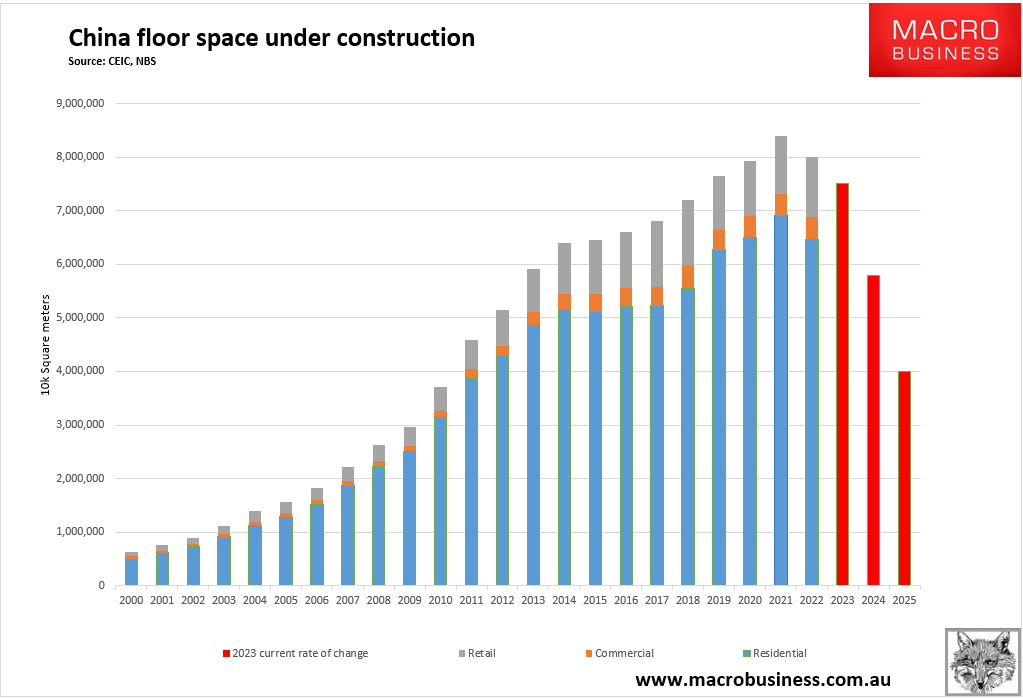

For nearly twenty years, the rise and rise of Chinese property construction was unstoppable. It did matter how much was built. Nor how irrational the dynamics were. It just kept getting bigger.

Now, we have entered the reverse phenomenon. It does not matter how low sales go, there is always less. No matter what anybody does, the falls don’t stop:

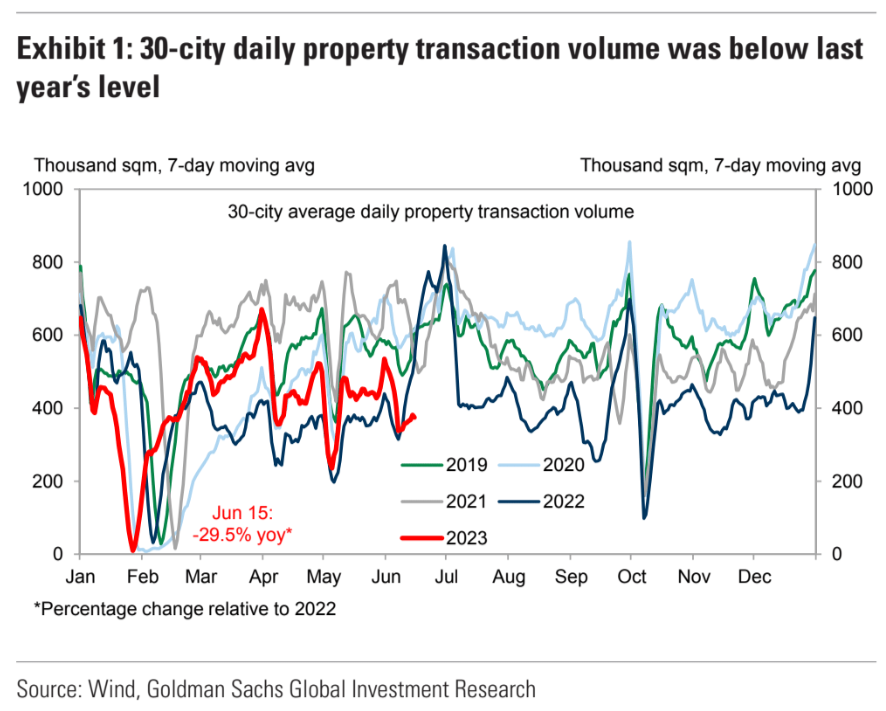

Last week, property sales hit all new lows:

The Dragon Boat Long Weekend sales event is later this year so that explains some of the relative weaknesses, but not all!

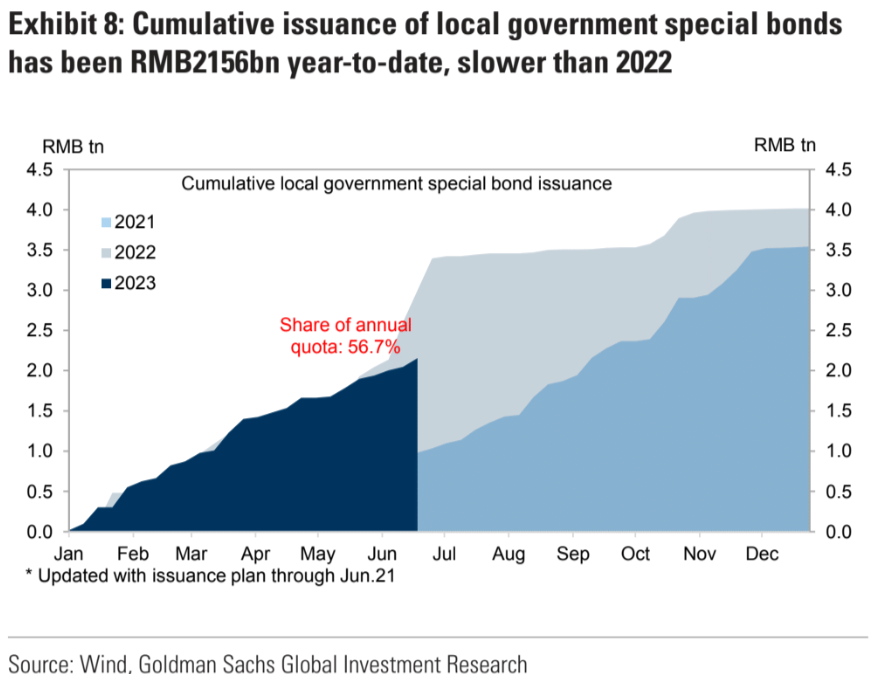

Infrastructure funding is starting to fall heavily year-on-year as well:

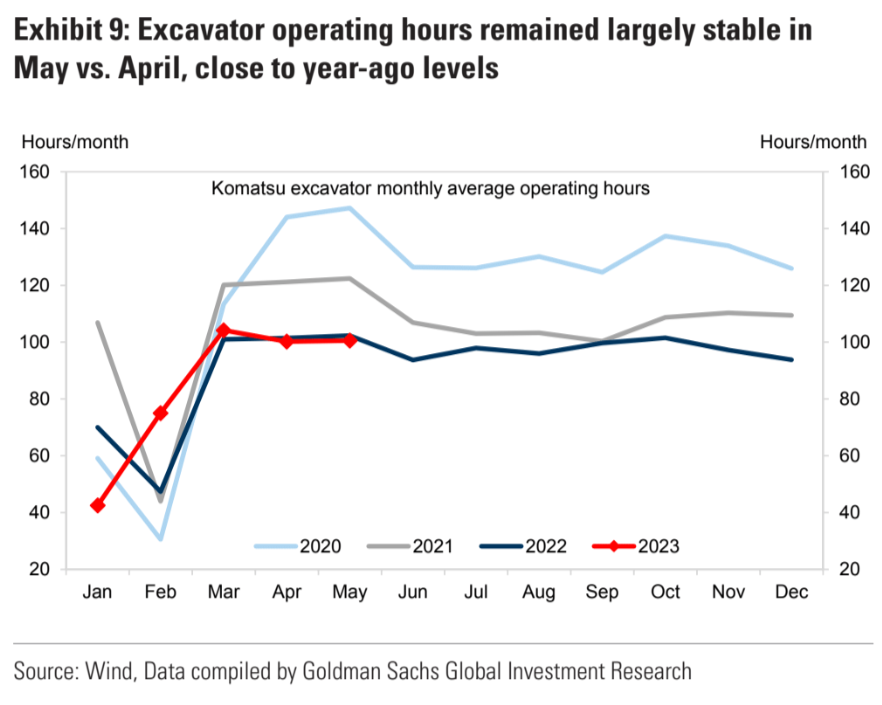

Excavator use is grinding down:

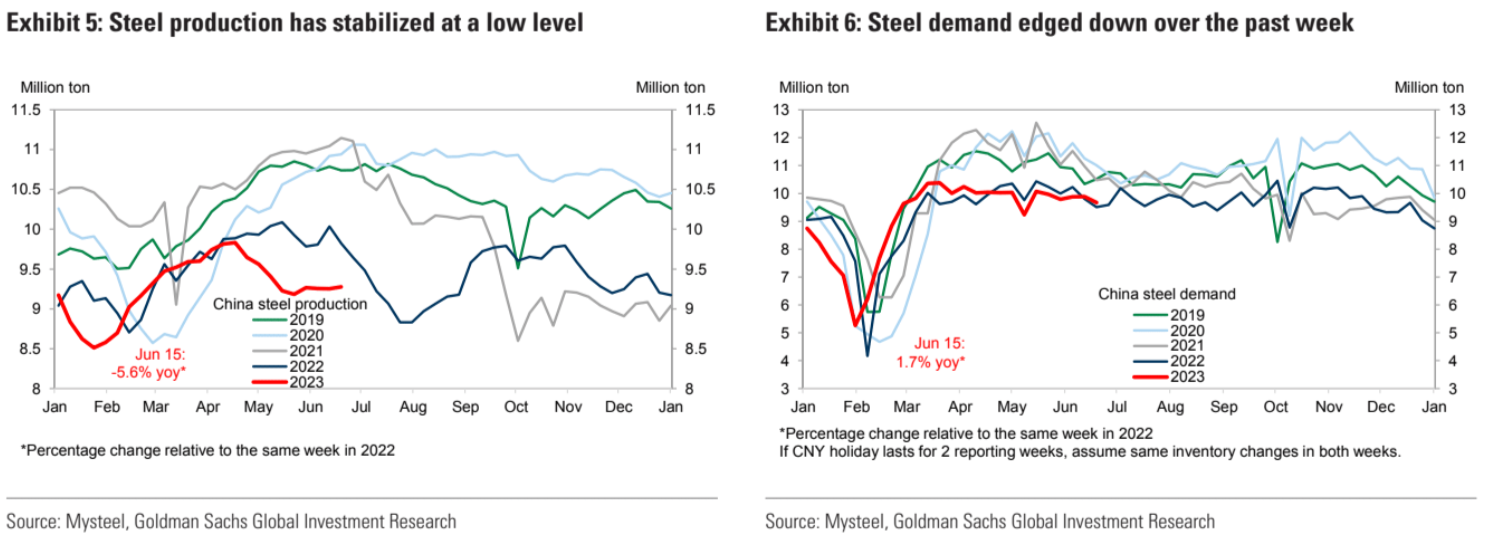

Steel is struggling:

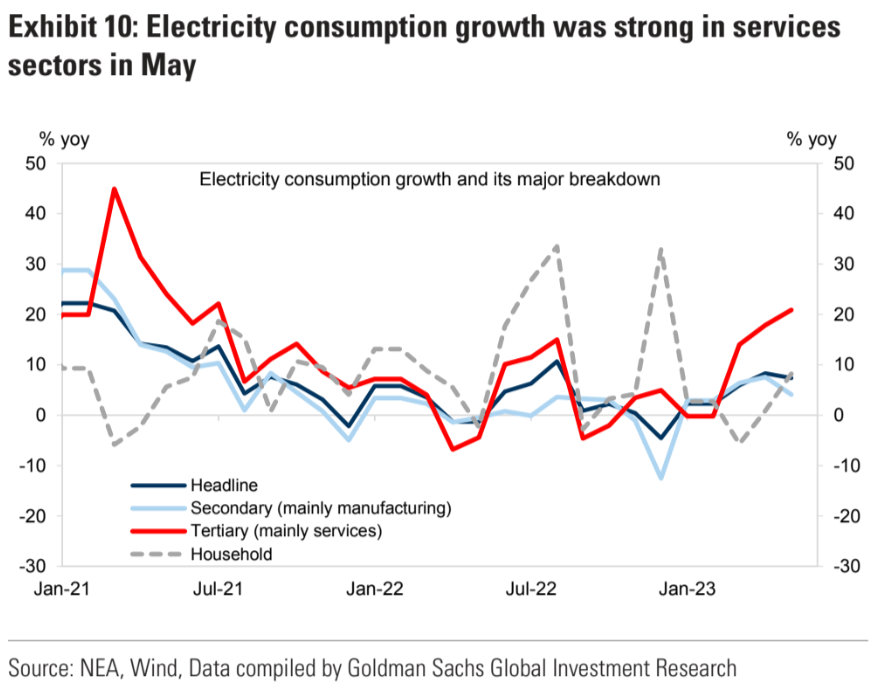

The broader economy is still OK though the weather has been hot so that explains some of the energy spike:

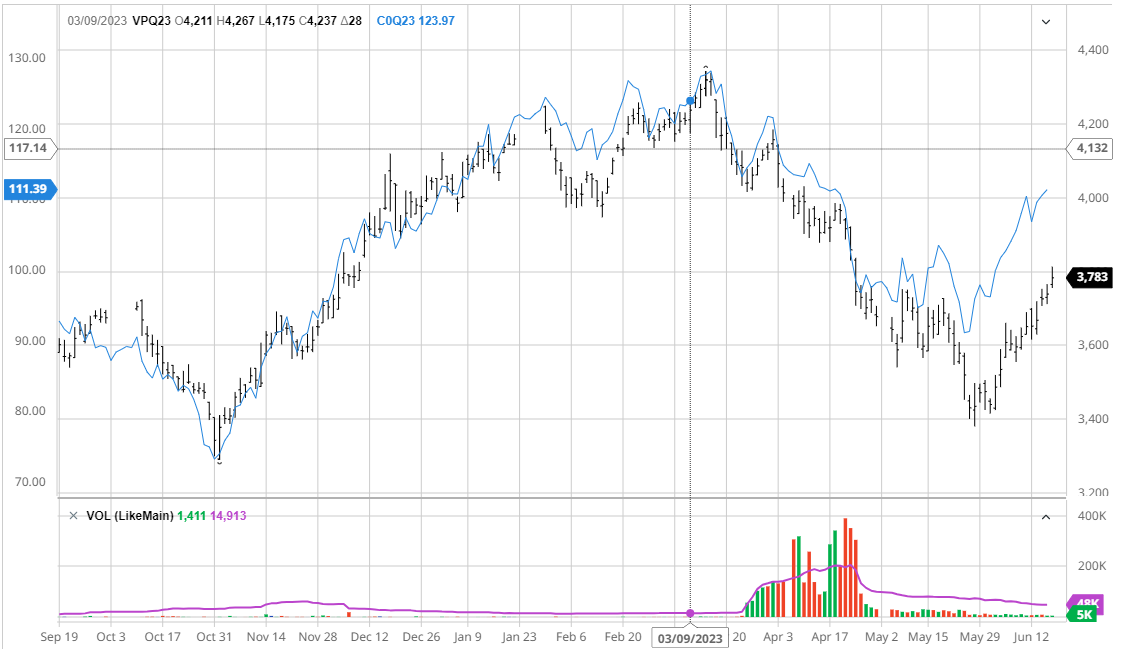

Stimulus speculation continues but the outlines are not encouraging for iron ore. Goldman:

On the back of material slowdown of export growth and weak domestic demand, policymakers shifted to a more supportive stance in recent days to facilitate overall economic growth. We continue to expect further policy easing measures to be announced in the next few weeks. We think “strengthening macro policy

adjustment” implies further monetary policy easing, consistent with our view that more RRR/policy rate cuts are ahead. “Effectively expanding demand” may imply accelerated government investment and infrastructure investment. “Enhancing real

economic development” could refer to support to new energy vehicle demand and other consumption areas. “Reducing key risks” is likely related to containing property and LGFV downside risks.Ahead of today’s State Council meeting, market expectations were increasing regarding China stimulus on the back of a Wall Street Journal article reporting that policymakers have been considering issuing RMB1tn central government specialbond (CGSB) for infrastructure investment. We think this is unlikely because CGSB was rarely used historically and because policymakers can accelerate the RMB1.7tn remaining local government special bond (LGSB) quota to support infrastructure building

in the next few months.In addition, PBOC, Financial regulatory administration bureau, CSRC and MOF jointly released a document to comprehensively promote rural vitalization. In particular, policymakers pledged to increase medium to long term loans to the rural sector through= relending tools and RRR adjustments, to improve financial services to rural residents and also to boost migrant workers’ employment and income

As you can see in the above infrastructure funding chart, all that a new push would do is stop activity from falling year-on-year while property construction keeps on shrinking so it is not bullish for iron ore beyond today’s relief rally:

I remain of the view that unless China gets much more aggressive, iron ore is a sell-the-rips market.

The next seasonal convergence of seasonal trends with weak fundamentals is September and the downside could be a doozy.