National Australia Bank’s chief economist, Alan Oster, says the near-term balance of risks with regard to inflation remains on the upside.

Oster notes that the Reserve Bank of Australia (RBA) does not expect inflation to return to the top end of its target range of 2-3% until mid-2025.

The trimmed mean – the RBA’s preferred measure of inflation – was still well above the target range at 6.6% in the March quarter.

NAB believes that with inflation remaining high, the RBA could potentially trigger two additional 25 basis point increases in the cash rate in the current monetary policy tightening cycle.

This would lift the official cash rate (OCR) to a peak of 4.35%.

In turn, GDP growth would slow to below 1% (-1% in per capita terms) and the unemployment rate would lift to 4.7% next year, which will cause the RBA to slash rates by at least 1%.

“After a sequence of surprises from the RBA in recent months, we are reverting to our baseline expectation from February that the cash rate will rise to a peak of at least 4.1% – which we pencil in for July, though we see some risk the RBA could wait till August”, Oster said in his note.

“The key uncertainty for our rate expectations has been the reaction function of the RBA, and monetary policy strategy of the RBA been marked by some mixed signals in 2023”.

“However, it is clear that the near-term balance of risks on inflation remain to the upside, and the RBA is forecasting inflation to only return to the top of the target band by mid-2025”, Oster said.

“At least one additional rate rise is likely to be necessary to limit the risk this timeline slips any further. We wouldn’t rule out the prospect of an additional rise to 4.35% if the data stays stronger for longer”.

“It remains our view that, as higher rates pass through to household cash flows and the wider economy, the economy will begin to slow more noticeably in the second half of 2023 and into 2024, seeing annual GDP growth slow to below 1% and the unemployment rate begin to rise, reaching around 4.7% in 2024”.

“This makes it an increasingly difficult balancing act for the RBA to manage inflation lower without slowing the economy too much. We continue to expect the cash rate to return to a more neutral setting of 3.1% by mid-2024 as this slowdown takes hold”, Oster concluded.

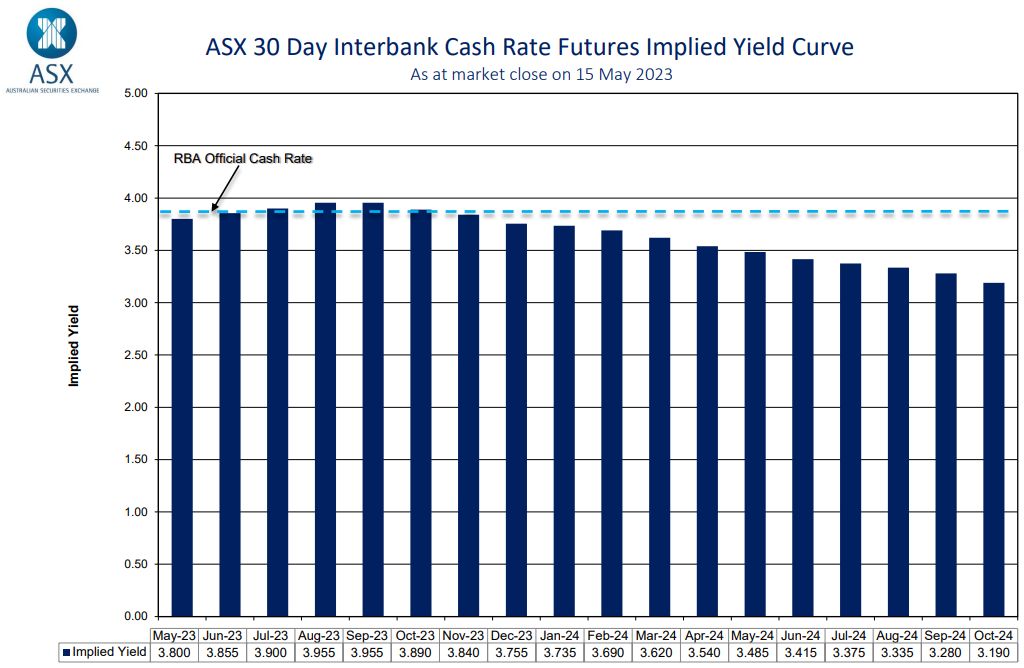

NAB’s hawkish view is at odds with financial markets, which expects rates possibly one more hike before cuts arrive late in the year:

Meanwhile, CBA believes the RBA is unlikely to hike again this cycle, as does Westpac.

Australia’s suffering mortgage holders will certainly be hoping CBA and Westpac have it right and NAB has it wrong.

Time will tell.