The latest lending figures from the Reserve Bank of New Zealand shows that new mortgage borrowers are borrowing far smaller sums relative to their incomes than they did during the pandemic.

Overall, the debt-to-income (DTI) ratios of new borrowers in March 2023 were the lowest since the Reserve Bank began recording this data in 2017.

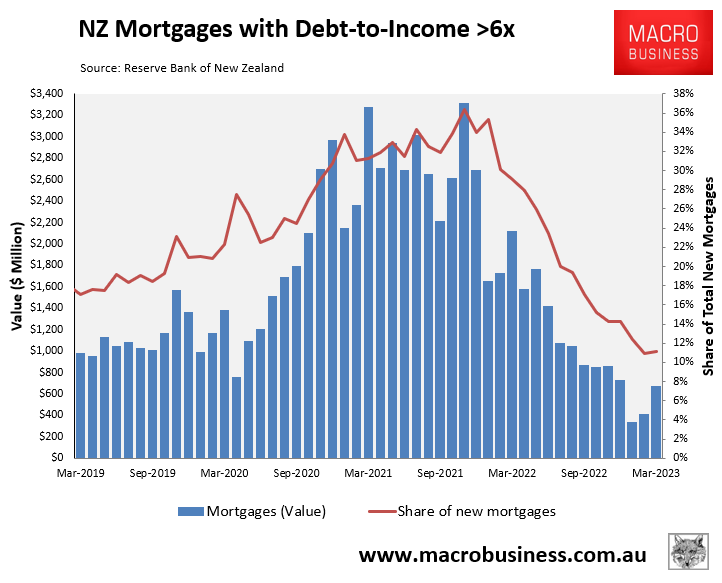

As illustrated in the next chart, only 11% of new mortgage originated in March 2023 were at DTI ratios of six or above.

That’s down more than two-thirds from the 36% of mortgages taken out at those same high DTIs in November 2021 at the peak of the market:

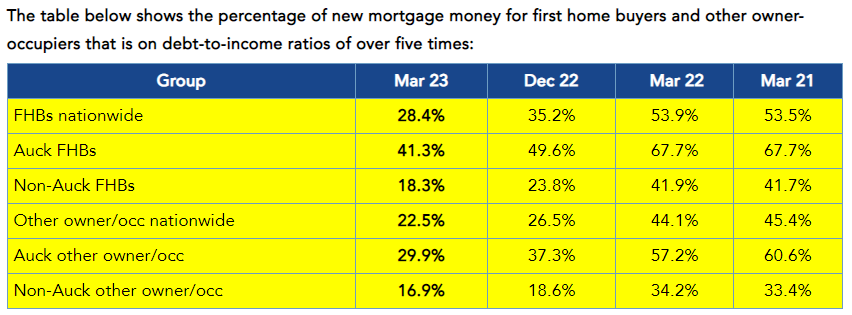

The below table from Interest.co.nz also shows the sharp fall in DTI ratios over five times across owner-occupiers:

A variety of factors have likely driven the sharp decline in DTI ratios.

The Reserve Bank has lifted official interest rates by 5.0% since late 2021.

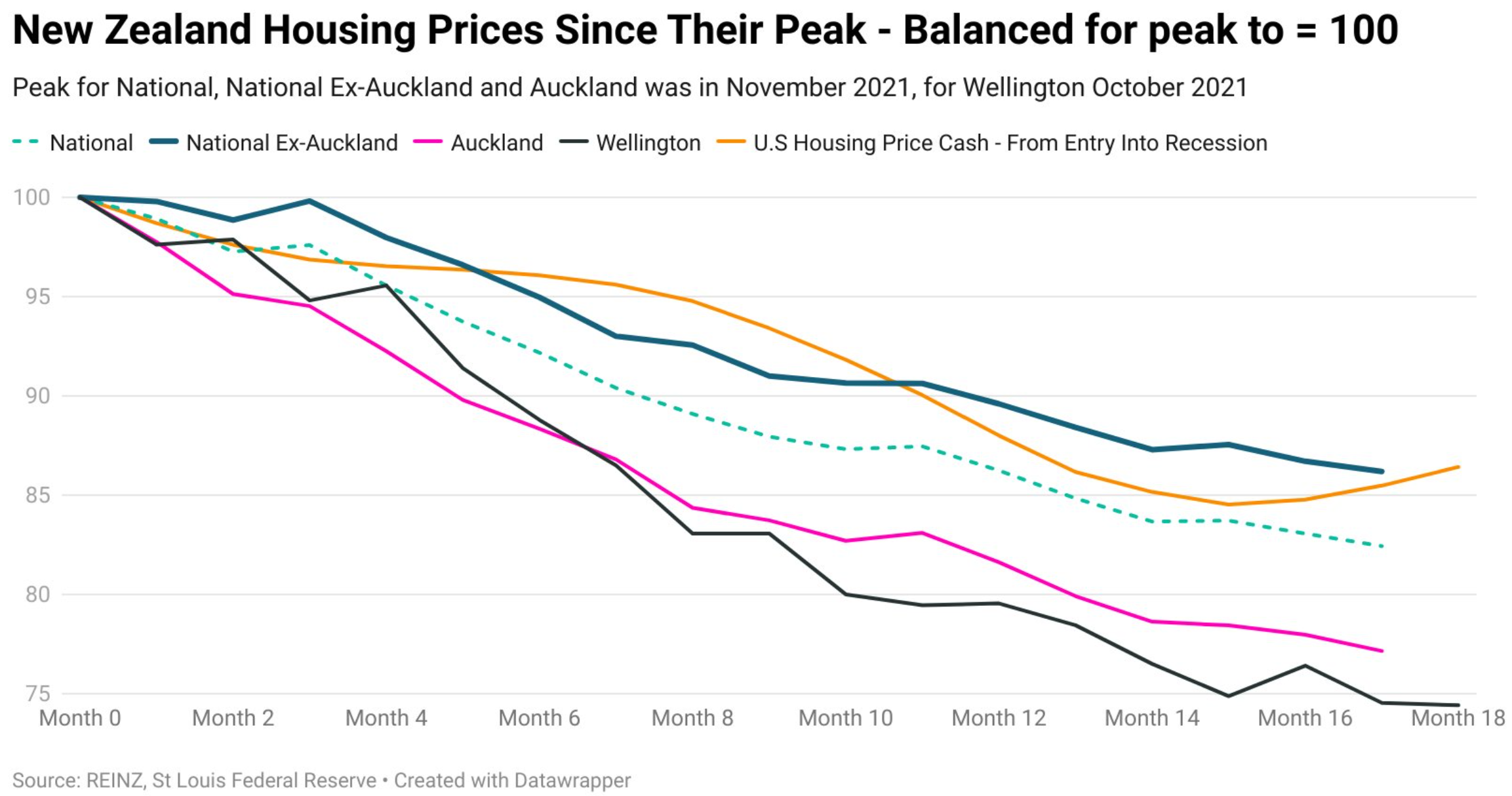

In turn, house prices have collapsed by around 17.5% across New Zealand, thereby requiring less money to be borrowed:

Household incomes have also risen in nominal terms.

Finally, the dramatic rise in mortgage rates, along with banks’ more conservative lending rules, has meant that would-be homeowners can no longer borrow at the previously seen high DTI ratios.

This sharp reduction in DTIs helps to explain why the Reserve Bank is seeking to ease mortgage loan-to-value ratio (LVR) restrictions from 1 July 2023.

Personally, I would like to see the Reserve Bank introduce hard DTI limits to prevent the housing bubble from reflating when the Reserve Bank eventually starts easing rates.